Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ZM

Some Shareholders Feeling Restless Over Zoom Communications Inc.'s (NASDAQ:ZM) P/E Ratio

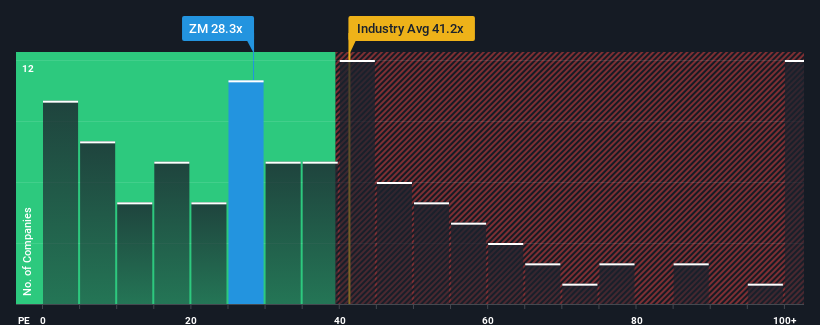

With a price-to-earnings (or "P/E") ratio of 28.3x Zoom Communications Inc. (NASDAQ:ZM) may be sending very bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 18x and even P/E's lower than 11x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Recent times have been advantageous for Zoom Communications as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

Check out our latest analysis for Zoom Communications

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Zoom Communications' to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 288% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 21% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 0.2% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 11% per annum growth forecast for the broader market.

With this information, we find it concerning that Zoom Communications is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

What We Can Learn From Zoom Communications' P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Zoom Communications' analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Zoom Communications that you need to be mindful of.

You might be able to find a better investment than Zoom Communications. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Zoom Communications might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ZM

Zoom Communications

Provides an Artificial Intelligence-first open work platform for human connection in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.8% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

AG

AgWiz on Ingredion ·

Ingredion's Future PE of 9.5x Will Make Waves in the Investment Community

Fair Value:US$88.2311.0% overvalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LY

Lyra on DT Cloud Star Acquisition ·

A SPAC in the Endgame Between Lifeboat and Siren Song

Fair Value:US$6.1584.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.7% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

57 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative