Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

Is Varonis Systems (NASDAQ:VRNS) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Varonis Systems, Inc. (NASDAQ:VRNS) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Varonis Systems

What Is Varonis Systems's Debt?

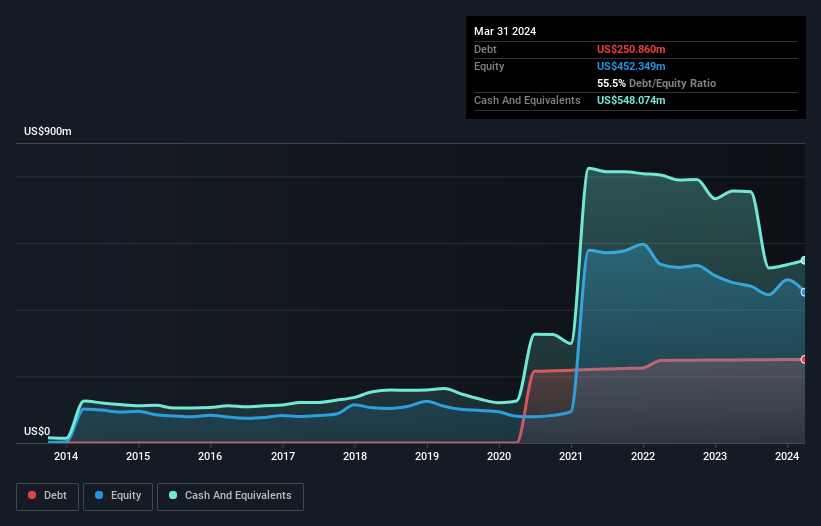

As you can see below, Varonis Systems had US$250.9m of debt, at March 2024, which is about the same as the year before. You can click the chart for greater detail. But on the other hand it also has US$548.1m in cash, leading to a US$297.2m net cash position.

A Look At Varonis Systems' Liabilities

The latest balance sheet data shows that Varonis Systems had liabilities of US$297.2m due within a year, and liabilities of US$304.1m falling due after that. On the other hand, it had cash of US$548.1m and US$100.4m worth of receivables due within a year. So it actually has US$47.2m more liquid assets than total liabilities.

Having regard to Varonis Systems' size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the US$5.13b company is struggling for cash, we still think it's worth monitoring its balance sheet. Succinctly put, Varonis Systems boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Varonis Systems's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Varonis Systems wasn't profitable at an EBIT level, but managed to grow its revenue by 4.4%, to US$506m. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Varonis Systems?

While Varonis Systems lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow US$75m. So although it is loss-making, it doesn't seem to have too much near-term balance sheet risk, keeping in mind the net cash. We'll feel more comfortable with the stock once EBIT is positive, given the lacklustre revenue growth. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Varonis Systems , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

136 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.3% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

PI

PittTheYounger on Cathay Pacific Airways ·

Cathay Pacific well-placed in growth markets, but at risk from US-China trade war

Fair Value:HK$11.984.4% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ID

Idle on Viper Energy ·

Sold 44.5, Great dividend but share numbers have increased 100% in last 12 months!!

Fair Value:US$3238.3% overvalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EN

enatega on Advanced Micro Devices ·

Open Source Online Order Systems: A Complete Guide

Fair Value:US$319.7739.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1310 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0