Advertisement

- United States

- /

- IT

- /

- NYSE:DXC

Will DXC Technology’s (DXC) AI Security Push Reshape Its Long-Term Competitive Edge?

- In recent days, DXC Technology announced new partnerships in AI-driven security operations and digital accessibility, including a multi-million customer engagement with Banco Sabadell, alongside reporting its first quarter fiscal 2026 earnings and updated revenue guidance for the rest of the year.

- A key highlight is the launch of DXC’s AI-powered Security Operations Center with 7AI, which promises substantial cost efficiencies and strengthens their position in managed security services.

- We will assess how this AI-centered service launch could influence DXC’s long-term investment outlook and business transformation narrative.

AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

DXC Technology Investment Narrative Recap

To be a shareholder in DXC Technology today, you need confidence in the company’s ability to pivot from persistent revenue declines toward lasting digital growth, while navigating operational restructuring and leadership changes. The first-quarter results and renewed guidance confirm that organic revenue is still forecast to contract by 3–5% in fiscal 2026, keeping the spotlight on slow top-line recovery as the most material short-term risk; the recent product and client wins, while promising, do not offset this near-term revenue pressure.

Among the recent announcements, the launch of DXC’s AI-powered Security Operations Center in partnership with 7AI stands out, delivering measurable efficiency gains to clients and positioning DXC as a player in automation-driven cyber services. While this initiative could build credibility for future contract bookings and support medium-term catalysts, it does not materially change the urgency for DXC to accelerate high-quality, scalable digital revenue near term.

By contrast, investors should also have clear visibility into ongoing execution risks such as leadership turnover and its impact on strategy, since...

Read the full narrative on DXC Technology (it's free!)

DXC Technology's narrative projects $12.3 billion in revenue and $246.9 million in earnings by 2028. This requires a 1.6% annual revenue decline and a $142.1 million decrease in earnings from the current $389.0 million.

Uncover how DXC Technology's forecasts yield a $16.50 fair value, a 25% upside to its current price.

Exploring Other Perspectives

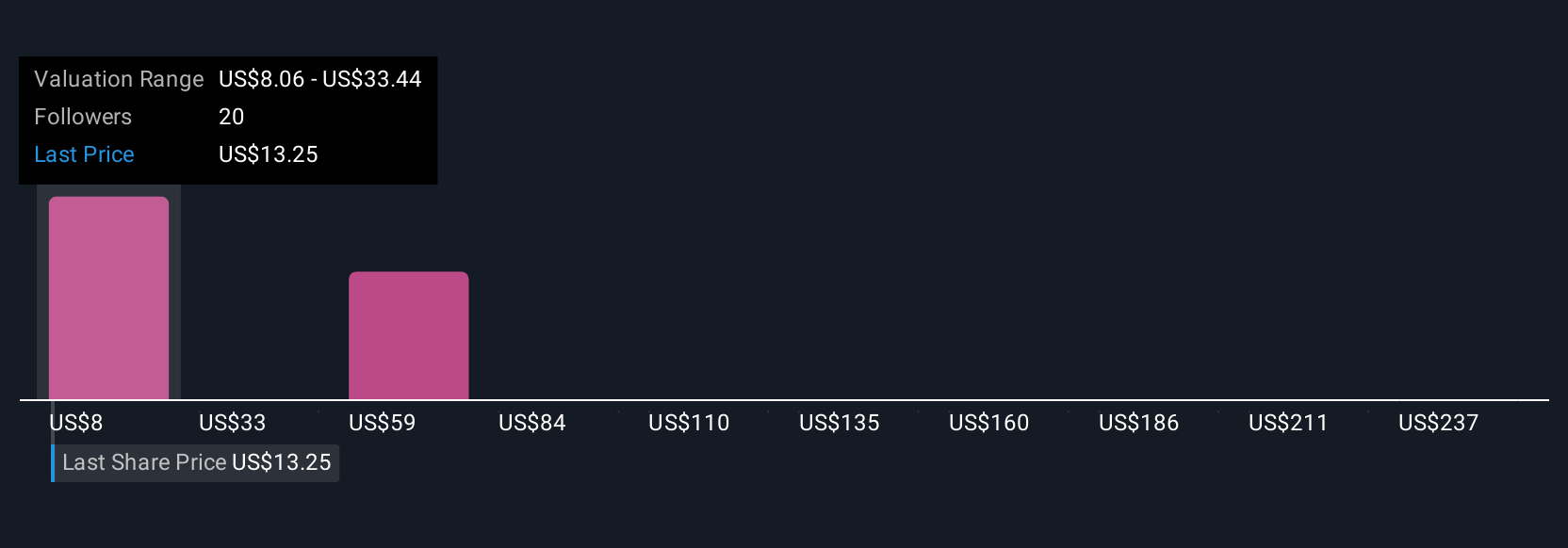

Fair value estimates from six Simply Wall St Community members for DXC range dramatically from US$8.06 to US$261.89 per share. Yet, persistent organic revenue decline remains a core concern that could shape DXC’s performance for those weighing various outlooks.

Explore 6 other fair value estimates on DXC Technology - why the stock might be worth 39% less than the current price!

Build Your Own DXC Technology Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your DXC Technology research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free DXC Technology research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DXC Technology's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 19 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DXC

DXC Technology

Provides information technology services and solutions in the United States, the United Kingdom, the Rest of Europe, Australia, and internationally.

Very undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

289 followersusers have followed this narrative

1 commentusers have commented on this narrative

43 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

102 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

9 followersusers have followed this narrative

3 commentsusers have commented on this narrative

4 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on OceanaGold ·

OceanaGold: Potential Upside with High Costs and Mid-Tier Status

Fair Value:CA$65.3336.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18057.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

HedgeY on Newron Pharmaceuticals ·

Still A Binary Phase III Bet on Evenamide

Fair Value:CHF 1824.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

102 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.229.5% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.1% undervalued

1400 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative