- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:LASR

The nLIGHT, Inc. (NASDAQ:LASR) First-Quarter Results Are Out And Analysts Have Published New Forecasts

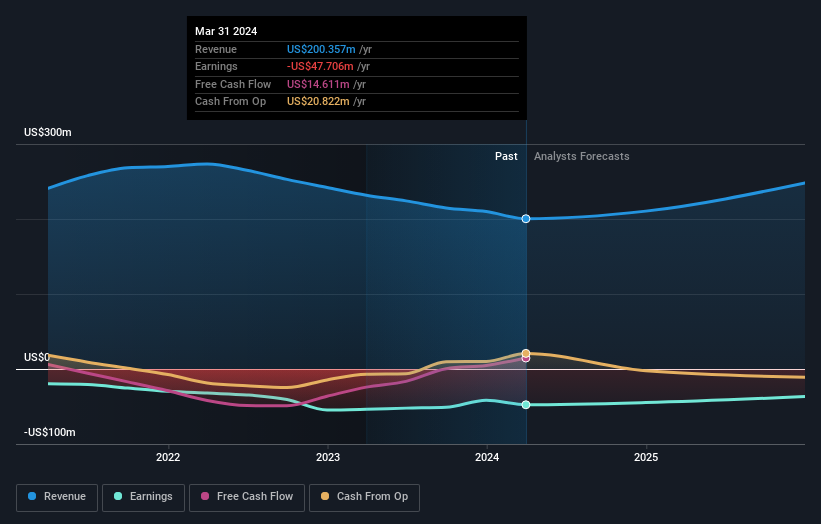

It's been a good week for nLIGHT, Inc. (NASDAQ:LASR) shareholders, because the company has just released its latest first-quarter results, and the shares gained 5.1% to US$12.14. The results look positive overall; while revenues of US$45m were in line with analyst predictions, statutory losses were 7.9% smaller than expected, with nLIGHT losing US$0.29 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

View our latest analysis for nLIGHT

Taking into account the latest results, the current consensus from nLIGHT's six analysts is for revenues of US$210.5m in 2024. This would reflect an okay 5.1% increase on its revenue over the past 12 months. The loss per share is expected to ameliorate slightly, reducing to US$0.93. Before this latest report, the consensus had been expecting revenues of US$211.1m and US$0.98 per share in losses. It looks like there's been a modest increase in sentiment in the recent updates, with the analysts becoming a bit more optimistic in their predictions for losses per share, even though the revenue numbers were unchanged.

The average price target held steady at US$16.00, seeming to indicate that business is performing in line with expectations. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on nLIGHT, with the most bullish analyst valuing it at US$20.00 and the most bearish at US$12.00 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await nLIGHT shareholders.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The analysts are definitely expecting nLIGHT's growth to accelerate, with the forecast 6.8% annualised growth to the end of 2024 ranking favourably alongside historical growth of 4.6% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 6.1% annually. nLIGHT is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their loss per share estimates for next year. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on nLIGHT. Long-term earnings power is much more important than next year's profits. We have forecasts for nLIGHT going out to 2025, and you can see them free on our platform here.

Even so, be aware that nLIGHT is showing 2 warning signs in our investment analysis , you should know about...

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:LASR

nLIGHT

Designs, develops, manufactures, and sells semiconductor and fiber lasers for industrial, microfabrication, and aerospace and defense applications.

Excellent balance sheet with very low risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion