Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:FLEX

Will Weakness in Flex Ltd.'s (NASDAQ:FLEX) Stock Prove Temporary Given Strong Fundamentals?

Flex (NASDAQ:FLEX) has had a rough week with its share price down 9.4%. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. Particularly, we will be paying attention to Flex's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Flex

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Flex is:

20% = US$1.0b ÷ US$5.0b (Based on the trailing twelve months to December 2024).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each $1 of shareholders' capital it has, the company made $0.20 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

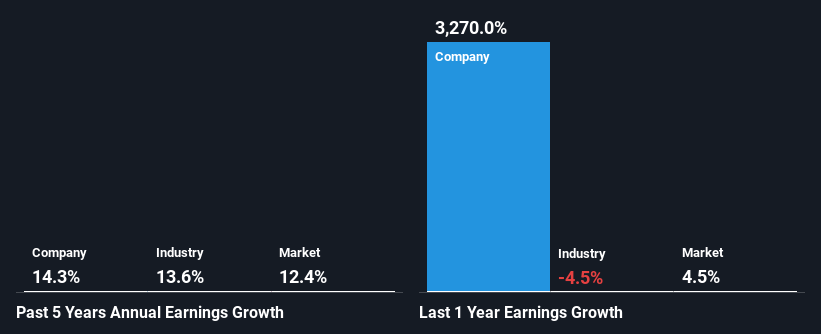

Flex's Earnings Growth And 20% ROE

To start with, Flex's ROE looks acceptable. Further, the company's ROE compares quite favorably to the industry average of 10%. This certainly adds some context to Flex's decent 14% net income growth seen over the past five years.

Next, on comparing Flex's net income growth with the industry, we found that the company's reported growth is similar to the industry average growth rate of 14% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. What is FLEX worth today? The intrinsic value infographic in our free research report helps visualize whether FLEX is currently mispriced by the market.

Is Flex Using Its Retained Earnings Effectively?

Flex doesn't pay any regular dividends, meaning that all of its profits are being reinvested in the business, which explains the fair bit of earnings growth the company has seen.

Summary

Overall, we are quite pleased with Flex's performance. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. Unsurprisingly, this has led to an impressive earnings growth. Having said that, the company's earnings growth is expected to slow down, as forecasted in the current analyst estimates. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:FLEX

Flex

Provides technology innovation, supply chain, and manufacturing solutions to data center, communications, enterprise, consumer, automotive, industrial, healthcare, industrial, and power industries.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JA

Jades on Coca-Cola ·

Coca-Cola’s Enduring Moat in a Health-Conscious World: Steady Compounder Poised for 5-10% Annual Returns Through Emerging Market Dominance

Fair Value:US$66.221.2% overvalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

ET

Ethan_cpa on Xero ·

Xero: Growth Was Priced In — Execution Is Not

Fair Value:AU$101.5622.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.4% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

Recently Updated Narratives

FI

FIMJ on NVIDIA ·

The NVIDIA Phenomenon

Fair Value:US$313.7541.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AA

Aadi_S on Take-Two Interactive Software ·

Take Two Interactive Software TTWO Valuation Analysis

Fair Value:US$2073.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

53

537578 on Recursion Pharmaceuticals ·

Recursion Pharmaceuticals! WTH is going on?

Fair Value:US$1.9784.3% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.0% undervalued

65 followersusers have followed this narrative

5 commentsusers have commented on this narrative

28 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.1% undervalued

1300 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.4% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

Trending Discussion

US

User on Caesars Entertainment ·

I can't take seriously any analysis of Caesars Entertainment when there is not present (at least onc...

0

|0