Zscaler (ZS) shares have been on the move recently, catching the eye of investors curious about the company's direction this month. Trading patterns show shifts that raise questions about current valuation and growth prospects.

Zscaler’s share price has been on a bumpy ride lately, sliding 8.2% over the past week and dropping 14.9% in the last month. However, it is still holding on to a robust year-to-date share price return of 51.4%. While recent volatility reflects shifting risk sentiment, the company's strong one-year total shareholder return of 30.4% and its impressive three-year gain of 98.2% suggest that momentum, despite some short-term ups and downs, remains firmly positive for long-term investors.

But after this volatility and a strong longer-term performance, the central question remains: is Zscaler now undervalued with room to run, or is the market already pricing in its future growth potential?

Advertisement

Most Popular Narrative: 16% Undervalued

Zscaler's fair value estimate is $327.98 per share, notably above the latest closing price of $275.01. This valuation gap draws attention to a narrative shaped by high growth expectations and sector innovation.

Explosive growth in AI/ML traffic and emerging threats is creating new security challenges that Zscaler is rapidly addressing with differentiated AI security and agentic operations products. This positions the company to capture a rising share of incremental cyber budgets and expand recurring ARR over the long term.

Want to see what fuels this premium price? The narrative is built on bold growth assumptions and a future profit turnaround rarely expected outside the fastest-growing tech. Curious how bullish projections and a unique margin outlook combine for a punchy valuation? Take a closer look to unlock the real numbers and underlying story powering this estimate.

However, increasing competition from established cybersecurity giants and the rapid pace of product launches could hinder Zscaler’s future market share and profit margins.

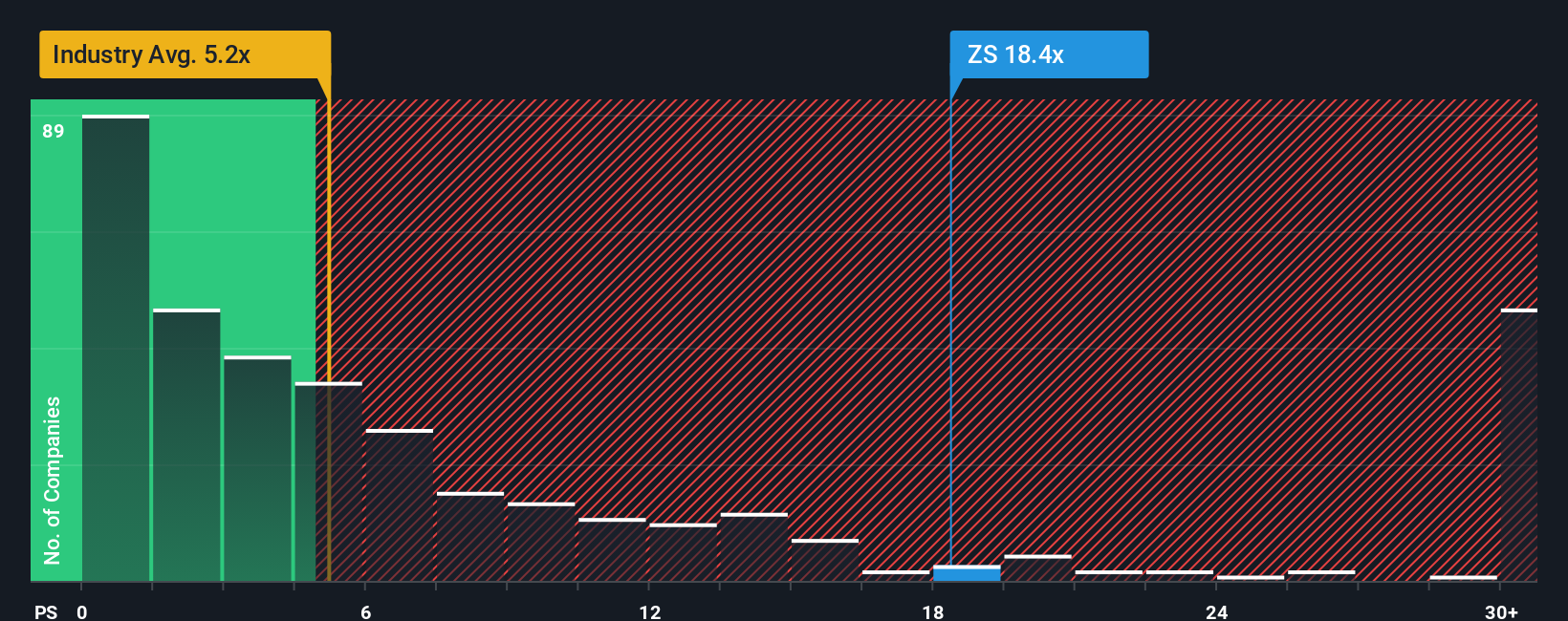

Looking through the lens of the price-to-sales ratio, Zscaler does not look cheap. At 16.3x, it trades well above both the industry average of 4.6x and the peer average of 15.5x, with the fair ratio at 12.5x. This suggests a premium price tag and a risk that market expectations might get ahead of reality. Is this level of optimism justified, or are investors setting themselves up for disappointment?

If you want to dig into the numbers firsthand or have your own take on Zscaler’s outlook, you can easily shape your own narrative in just a few minutes: Do it your way

Don’t let market moves pass you by. Uncover smarter opportunities by checking out handpicked lists that highlight trends, value, and future growth potential right now.

Catch rising trends in artificial intelligence by reviewing these 26 AI penny stocks, which are reshaping industries and unlocking game-changing innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zscaler might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.