Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:NSSC

Napco Security Technologies (NSSC) Margin Slippage Challenges Bullish Profitability Narratives

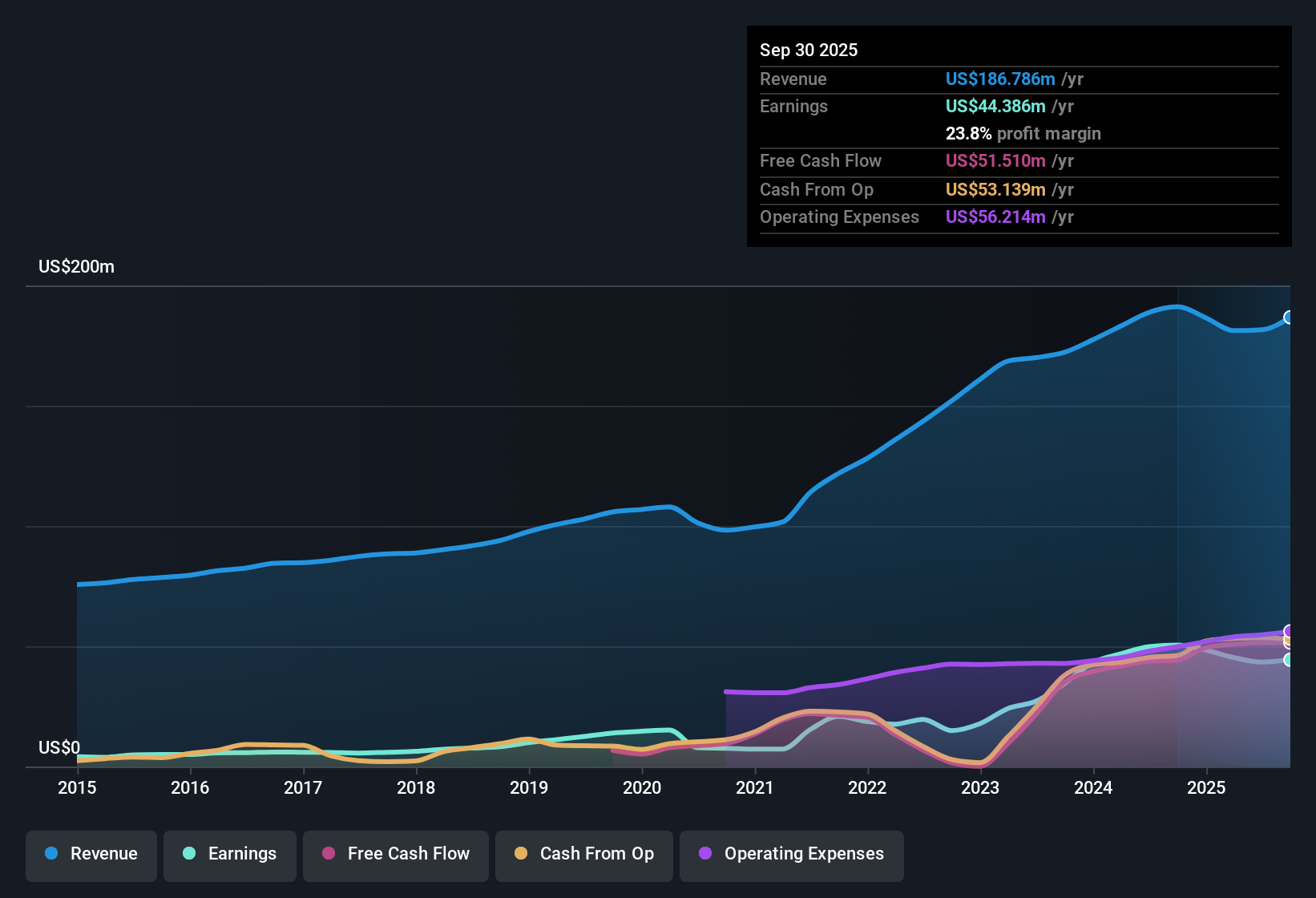

Napco Security Technologies (NSSC) just posted Q2 2026 results with revenue of US$48.2 million and basic EPS of US$0.38, alongside net income of US$13.5 million, putting fresh numbers on the table for investors tracking its profitability. The company has seen quarterly revenue move from US$42.9 million in Q2 2025 to US$48.2 million in Q2 2026, while basic EPS shifted from US$0.29 to US$0.38 over the same span. Trailing twelve month EPS stands at US$1.33 and net income at US$47.4 million, setting up a story that now hinges on how durable its mid 20% margin profile really is.

See our full analysis for Napco Security Technologies.With the latest figures in place, the next step is to weigh these margins and growth expectations against the dominant narratives around NSSC to see which views hold up and which start to look out of sync.

Curious how numbers become stories that shape markets? Explore Community Narratives

Trailing 12‑month profits at US$47.4 million

- Over the last twelve months, Napco generated US$192.0 million of revenue and US$47.4 million of net income, which lines up with the 24.7% net margin figure that has been referenced.

- What stands out for a more bullish view is that trailing EPS of US$1.33 sits above any single quarter in the recent set, yet the same data shows one year of weaker earnings compared with the roughly 29.7% per year pace over five years, which means:

- Supporters can point to steady profits, with net income moving from US$10.5 million in Q2 2025 to US$13.5 million in Q2 2026.

- Cautious investors can point to the fact that trailing net income of US$47.4 million is lower than the US$50.5 million reference point in the earlier LTM data, which is consistent with the comment that one year earnings growth turned negative versus that multi year trend.

Margins ease from 25.9% to 24.7%

- The latest trailing net margin of 24.7% compares with 25.9% in the prior year, which lines up with full year net income moving from US$48.4 million on US$186.5 million of revenue to US$47.4 million on US$192.0 million of revenue.

- Critics who worry about pressure on profitability get some backing here, because:

- The margin slip from 25.9% to 24.7% shows profits did not scale in lockstep with revenue, even though revenue across those two trailing periods stayed in a tight band around US$186 million to US$192 million.

- The negative one year earnings growth that has been flagged sits alongside this softer margin, which together suggests that, over the last year, Napco converted each dollar of sales into slightly less profit than in the prior period.

P/E of 30.8x versus 26.6x sector and DCF fair value

- Napco is referenced at a P/E of 30.8x against a US Electronic industry average of 26.6x and a peer group average of 87.6x, while a DCF fair value of about US$30.02 sits below the current share price of US$41.02.

- Skeptics who focus on valuation find several data points to work with, because:

- The P/E of 30.8x is above the 26.6x industry marker and the share price of US$41.02 is above the DCF fair value reference of roughly US$30.02, which is consistent with the view that the stock may be pricing in more than the cash flow model implies.

- At the same time, the P/E being well below the 87.6x peer average and forecasts calling for about 9.8% revenue growth and 11.0% earnings growth per year give investors some context for why the market might still be comfortable with a premium to the broader industry.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Napco Security Technologies's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Napco’s softer net margin, weaker one year earnings trend versus its multi year pace, and P/E above industry alongside a lower DCF fair value all lean toward valuation risk.

If paying up for that kind of earnings wobble feels uncomfortable, use our pre screened these 877 undervalued stocks based on cash flows to hunt for companies where pricing and cash flow assumptions look more aligned.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Napco Security Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NSSC

Napco Security Technologies

Engages in the development, manufacturing, and sale of electronic security systems for commercial, residential, institutional, industrial, and governmental applications in the United States and internationally.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

120 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.0% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

DO

Double_Bubbler on EnSilica ·

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value:UK£590.2% undervalued

122 followersusers have followed this narrative

17 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Akebia Therapeutics ·

Vafseo and the Future of Renal Anemia Treatment – Akebia’s Vision for a $5B Kidney Disease Portfolio

Fair Value:US$77.2998.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Butler National ·

Butler National (Buks) outperforms.

Fair Value:US$3.449.3% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.6% undervalued

1308 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.0% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

32 likesusers have liked this narrative