- United States

- /

- Diversified Financial

- /

- NasdaqGS:PYPL

PayPal (NASDAQ:PYPL) Remains a Growth Story in Face of Rising Competition

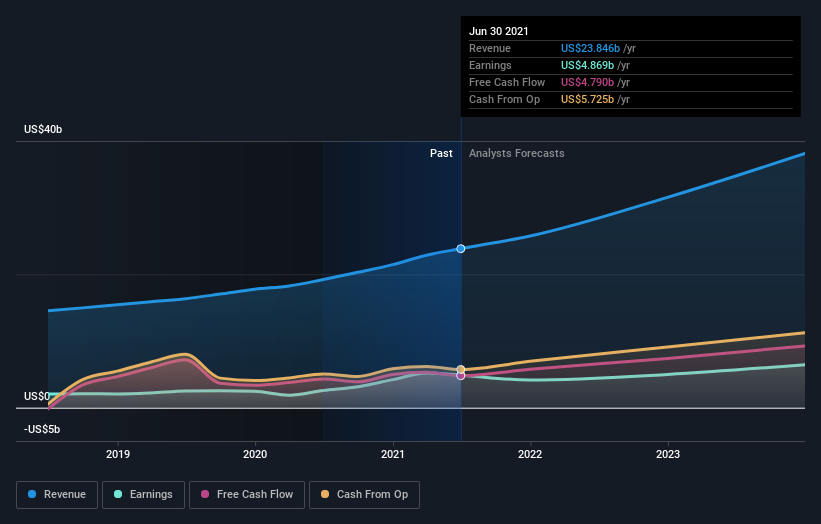

PayPal Holdings, Inc. ( NASDAQ:PYPL ) is one of the companies that quickly reversed the 2020 downturn, tripling up within a year, to reach the impressive US$322b valuation.

Yet, the stock is looking a bit expensive at a price-to-earnings (P/E) ratio of 66. As it pays no dividend, the premise relies on the strong growth trend continuing in the future.

The most recent earnings report performed in consensus:

- Revenue: US$6.2b, growth 18.6% y/y

- EPS: US$1.15, growth 7% y/y

- Q3 guidance: US$6.15b to US$6.25b (consensus US$6.45b)

- Q3 EPS: US$1.07 (estimate US$1.14)

The market certainly didn't like the softer Q3 guidance as the stock dropped 10% since the earnings.

The rising competition didn't help the cause either after Square announced an agreement to buy Afterpay . With a US$29b acquisition, Square is entering the lucrative „buy now pay later“ segment, integrating it into an existing platform.

Meanwhile, Paypal is expanding in the crypto market, introducing Cash Back to Crypto . This feature allows Venmo credit cardholders to purchase cryptocurrencies by using the earned cashback automatically. A few weeks back, PayPal raised cryptocurrency purchase limit s for U.S customers to US$100k per week.

View our latest analysis for PayPal Holdings

Is PayPal Holdings still cheap?

The stock seems fairly valued at the moment, according to our valuation model. It's trading around 17.27% above our intrinsic value, which means if you buy PayPal Holdings today, you'd be paying a relatively reasonable price for it. And if you believe the company's actual value is $233.97, there's only a minor downside when the price falls to its real value.Although, there may be an opportunity to buy in the future. This is because the beta (a measure of share price volatility) is high, meaning its price movements will be exaggerated relative to the rest of the market.

If the market is bearish, the company's shares will likely fall by more than the rest of the market, providing a buying opportunity.

Can we expect growth from PayPal Holdings?

Investors looking for growth in their portfolio may want to consider a company's prospects before buying its shares. Buying a great company with a robust outlook at a low price is always a good investment, so let's also look at the company's future expectations.PayPal Holdings' earnings over the next few years are expected to increase by 41%, indicating a highly optimistic future ahead. This should lead to more robust cash flows, feeding into a higher share value.

Yet, with the user growth that seems to be only accelerating, those numbers indeed remain a possibility.

What this means for you:

Are you a shareholder?It seems like the market has already priced in PYPL's positive outlook, with shares trading around their fair value. However, there are also other important factors which we haven't considered today, such as the track record of its management team. Have these factors changed since the last time you looked at the stock? Will you have enough conviction to buy should the price fluctuates below the true value?

Are you a potential investor? If you've been keeping tabs on PYPL, now may not be the most advantageous time to buy, given it is trading around its fair value. However, the positive outlook is encouraging for the company, which means it's worth further examining other factors such as the strength of its balance sheet to take advantage of the next price drop.

So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. While conducting our analysis, we found that PayPal Holdings has 2 warning signs , and it would be unwise to ignore them.

If you are no longer interested in PayPal Holdings, you can use our free platform to see our list of over 50 other stocks with high growth potential.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NasdaqGS:PYPL

PayPal Holdings

Operates a technology platform that enables digital payments for merchants and consumers worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion