Advertisement

- United States

- /

- IT

- /

- NasdaqGS:VRSN

Is VeriSign Still a Smart Bet After 22.9% Year-to-Date Surge?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if VeriSign is a bargain or overpriced right now? Let's dig into what really drives its value and return potential.

- VeriSign's stock price has climbed steadily, up 22.9% year to date and showing a 35.8% return over the past year, which has certainly grabbed the market's attention.

- Over the last few months, headline news has focused on VeriSign's continued dominance as the registry for .com and .net domains, as well as regulatory discussions around internet infrastructure. These developments have been key drivers behind the recent price momentum and growing investor interest.

- The company currently earns a 2 out of 6 valuation score, highlighting some concerns about its price tag. Next, we will break down what this score really means. Stay tuned for an even more effective way to gauge VeriSign's fair value at the end of the article.

VeriSign scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: VeriSign Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the value of a company by projecting its future cash flows and then discounting those flows back to today. This allows investors to assess what the business is fundamentally worth based on its future profit potential, rather than relying solely on current earnings or market sentiment.

For VeriSign, the current Free Cash Flow stands at $998 million. Analysts expect this figure to keep growing, with estimates for 2026 reaching $1.16 billion. Looking further ahead, using projections extrapolated beyond analyst coverage, VeriSign’s free cash flow in 2035 is modeled to reach approximately $1.82 billion. All these forecasts are in US dollars.

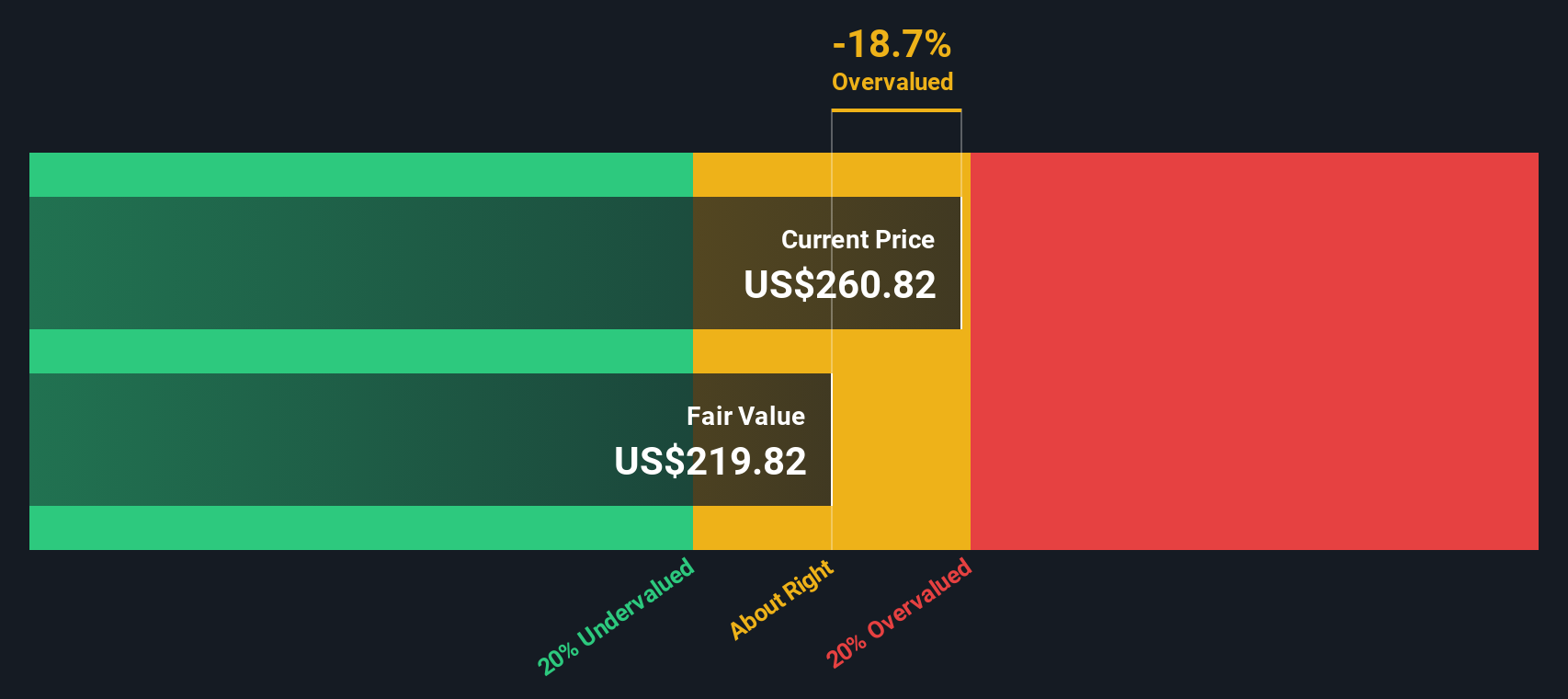

Based on this 2 Stage Free Cash Flow to Equity model, VeriSign’s intrinsic value is calculated to be $244.18 per share. However, the stock market is currently valuing the shares at a level around 3.2% higher than this estimate. This suggests the stock is just slightly overvalued, but remains within a reasonable range based on cash flow fundamentals.

Result: ABOUT RIGHT

VeriSign is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: VeriSign Price vs Earnings

The price-to-earnings (PE) ratio is widely used to value profitable companies like VeriSign, as it connects a stock’s price to how much profit it actually generates. Investors favor this metric for mature, consistently earnings-positive businesses because it gives a straightforward snapshot of how expensive the stock is relative to its bottom line.

A “normal” or fair PE ratio is shaped by many factors, especially how fast investors expect a company’s profits to grow and the perceived risks around those future earnings. Companies with strong growth prospects or more predictable earnings tend to command higher PE ratios. Those with slower growth or greater uncertainty often trade at lower multiples.

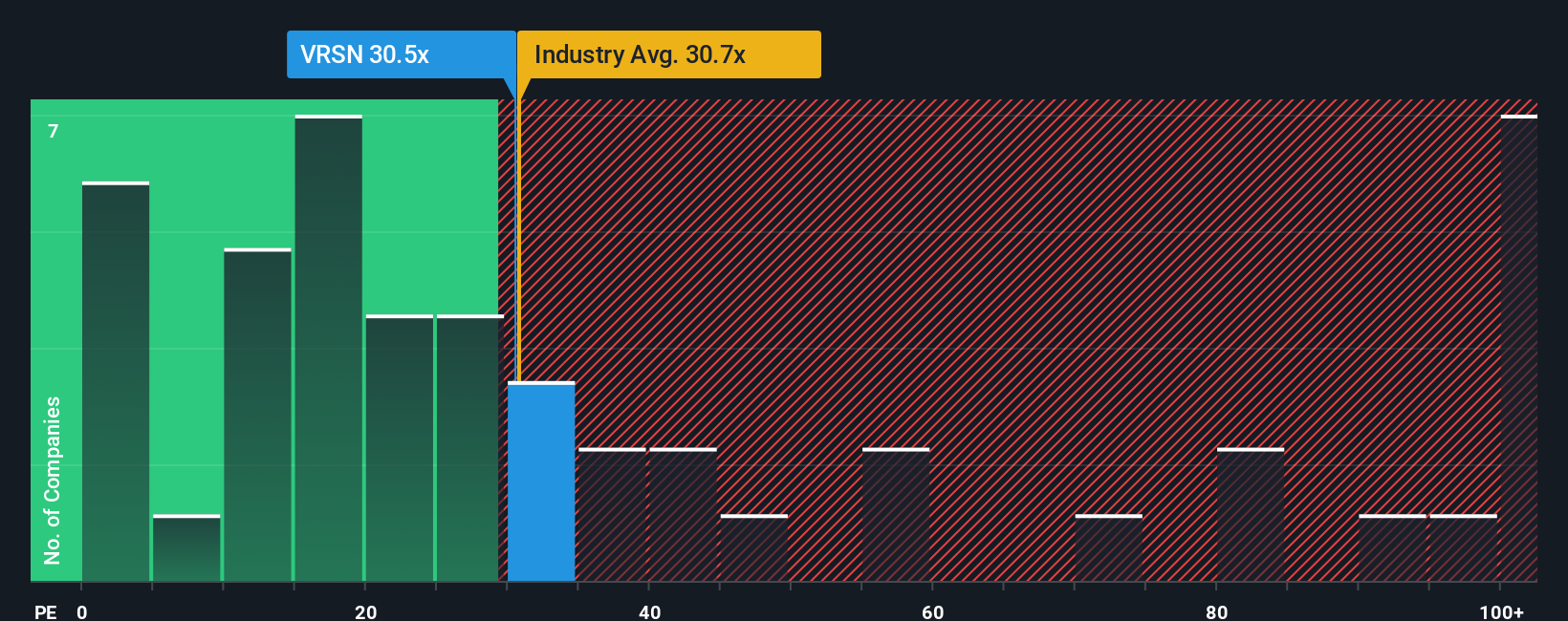

Currently, VeriSign trades at a PE ratio of 28.8x, which is very close to the average for the broader IT industry, at 28.1x. Compared to its peer average of 43.0x, VeriSign looks relatively less expensive. However, a more precise valuation tool is Simply Wall St’s proprietary Fair Ratio, calculated as 30.0x for VeriSign. The Fair Ratio incorporates crucial factors such as forecasted earnings growth, risk profile, profit margins, company size, and sector dynamics to estimate the right multiple for this specific business.

With VeriSign’s current PE of 28.8x sitting just below its Fair Ratio of 30.0x, it suggests the stock is fairly valued on this metric and priced about right for its prospects and quality.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1437 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your VeriSign Narrative

Earlier, we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is more than just numbers. It is your story or perspective about a company’s future, connecting your assumptions for revenue growth, earnings, and margins to a fair value calculation. Narratives turn investment research into something practical and interactive, letting you visualize how your beliefs about a company shape your view of what it's worth, all in one place on Simply Wall St's Community page, used by millions of investors worldwide.

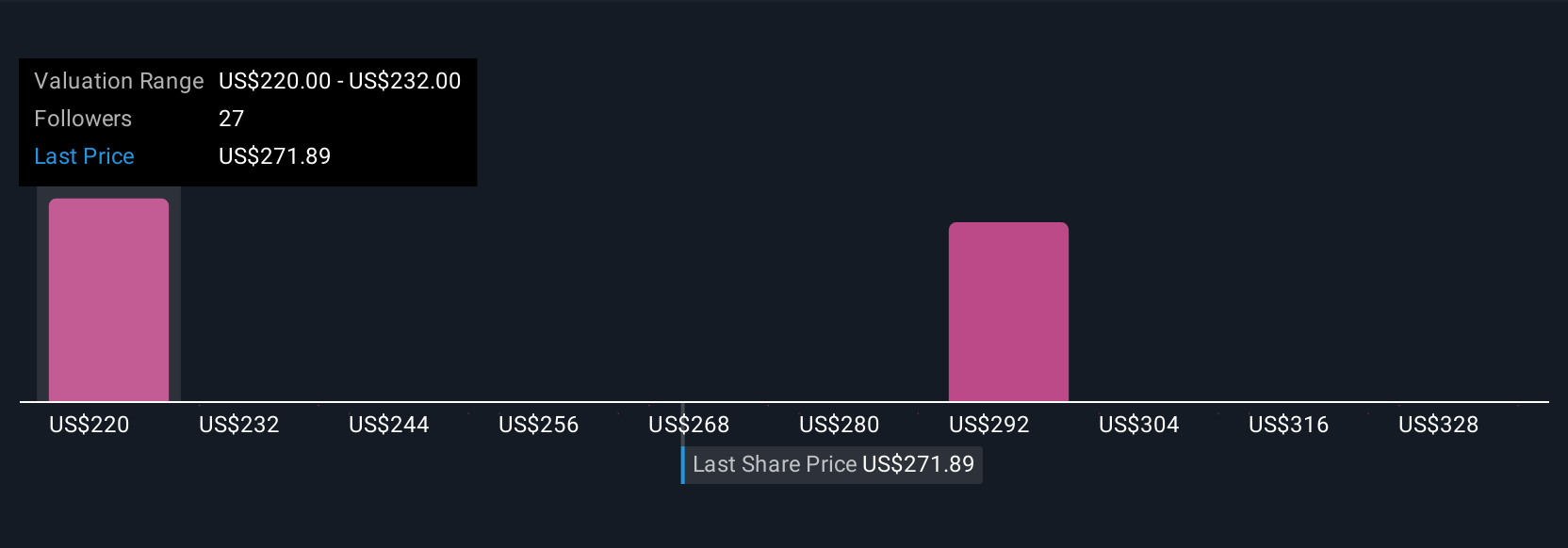

Narratives make it easy for investors to monitor when the fair value of a stock diverges from the actual market price, helping you decide if and when to buy or sell. They are automatically updated with new earnings, news, or data, ensuring your viewpoint stays current. For example, based on recent analyst forecasts for VeriSign, some investors see a fair value as high as $340, factoring in strong domain growth and new revenue streams, while others estimate just $250, due to more cautious assumptions about future profitability and industry risks. With Narratives, you can easily see the range of perspectives, compare them to your own, and make smarter, more informed investment decisions.

Do you think there's more to the story for VeriSign? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRSN

VeriSign

Provides internet infrastructure and domain name registry services that enables internet navigation for various recognized domain names worldwide.

Low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

934 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative