Stock Analysis

- United States

- /

- IT

- /

- NasdaqGS:VRSN

The past three years for VeriSign (NASDAQ:VRSN) investors has not been profitable

Many investors define successful investing as beating the market average over the long term. But the risk of stock picking is that you will likely buy under-performing companies. Unfortunately, that's been the case for longer term VeriSign, Inc. (NASDAQ:VRSN) shareholders, since the share price is down 22% in the last three years, falling well short of the market return of around 22%. The more recent news is of little comfort, with the share price down 22% in a year. Shareholders have had an even rougher run lately, with the share price down 10% in the last 90 days. This could be related to the recent financial results - you can catch up on the most recent data by reading our company report.

Since shareholders are down over the longer term, lets look at the underlying fundamentals over the that time and see if they've been consistent with returns.

See our latest analysis for VeriSign

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

During the unfortunate three years of share price decline, VeriSign actually saw its earnings per share (EPS) improve by 15% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

It's worth taking a look at other metrics, because the EPS growth doesn't seem to match with the falling share price.

We note that, in three years, revenue has actually grown at a 5.9% annual rate, so that doesn't seem to be a reason to sell shares. It's probably worth investigating VeriSign further; while we may be missing something on this analysis, there might also be an opportunity.

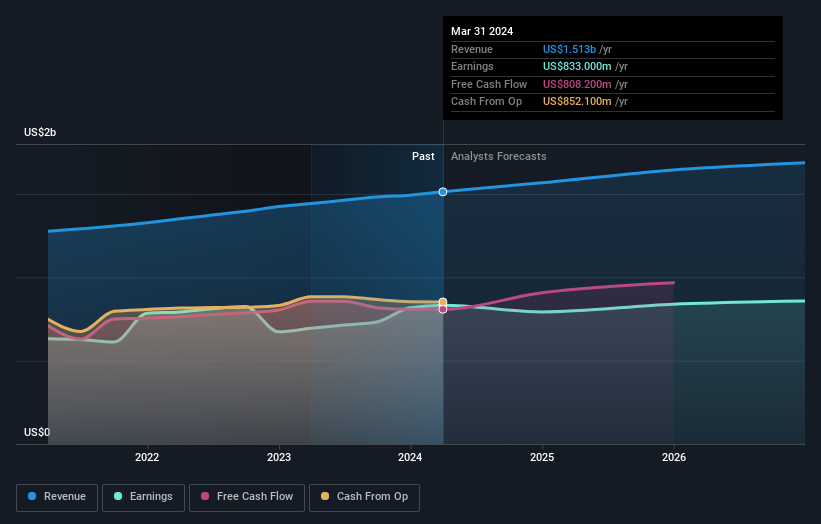

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We know that VeriSign has improved its bottom line lately, but what does the future have in store? You can see what analysts are predicting for VeriSign in this interactive graph of future profit estimates.

A Different Perspective

VeriSign shareholders are down 22% for the year, but the market itself is up 30%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 2% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. It's always interesting to track share price performance over the longer term. But to understand VeriSign better, we need to consider many other factors. For example, we've discovered 3 warning signs for VeriSign (1 can't be ignored!) that you should be aware of before investing here.

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether VeriSign is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:VRSN

VeriSign

Provides domain name registry services and internet infrastructure that enables internet navigation for various recognized domain names worldwide.

Solid track record and good value.