Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:NSSC

Napco Security Technologies (NSSC): Margin Decline Reinforces Narrative of Slowing Earnings Momentum

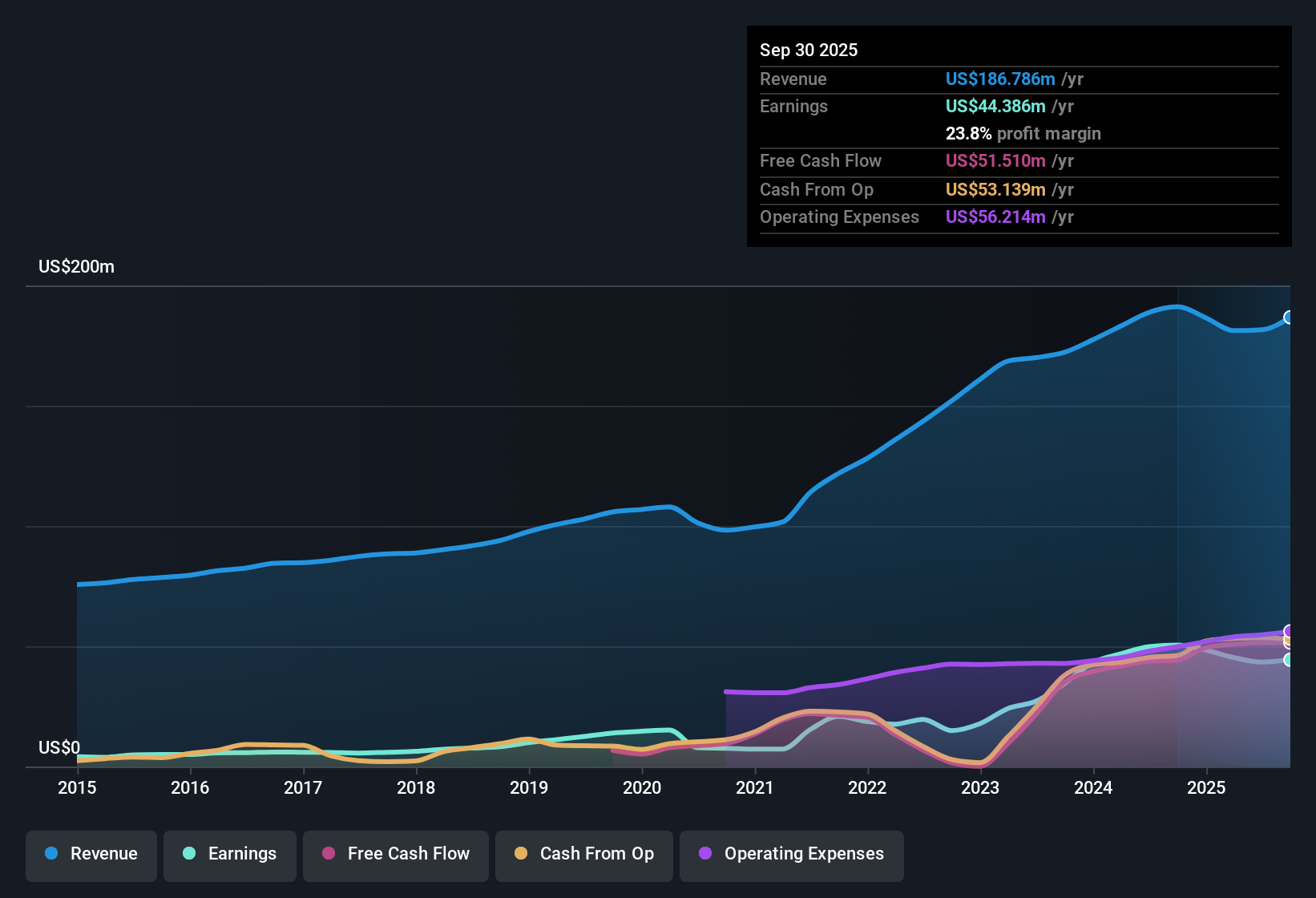

Napco Security Technologies (NSSC) reported earnings growth forecasts of 12.2% per year alongside revenue expected to rise by 9.9% each year. Net profit margins landed at 23.9% this period, down from last year’s 26.4%. Notably, the company saw negative earnings growth most recently despite a five-year average increase of 35.3% per year. With ongoing profit and revenue growth in the forecast, but a moderation in both margins and momentum, investors are faced with weighing solid historical performance against a slowing outlook.

See our full analysis for Napco Security Technologies.Next, we’ll set these up-to-date results alongside the prevailing narratives to see which stories the numbers support and where the conversation might shift.

See what the community is saying about Napco Security Technologies

Recurring Revenue Mix Lifts Predictability

- Recurring monthly service revenue, driven largely by StarLink fire radios and new cloud-based platforms, now makes up an increasing share of Napco’s total sales. This shift is helping stabilize the company’s long-term earnings outlook.

- According to the analysts' consensus view, the higher mix of high-margin, subscription-style revenue is expected to provide more reliable cash flow and margin expansion over the next three years.

- Forecasts call for profit margins to rise from 23.9% today to 24.8% by 2028. Analysts attribute this primarily to continued growth in these recurring lines.

- Consensus narrative states that expansion into new markets with scalable, integrated solutions could further diversify revenue streams and support more predictable, resilient earnings.

Consensus expectations for ongoing margin gains put Napco’s forecast to the test. See why balanced analysts think the services pivot is so crucial: 📊 Read the full Napco Security Technologies Consensus Narrative.

Hardware Slump Challenges Near-Term Margins

- Equipment sales dropped 15.7% year-over-year, with gross margins in this segment falling to 24%. This is down significantly from 29% last year and underscores ongoing softness in traditional hardware demand.

- In the analysts' consensus view, although recurring service revenue growth helps offset these pressures, continued declines in hardware profitability and increased spending on SG&A and R&D could weigh on overall earnings momentum if top-line growth remains weak.

- Operating income declined 14% year-over-year while net income was down 13%. Weakness in hardware outpaced gains in higher-margin services, indicating some risk to sustained margin improvement.

- Analysts highlight that persistent pressure in hardware could threaten not only current margins but also future revenue growth if demand does not stabilize or pricing actions cannot fully compensate for lost volume.

Trading Above DCF Fair Value, At a Sector Premium

- Napco shares recently traded at $40.76, a 30% premium to DCF fair value of $31.31, and with a Price-to-Earnings ratio of 33.5x compared to the US Electronic industry average of 24.3x. This is still below the peer group at 51.5x.

- According to the analysts' consensus view, this premium pricing reflects strong historical growth and expectations for continued margin recovery. It also signals that investors are considering both the opportunities from recurring revenue and the risks of slower growth relative to the broader market.

- Consensus places the analyst price target at $44.50, about 9% above the current price, which suggests limited immediate upside if forecasts prove accurate.

- With valuation already reflecting optimistic profit and revenue gains, any setback in margins or growth drivers could make the stock more sensitive to downside pressure than peers trading closer to their DCF values.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Napco Security Technologies on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Got a different angle on these results? Add your insights and shape your perspective into a unique narrative. Do it in under three minutes. Do it your way

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Napco Security Technologies.

See What Else Is Out There

Napco faces pressure from declining hardware sales and overvaluation risks, which could expose investors to downside if growth drivers falter.

If you're seeking stocks with more attractive valuations and upside potential, search for opportunities now by using these 839 undervalued stocks based on cash flows that are priced more favorably based on their cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Napco Security Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NSSC

Napco Security Technologies

Engages in the development, manufacturing, and sale of electronic security systems for commercial, residential, institutional, industrial, and governmental applications in the United States and internationally.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.551.6% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58016.4% overvalued

29 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8823.8% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.4% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

ES

Esteban on Copart ·

CPRT 04-2026

Fair Value:US$23.0343.6% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

lexdrew1 on GE Vernova ·

GE Vernova revenue will grow by 13% with a future PE of 64.7x

Fair Value:US$1.17k2.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.886.0% undervalued

79 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.5% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.231.8% undervalued

66 followersusers have followed this narrative

2 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5726.7% undervalued

1388 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

TA

Taurustunez88 on Dangote Sugar Refinery ·

With the N500b rights issue, I believe Dangote sugar refinery’s loss due to FX pressures will be dra...

1

|0