- United States

- /

- Communications

- /

- NasdaqGS:AUDC

Consider This Before Buying AudioCodes Ltd. (NASDAQ:AUDC) For The 1.4% Dividend

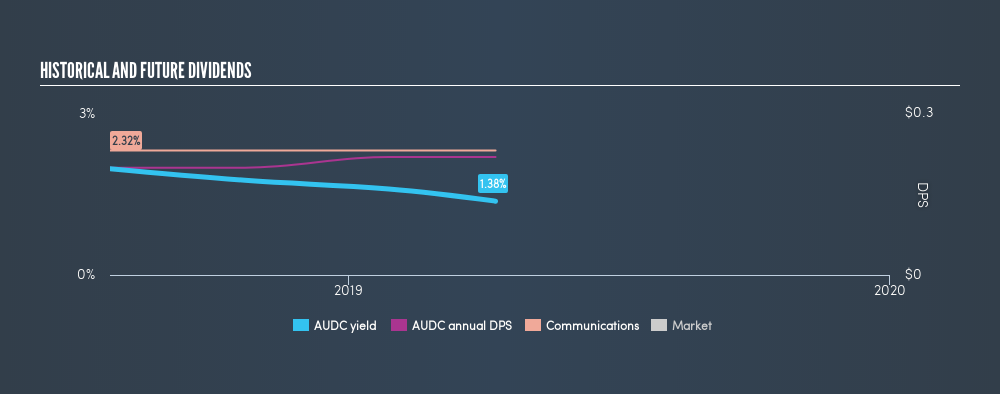

Dividends can be underrated but they form a large part of investment returns, playing an important role in compounding returns in the long run. AudioCodes Ltd. (NASDAQ:AUDC) has begun paying dividends recently. It now yields 1.4%. Should it have a place in your portfolio? Let's take a look at AudioCodes in more detail.

View our latest analysis for AudioCodes

Here's how I find good dividend stocks

When researching a dividend stock, I always follow the following screening criteria:

- Is it the top 25% annual dividend yield payer?

- Has its dividend been stable over the past (i.e. no missed payments or significant payout cuts)?

- Has the amount of dividend per share grown over the past?

- Is is able to pay the current rate of dividends from its earnings?

- Will the company be able to keep paying dividend based on the future earnings growth?

Does AudioCodes pass our checks?

The company currently pays out 66% of its earnings as a dividend, according to its trailing twelve-month data, meaning the dividend is sufficiently covered by earnings. Furthermore, analysts have not forecasted a dividends per share for the future, which makes it hard to determine the yield shareholders should expect, and whether the current payout is sustainable, moving forward.

When considering the sustainability of dividends, it is also worth checking the cash flow of a company. Cash flow is important because companies with strong cash flow can usually sustain higher payout ratios.

If there's one type of stock you want to be reliable, it's dividend stocks and their stable income-generating ability. The reality is that it is too early to consider AudioCodes as a dividend investment. Last year was the company's first dividend payment, so it is certainly early days. The standard practice for reliable payers is to look for 10 or so years of track record.

In terms of its peers, AudioCodes has a yield of 1.4%, which is on the low-side for Communications stocks.

Next Steps:

Now you know to keep in mind the reason why investors should be careful investing in AudioCodes for the dividend. On the other hand, if you are not strictly just a dividend investor, the stock could still be offering some interesting investment opportunities. Given that this is purely a dividend analysis, I recommend taking sufficient time to understand its core business and determine whether the company and its investment properties suit your overall goals. There are three important aspects you should look at:

- Valuation: What is AUDC worth today? Even if the stock is a cash cow, it's not worth an infinite price. The intrinsic value infographic in our free research report helps visualize whether AUDC is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on AudioCodes’s board and the CEO’s back ground.

- Dividend Rockstars: Are there better dividend payers with stronger fundamentals out there? Check out our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:AUDC

AudioCodes

Provides advanced communications software, products, and productivity solutions for the digital workplace worldwide.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion