Advertisement

- United States

- /

- Software

- /

- NasdaqGS:PONY

Pony AI (PONY): Valuation in Focus Following Major Partnerships and Hong Kong Dual Listing

Simply Wall St

Reviewed by Simply Wall St

Pony AI (NasdaqGS:PONY) has sparked fresh interest following a string of important events. These include a new Bolt partnership for European expansion, breakthroughs in its Gen-7 Robotaxi fleet, and a major Hong Kong dual listing that raised more capital.

See our latest analysis for Pony AI.

Momentum is building around Pony AI, with breakthroughs in both its robotaxi services and new partnerships fueling optimism despite some recent turbulence. After a steep 27.8% drop in its 30-day share price return, excitement over expansion plans and fresh capital has helped the latest share price rebound toward $13.33. This brings a 1-week share price return close to 7% as investor confidence strengthens for the road ahead.

If the flurry of activity in autonomous tech has sparked your interest, consider taking the next step and explore See the full list for free..

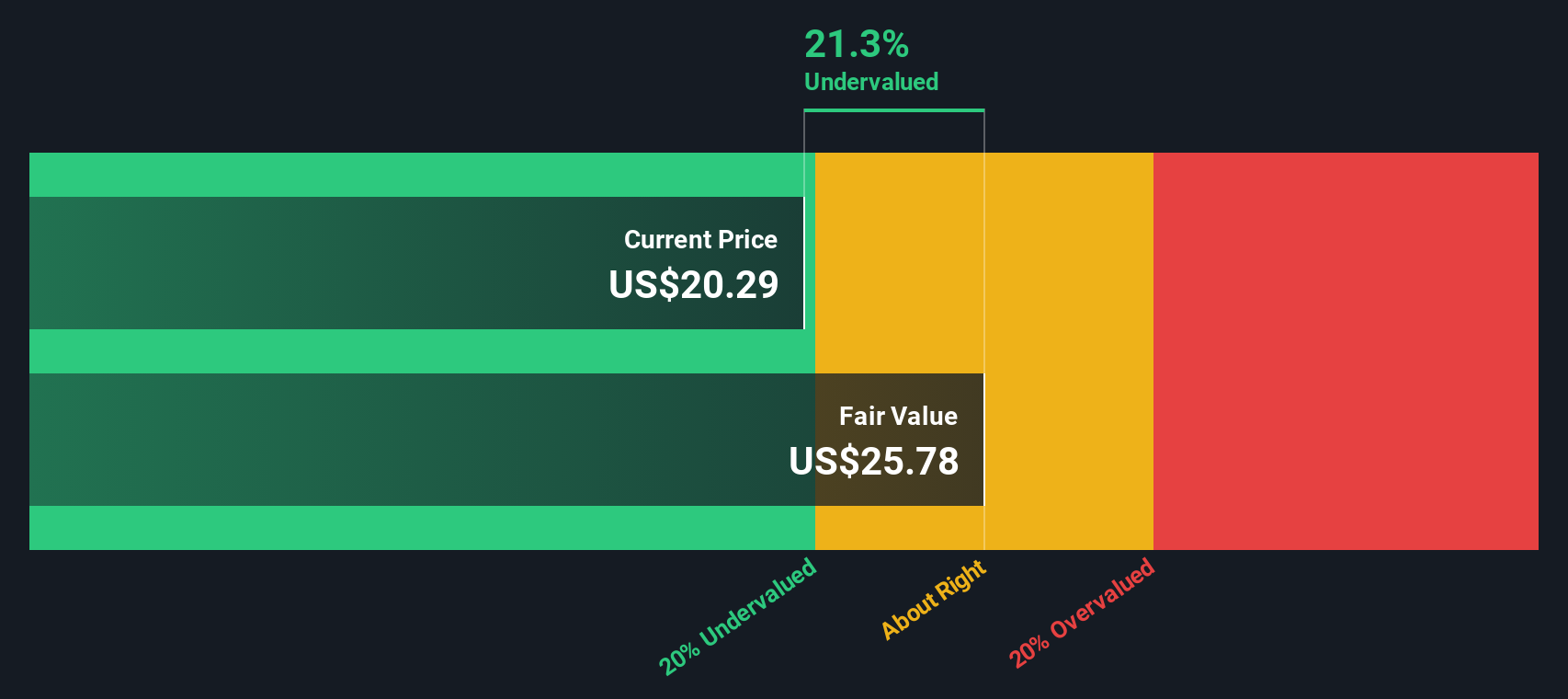

Pony AI’s rapid expansion, strong revenue growth, and ambitious international partnerships raise the key question for investors: does the current price reflect all this future potential, or is there still real value on the table?

Price-to-Book Ratio of 6.8x: Is it justified?

Pony AI is trading at a price-to-book (P/B) ratio of 6.8x, compared to the US Software industry average of 3.4x. At the last close of $13.33, this signals the market is putting a premium on Pony AI’s future potential and assets relative to peers.

The price-to-book ratio measures how much investors are willing to pay for each dollar of the company's net assets. In the context of a high-growth, capital-intensive sector like autonomous driving, a P/B above the industry norm may reflect strong expectations for future growth, unique technology, or brand value not captured on the balance sheet.

For Pony AI, the current P/B ratio stands well above the industry average. This premium suggests the market expects significant value creation, likely tied to its rapid revenue growth and aggressive expansion strategy. However, keep in mind that Pony is still unprofitable, and its P/B multiple exceeds the typical level for US Software companies. If regression-based fair value benchmarks were available, they would serve as the next reference point for the market.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 6.8x (OVERVALUED)

However, rapid expansion can strain operational control, and ongoing losses highlight the challenge of achieving consistent profitability in a competitive autonomous driving sector.

Find out about the key risks to this Pony AI narrative.

Another View: DCF Model Suggests Deep Value

While the price-to-book ratio presents Pony AI as expensive compared to software peers, our DCF model presents a different perspective. Using long-term forecasted cash flows, the SWS DCF model estimates Pony’s fair value at $50.72, nearly four times higher than its current price. Is the market overlooking something about Pony AI’s future, or is the model too optimistic in a fast-changing sector?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Pony AI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 933 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Pony AI Narrative

If you have a different perspective or would like to dig into the details yourself, you might consider building your own view in just a few minutes with Do it your way.

A great starting point for your Pony AI research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Stay ahead of the crowd and expand your investment horizons by checking out carefully curated lists that highlight unique opportunities. Don’t let the next big winner pass you by.

- Tap into future healthcare breakthroughs and uncover these 30 healthcare AI stocks targeting medical innovation and AI-powered solutions.

- Harness the potential of digital currency adoption by examining these 81 cryptocurrency and blockchain stocks changing the landscape of blockchain and financial technology.

- Spot overlooked opportunities with strong fundamentals by browsing these 933 undervalued stocks based on cash flows focusing on value stocks that could be primed for gains.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PONY

Pony AI

Through its subsidiaries, engages in the autonomous mobility business in the People’s Republic of China, the United States, and internationally.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

135 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

83 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

923 followersusers have followed this narrative

5 commentsusers have commented on this narrative

22 likesusers have liked this narrative