Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:NTAP

Is NetApp Attractively Priced After Its Recent Share Pullback And Cloud Growth Push?

Reviewed by Bailey Pemberton

- If you have been wondering whether NetApp at around $110 a share is a bargain or a value trap, you are not alone. This breakdown is designed to give you a clear, no nonsense view.

- The stock has slipped 7.2% over the last week and is down 4.7% year to date, but that comes after a 100.6% gain over 3 years and 89.5% over 5 years, which indicates that the market has already repriced a lot of optimism into the story.

- Recently, investors have been reacting to NetApp's ongoing push into hybrid cloud data services and its deeper partnerships with hyperscalers like Microsoft Azure and AWS. These factors help explain some of the volatility in the share price. There has also been steady attention on its recurring revenue mix and cost discipline, both of which can influence how the market thinks about its long term growth and resilience.

- Right now, NetApp scores a 5/6 valuation check score, suggesting it screens as undervalued on most of our metrics. Next we will unpack what that means across different valuation approaches, before finishing with a more intuitive way to think about what the stock may be worth.

Find out why NetApp's -3.3% return over the last year is lagging behind its peers.

Approach 1: NetApp Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes the cash NetApp is expected to generate in the future and discounts those projections back into todays dollars, giving an estimate of what the whole business is worth now.

NetApp currently generates about $1.68 billion in free cash flow, and analysts see this rising steadily as the company deepens its hybrid cloud and data services positioning. Based on analyst inputs for the next few years and Simply Wall St extrapolations beyond that, free cash flow is projected to climb to roughly $2.65 billion by 2035. These cash flows are all modeled in $ and discounted using a 2 Stage Free Cash Flow to Equity framework, which captures a faster growth phase before fading to more mature growth.

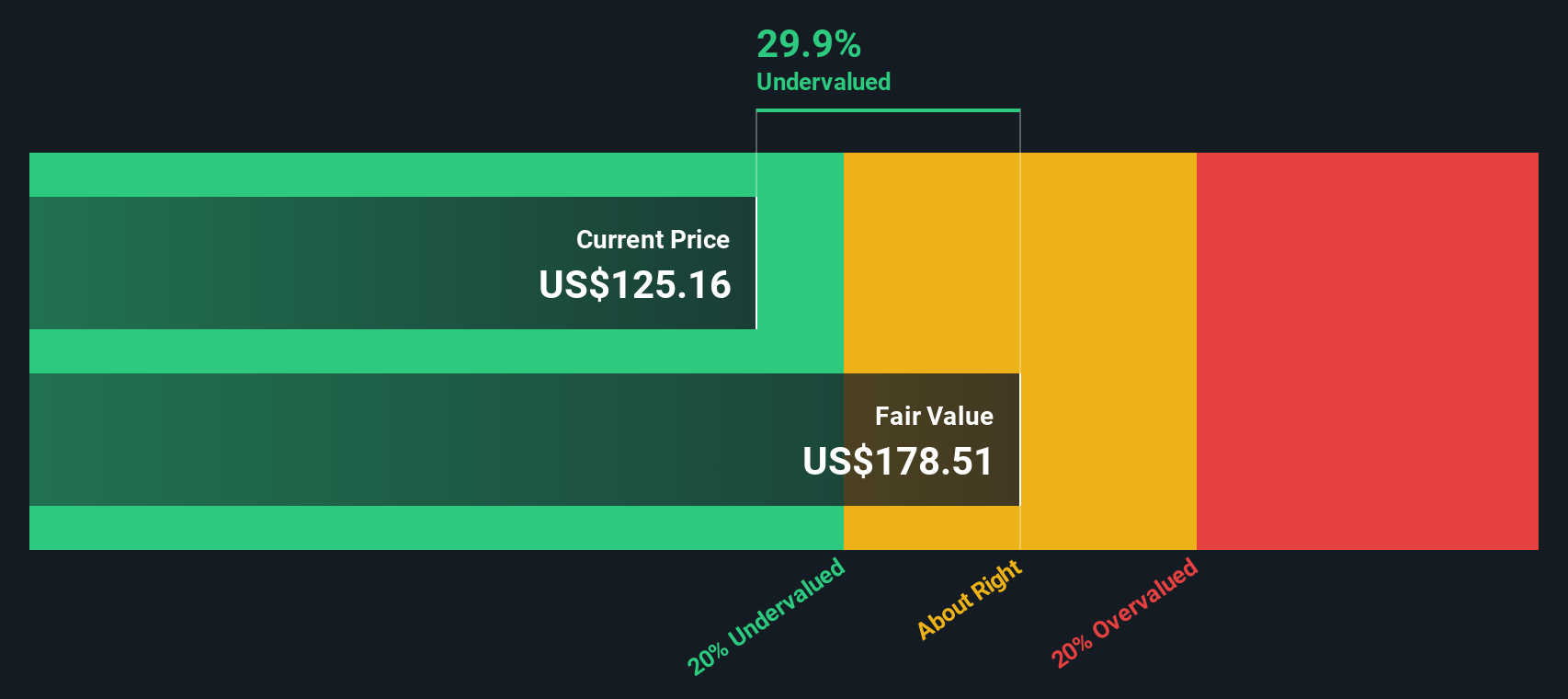

Putting all of those discounted cash flows together results in an estimated intrinsic value of about $185 per share, implying the stock is roughly 40.3% below its DCF fair value at the current price. In other words, the cash flow math points to NetApp trading at a sizable discount.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NetApp is undervalued by 40.3%. Track this in your watchlist or portfolio, or discover 916 more undervalued stocks based on cash flows.

Approach 2: NetApp Price vs Earnings

For a profitable, relatively mature tech business like NetApp, the price to earnings ratio is a useful yardstick because it directly links what investors are paying to the earnings the company is generating today. In general, companies with stronger, more reliable growth and lower perceived risk can justify a higher, or more expensive, PE multiple. Slower growth or higher risk typically calls for a lower, or cheaper, PE.

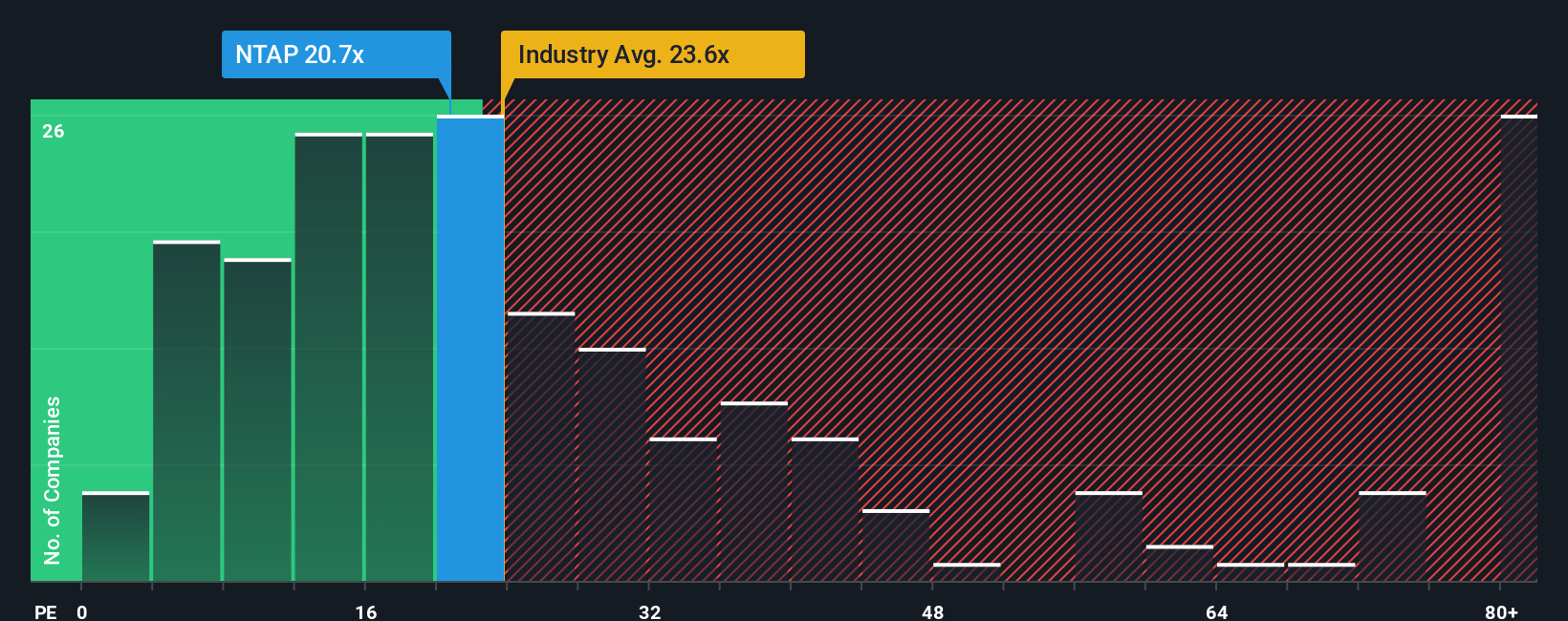

NetApp currently trades on a PE of about 18.6x. That sits below both the broader Tech industry average of roughly 22.0x and well under the peer group average of around 59.4x. This initially points to the stock being priced more conservatively than many of its competitors.

Simply Wall St's Fair Ratio framework goes a step further by estimating what PE multiple NetApp should trade on, given its earnings growth outlook, profitability, industry, size and risk profile. For NetApp, that Fair Ratio comes out at about 25.0x, which indicates that the stock may merit a higher multiple than the market is currently assigning. From an earnings-based perspective, NetApp therefore appears to be priced at a level that could be viewed as attractive relative to these fundamentals.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1455 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your NetApp Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the story you believe about a company, translated into numbers like future revenue, earnings, margins and ultimately a fair value estimate.

A Narrative connects three things in a straight line: the company’s story, a financial forecast based on that story, and a resulting fair value, so you can clearly see why you think a stock is cheap, expensive, or fairly priced.

On Simply Wall St, Narratives are an easy, accessible tool on the Community page that millions of investors use to turn their views into forward looking forecasts, then compare their Fair Value to the current Price to decide whether it is time to buy, hold or sell.

Because Narratives update dynamically as new information like earnings releases, guidance or major news hits the market, your view of NetApp’s worth does not stay static. For example, one investor might build a bullish NetApp Narrative around accelerating AI storage demand and see fair value closer to $130 per share, while another, more cautious investor could assume slower cloud growth and margin pressure and land nearer $100, yet both can clearly see how their assumptions drive different values and decisions.

Do you think there's more to the story for NetApp? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NetApp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NTAP

NetApp

Provides a range of enterprise software, systems, and services that customers use to transform their data infrastructures in the United States, Canada, Latin America, Europe, the Middle East, Africa, and the Asia Pacific.

Very undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.1% undervalued

211 followersusers have followed this narrative

1 commentusers have commented on this narrative

30 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.6% undervalued

53 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0719.6% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3814.1% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on INTLOOP ·

Renewed focus on business investment

Fair Value:JP¥4.17k56.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36036.7% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Fibromat (M) Berhad ·

Fibromat: More than just a niche player, with clearer earnings visibility from order book and project wins

Fair Value:RM 1.0519.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.6% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.5% undervalued

1349 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0