Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGS:PYPL

PayPal (NASDAQ:PYPL) is still Optimistically Valued after recent price Weakness

Yesterday, PayPal Holdings, Inc. ( NASDAQ:PYPL ) responded to last week’s rumors of a potential acquisition of Pinterest with a one-line press release . The press release simply stated: ‘In response to market rumors regarding a potential acquisition of Pinterest by PayPal, PayPal stated that it is not pursuing an acquisition of Pinterest at this time.’ While this statement doesn’t rule out a deal in the future, it certainly implies there will not be a deal any time soon.

Last week the share price fell as much as 11% as a result of the rumor. Yesterday it recovered some of those losses, but it remains 20% below the all-time high of $310. This is a significant correction for a stock that is up more than 500% over the last five years and it's worth considering the potential opportunity PayPal now offers.

What is PayPal Holdings worth?

Our analysis of PayPal includes an estimate of its fair value which works out to $244 - just 1.6% below the current price. This estimate is based on the average cash flow forecasts from 13 analysts - so it will change as these forecasts change.

To get a sense of the current valuation in relative terms we can consider the price-to-earnings (or "P/E") ratio, which is 58x. This is a lot higher than the equity market (18X) and the American IT Industry (35.1x). PayPal’s P/E ratio implies that investors are still very optimistic about the company’s growth compared to the market. This means that if growth doesn’t outpace the broader market, the stock might not be able to maintain such a high price multiple.

What kind of growth will PayPal Holdings generate?

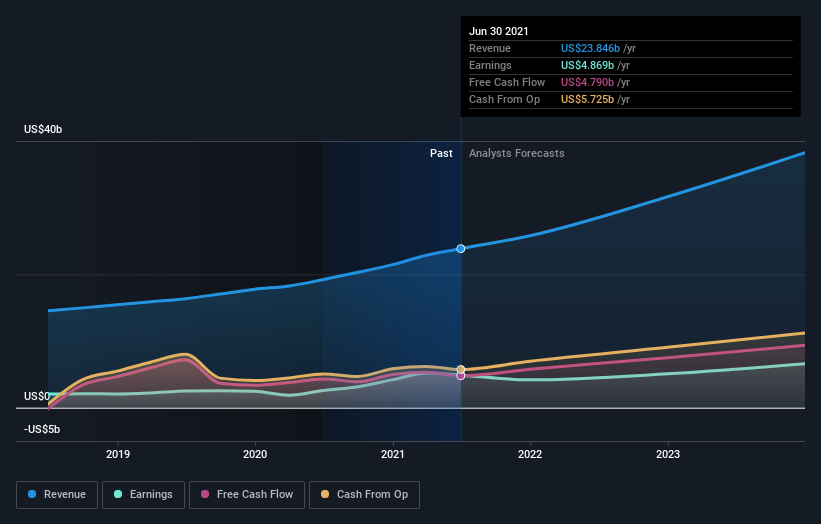

Considering PayPal’s historical and likely future growth, gives some perspective to the current valuation. Between 2013 and 2019, revenue growth ranged between 15 and 20%. In the last 18 months, this growth has accelerated to 24%, and even reached 30.6% in the first quarter this year - before dropping back to 18% in the second quarter.

In addition to the recent acceleration in revenue growth, PayPal’s profit margin has also widened over the last year, which results in net income growth of 88.5%.

Analysts now expect earnings growth of 20 to 25% over the next few years on revenue growth of 20 to 22%.

What does this mean for Investors?

PayPal is arguably the world’s leading fintech company, and its future remains bright. But there is a limit to the valuation it can trade on, and investors now have an expanding list of rapidly growing, smaller fintech companies to choose from.

Despite the 20% correction, the current valuation implies investors are still expecting significant outperformance. This may become a problem if the company cannot maintain the current trajectory or if margins revert to per-2020 levels.

The next set of quarterly results will be announced on the 8th November, and analysts are expecting revenue of $6.2 billion and EPS of $1.08. To maintain investor confidence, the company really needs to match or beat these numbers. Future guidance will also be key when these results are released.

Our full PayPal analysis includes the valuation and growth forecasts - the data is updated daily and any changes to analyst forecasts will be reflected soon after they are made.

If you are no longer interested in PayPal Holdings, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NasdaqGS:PYPL

PayPal Holdings

Operates a technology platform that enables digital payments for merchants and consumers worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1947.9% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7719.6% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19017.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

TH

TheTurntTomato on Constellium ·

CSTM: A High-Barrier Aerospace and EV Materials Leader Trading at Just 9x Earnings

Fair Value:US$37.1625.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

TheTurntTomato on PicS ·

A Fast-Growing Fintech Priced Like a Slow-Growth Bank

Fair Value:US$20.442.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

TheTurntTomato on Canadian Solar ·

Why CSIQ Could Be One of the Market's Most Misunderstood Renewable Energy Stocks

Fair Value:US$18.0515.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.0% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.4% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.6% undervalued

65 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0