Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

Evaluating Varonis (VRNS) After New Microsoft and AWS Security Integrations Reshape Its Data Protection Story

Varonis Systems (VRNS) is back on radar after rolling out fresh integrations with Microsoft Purview and AWS Security Hub, tightening its grip on data security just as AI driven workloads raise new risk questions.

See our latest analysis for Varonis Systems.

Those Purview and AWS Security Hub integrations land at a tricky moment for investors. The latest 1 day share price return of 2.98 percent to 32.47 dollars comes after a steep 90 day share price return decline of 43.22 percent and a 1 year total shareholder return of negative 32.37 percent, even though the 3 year total shareholder return is still up 35.18 percent. This hints that momentum has clearly faded in the short term, but the longer term story is not completely broken.

If this kind of security focused AI story interests you, it might be worth scanning other software names by exploring more high growth tech and AI stocks that could be riding similar demand trends.

With revenue still growing double digits but margins under pressure, and the stock trading at a steep discount to analyst targets, is Varonis now mispriced by wary investors, or is the market already baking in its next leg of growth?

Most Popular Narrative Narrative: 38.3% Undervalued

With Varonis Systems last closing at 32.47 dollars against a narrative fair value of about 52.63 dollars, the valuation debate turns on how aggressively future growth is being priced in.

Continued SaaS transition and high NRR (notably for SaaS customers), combined with robust upsell momentum across cloud and multi-cloud environments, enhance ARR visibility and predictability, driving durable earnings and margin expansion as the SaaS mix climbs and operational leverage improves post-transition.

Want to see the math behind that confidence? The narrative leans on rapid recurring revenue gains, rising margins, and a punchy future earnings multiple. Curious how those moving parts stack up into that higher fair value? Read on to unpack the projections driving this upside case.

Result: Fair Value of $52.63 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slower on-premise renewals and execution risk around the SaaS migration could derail those upbeat assumptions and cap near-term upside.

Find out about the key risks to this Varonis Systems narrative.

Another Lens on Valuation

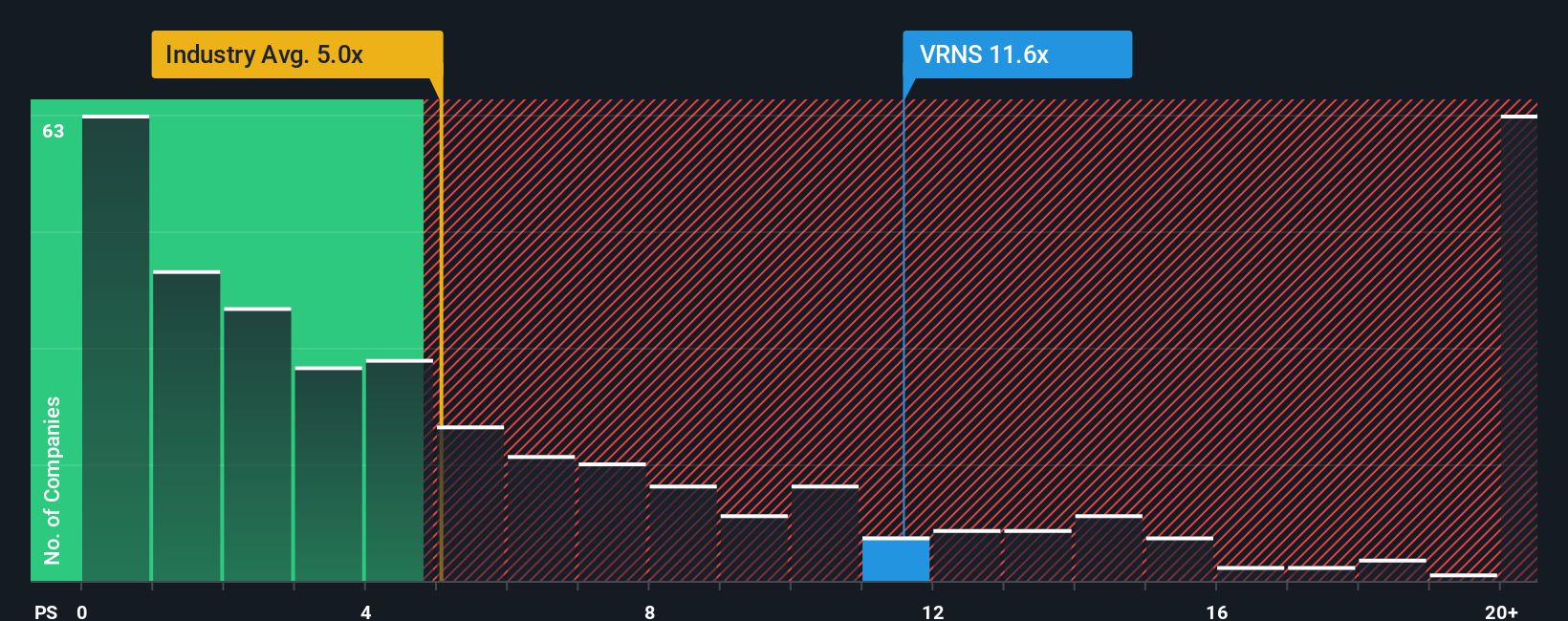

Price to sales tells a different story. Varonis trades around 6.3 times sales, richer than both US software peers at 4.9 times and its own 6 times fair ratio, hinting that even after the sell off, multiple compression risk has not fully cleared. Could the pessimism actually deepen?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Varonis Systems Narrative

If this view does not fully resonate, or you prefer digging into the numbers yourself, you can easily build a custom narrative in minutes: Do it your way.

A great starting point for your Varonis Systems research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Do not stop at one stock story. Sharpen your edge by using Simply Wall Street's screener to spot fresh, data backed opportunities before others react.

- Capitalize on market mispricing by targeting companies trading below their fundamentals using these 897 undervalued stocks based on cash flows to hunt for potential value winners.

- Ride structural growth in cutting edge automation and analytics by scanning these 26 AI penny stocks for businesses powering the next wave of intelligent software.

- Lock in potential long term income streams by reviewing these 15 dividend stocks with yields > 3% that can strengthen your portfolio's cash flow through reliable payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

143 followersusers have followed this narrative

1 commentusers have commented on this narrative

24 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k22.4% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9421.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87177.0% overvalued

3 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Red Cat Holdings ·

Red Cat Holdings (RCAT): The Small-Drone Contender Bracing for Q4 Impact

Fair Value:US$18.458.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Micron Technology ·

Micron Technology Inc. (MU): The "Silicon Gold" Rush Reaches a Fever Pitch

Fair Value:US$4956.7% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Jabil ·

Jabil Inc. (JBL): The AI "Picks and Shovels" Play Ahead of Earnings

Fair Value:US$295.511.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.8% undervalued

54 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9824.4% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.0% undervalued

1312 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0