Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqCM:AEY

Does ADDvantage Technologies Group (NASDAQ:AEY) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that ADDvantage Technologies Group, Inc. (NASDAQ:AEY) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for ADDvantage Technologies Group

What Is ADDvantage Technologies Group's Debt?

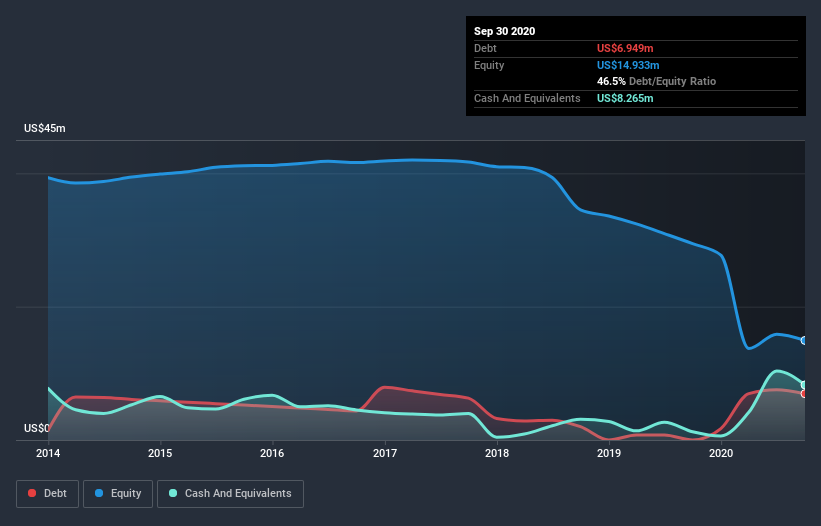

As you can see below, at the end of September 2020, ADDvantage Technologies Group had US$6.95m of debt, up from none a year ago. Click the image for more detail. But on the other hand it also has US$8.27m in cash, leading to a US$1.32m net cash position.

How Healthy Is ADDvantage Technologies Group's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that ADDvantage Technologies Group had liabilities of US$11.2m due within 12 months and liabilities of US$6.56m due beyond that. Offsetting this, it had US$8.27m in cash and US$7.24m in receivables that were due within 12 months. So it has liabilities totalling US$2.24m more than its cash and near-term receivables, combined.

Since publicly traded ADDvantage Technologies Group shares are worth a total of US$37.9m, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, ADDvantage Technologies Group boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is ADDvantage Technologies Group's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year ADDvantage Technologies Group had a loss before interest and tax, and actually shrunk its revenue by 9.1%, to US$50m. We would much prefer see growth.

So How Risky Is ADDvantage Technologies Group?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that ADDvantage Technologies Group had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$4.4m and booked a US$17m accounting loss. Given it only has net cash of US$1.32m, the company may need to raise more capital if it doesn't reach break-even soon. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - ADDvantage Technologies Group has 4 warning signs (and 1 which can't be ignored) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade ADDvantage Technologies Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:AEY

ADDvantage Technologies Group

ADDvantage Technologies Group, Inc., through its subsidiaries, operates as a communications infrastructure services and equipment provider in the United States and internationally.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

76 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

WA

wahyud on Perusahaan Perkebunan London Sumatra Indonesia ·

LSIP Revenue to Rise a Whopping 43.92% Amid Market Dynamics

Fair Value:Rp3.6k63.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Charoen Pokphand Indonesia ·

Charoen Pokphand Indonesia will soar with a 12.94% growth and a 10.67x future P/E

Fair Value:Rp4.53k4.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Medco Energi Internasional ·

Medco Energi's Revenue Will Increase by 2.45% Doors Opening

Fair Value:Rp1.75k23.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

113 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1194 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative