Advertisement

- United States

- /

- Software

- /

- NYSE:ESTC

Could Elastic (ESTC) AI Enhancements Shift the Narrative on Long-Term Competitive Positioning?

Simply Wall St

Reviewed by Sasha Jovanovic

- In October 2025, Elastic introduced Agent Builder for rapidly creating custom AI agents using enterprise data and launched a managed OpenTelemetry Protocol endpoint within Elastic Observability, enhancing developer productivity and simplifying telemetry infrastructure management for enterprises.

- These product releases underscore Elastic's commitment to enabling faster and more secure deployment of generative AI solutions and streamlining cloud observability operations through automation and context engineering advancements.

- We'll take a closer look at how Agent Builder’s focus on context-rich AI agents may influence Elastic’s long-term investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Elastic Investment Narrative Recap

For investors considering Elastic, the central thesis often rests on the company’s ability to capitalize on accelerating enterprise demand for artificial intelligence and unified data search, observability, and security platforms. The recent launch of Agent Builder and managed OpenTelemetry endpoint reinforce Elastic's focus on AI-driven product innovation, but these alone do not fundamentally alter the biggest near-term catalyst, the shift of enterprise workloads to Elastic Cloud, or the primary risk of intensifying competition from hyperscale cloud providers.

Of the two news events, the introduction of Agent Builder stands out as most relevant for investors thinking about Elastic’s catalyst of AI-powered feature adoption, as it could support further expansion within existing enterprise accounts by deepening product integration and value proposition.

However, investors should also keep in mind the potential impact of growing competition from large cloud vendors, especially as the market continues to prioritize vertically integrated, cloud-based platforms over standalone offerings...

Read the full narrative on Elastic (it's free!)

Elastic's current analysis anticipates $2.3 billion in revenue and $50.5 million in earnings by 2028. To achieve this, the company needs to deliver 13.9% annual revenue growth and increase earnings by $134 million from the current -$83.5 million.

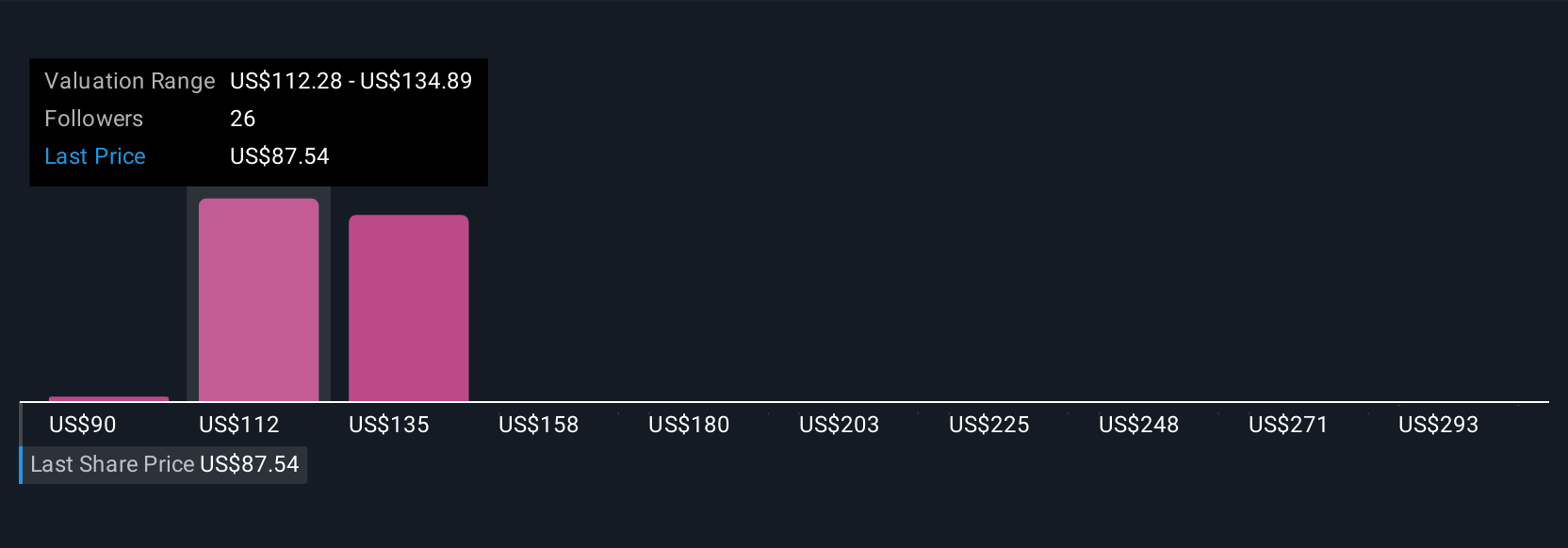

Uncover how Elastic's forecasts yield a $120.16 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Seven private investor fair value estimates from the Simply Wall St Community span a range from US$89.66 to US$315.80 per share. While the market weighs these contrasting viewpoints, ongoing cloud migration remains a key story with broad implications for Elastic’s revenue mix and competitive positioning.

Explore 7 other fair value estimates on Elastic - why the stock might be worth over 3x more than the current price!

Build Your Own Elastic Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Elastic research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Elastic research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Elastic's overall financial health at a glance.

No Opportunity In Elastic?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Elastic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ESTC

Elastic

A search artificial intelligence (AI) company, provides software platforms to run in hybrid, public or private clouds, and multi-cloud environments in the United States and internationally.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor