Zscaler (ZS) shares have climbed about 8% over the past 3 months, drawing attention from investors who are tracking steady gains in the cybersecurity sector. Growth in annual revenue and improving net income trends continue to shape optimism.

Zscaler has ridden a wave of sector momentum, with its share price returning nearly 8% in the last three months and a solid 69.5% year-to-date. This continues a strong run, highlighted by a 70% total shareholder return over the past year and more than doubling investors’ money over three and five years. Recent gains suggest optimism about the company’s long-term growth prospects is building, as investors respond to ongoing revenue growth and improved profitability.

If you’re watching trends in digital security, it makes sense to see which other fast-growing tech and AI companies are capturing investor attention. See the full list for free.

With shares near all-time highs and strong performance metrics, investors may wonder if Zscaler is undervalued and primed for future gains or if the market has already priced in much of its growth potential.

Advertisement

Most Popular Narrative: 5.2% Undervalued

Compared to the latest closing price of $307.92, the most widely followed narrative estimates Zscaler's fair value at $324.66. This suggests the stock could still gain ground if the key growth drivers play out as projected in the narrative.

Strategic platform innovation and programs like Z-Flex are driving broader product adoption within existing accounts and enabling larger, multi-year deals. This is increasing total contract value and supporting higher future operating margins through scale.

What’s behind this upbeat fair value? The story centers on expanding margins, aggressive platform adoption, and blockbuster multi-year growth. There is a bold set of fundamental forecasts running the show. If you want to see exactly how these expectations add up, the full narrative breaks it down in detail.

However, increasing competition from established cybersecurity giants and ongoing cloud provider integration could put pressure on Zscaler’s growth trajectory and margins moving forward.

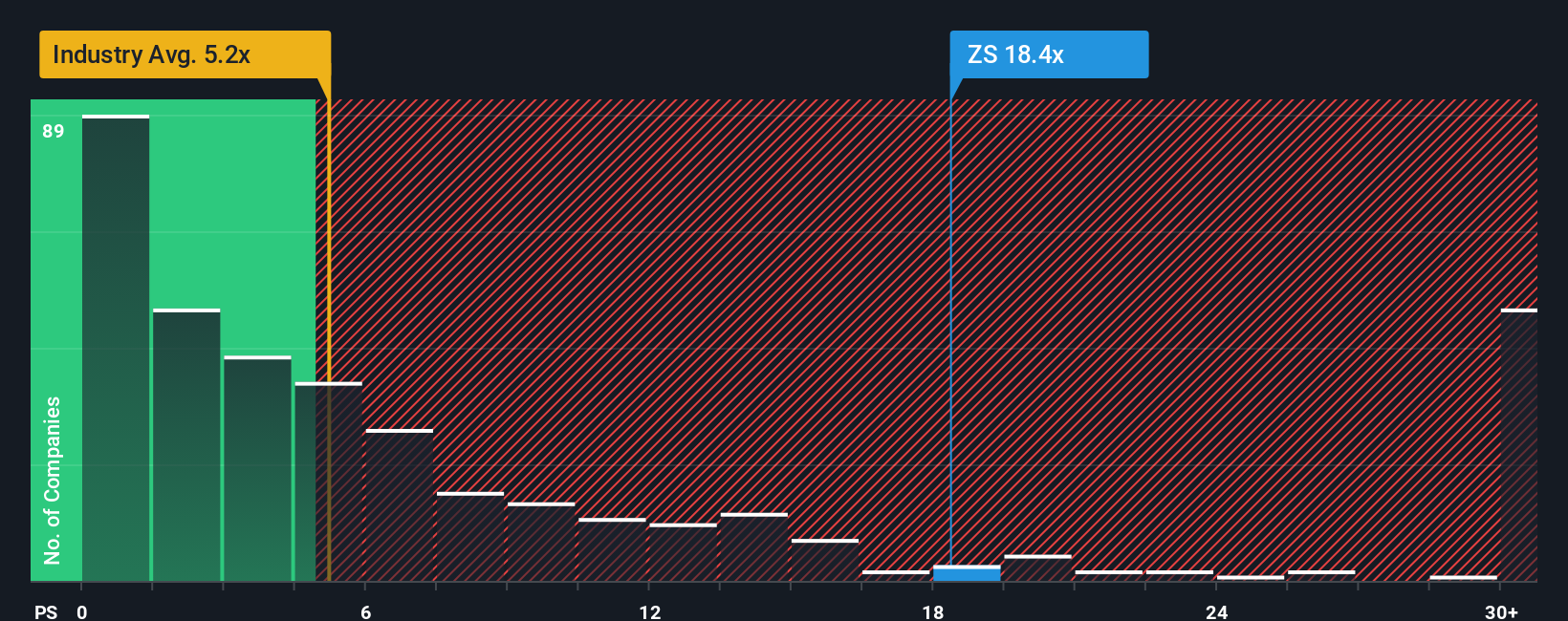

Looking at how Zscaler’s price compares to sales, the stock currently trades at 18.2 times sales versus an industry average of just 5.2, and even peers average 19. This is also above the fair ratio of 13.1. Such a wide gap means investors are paying a significant premium. The market has already priced in a lot of growth, which adds some risk if things do not go perfectly. Are investors too optimistic, or will Zscaler keep justifying this lofty valuation?

If you have a different perspective or want to dive deeper into the financials, you can quickly build your own narrative using our tools. Do it your way

Unlock even more opportunities beyond Zscaler by targeting stocks with promising growth, unique value, or sector leadership. Don’t let your next smart investment slip by. These handpicked strategies are just a click away.

Spot emerging trends early when you review these 26 AI penny stocks offering exposure to cutting-edge artificial intelligence innovations at accessible prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zscaler might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.