RingCentral (RNG) just made a set of moves that could have big implications for those weighing what to do with its stock. The company expanded its existing credit agreement to $1.24 billion, with major players like Bank of America and JPMorgan involved. At the same time, it announced a $500 million share buyback plan. Combined with a net income turnaround last quarter and recent earnings upgrades from analysts, these events underscore strengthening financial flexibility and a positive shift in momentum.

Taking a look at RingCentral’s performance this year, the picture is more nuanced. The stock has bounced back over the past three months with a double-digit percentage gain, but it is still down for the year as a whole. Over the longer term, results have lagged, even as annual sales and earnings have started to pick up. The setup now leaves investors balancing short-term optimism with the longer view. Momentum may be building again, but the past few years still cast a long shadow.

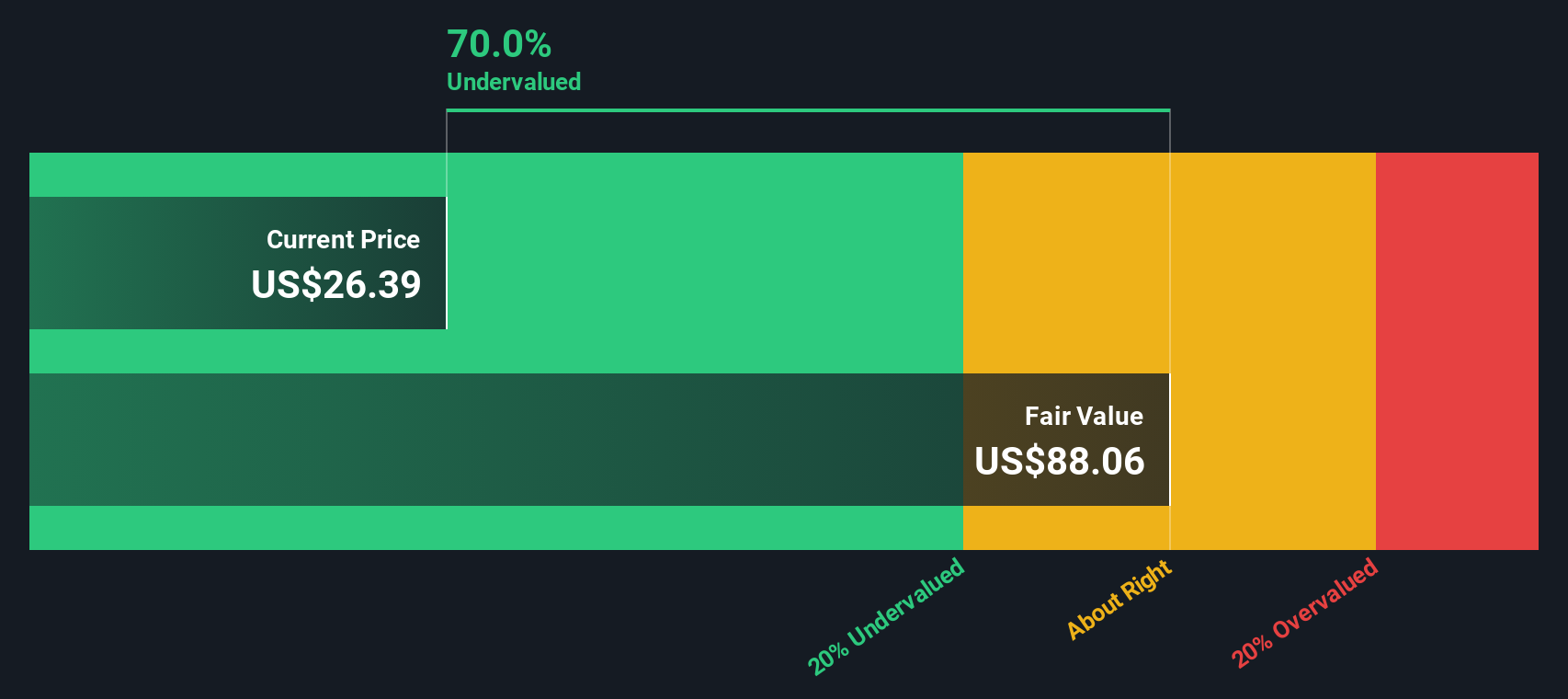

After this recent surge in financial maneuvering and a rebound in net income, the big question becomes whether RingCentral’s stock is finally trading at a discount or if the market is already pricing in all the good news.

Advertisement

Most Popular Narrative: 6.1% Undervalued

According to the most widely followed narrative, RingCentral is trading modestly below its estimated fair value, with a discount rate applied that reflects moderate expectations of future growth and risk.

The expansion of AI-powered products such as RingCX, RingSense, and AIR is driving new customer adoption and early double-digit growth. This is positioning RingCentral to capture additional market share as enterprises accelerate their digital transformation initiatives and seek more automated, data-driven communication solutions. These trends are likely to support future revenue growth and margin expansion.

Curious what is fueling this undervalued call? One number in particular could change the narrative for years to come, and it is not just about revenue. There is a bold set of assumptions working beneath the surface, including a major turnaround in profitability and robust market share expansion. Want to see how these projections all add up to that price target? The future is not as predictable as the numbers might suggest.

However, growing competition from bundled communications suites and dependency on key partners could quickly challenge this outlook if business conditions change.

But our DCF model adds another angle entirely. It digs into long-term cash flow forecasts, and by this method, RingCentral still comes out significantly undervalued. Could this be a signal that the market is missing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out RingCentral for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own RingCentral Narrative

If you see things differently, or want to dig into RingCentral’s data on your own terms, you can craft your own perspective in just minutes. Do it your way

A great starting point for your RingCentral research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready for Your Next Investing Opportunity?

If you want to stay ahead of the curve, put your money to work smarter, and never miss the breakout stories, these ideas are made for you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies