Advertisement

- United States

- /

- Software

- /

- NasdaqGS:MTLS

Materialise NV's (NASDAQ:MTLS) P/E Is On The Mark

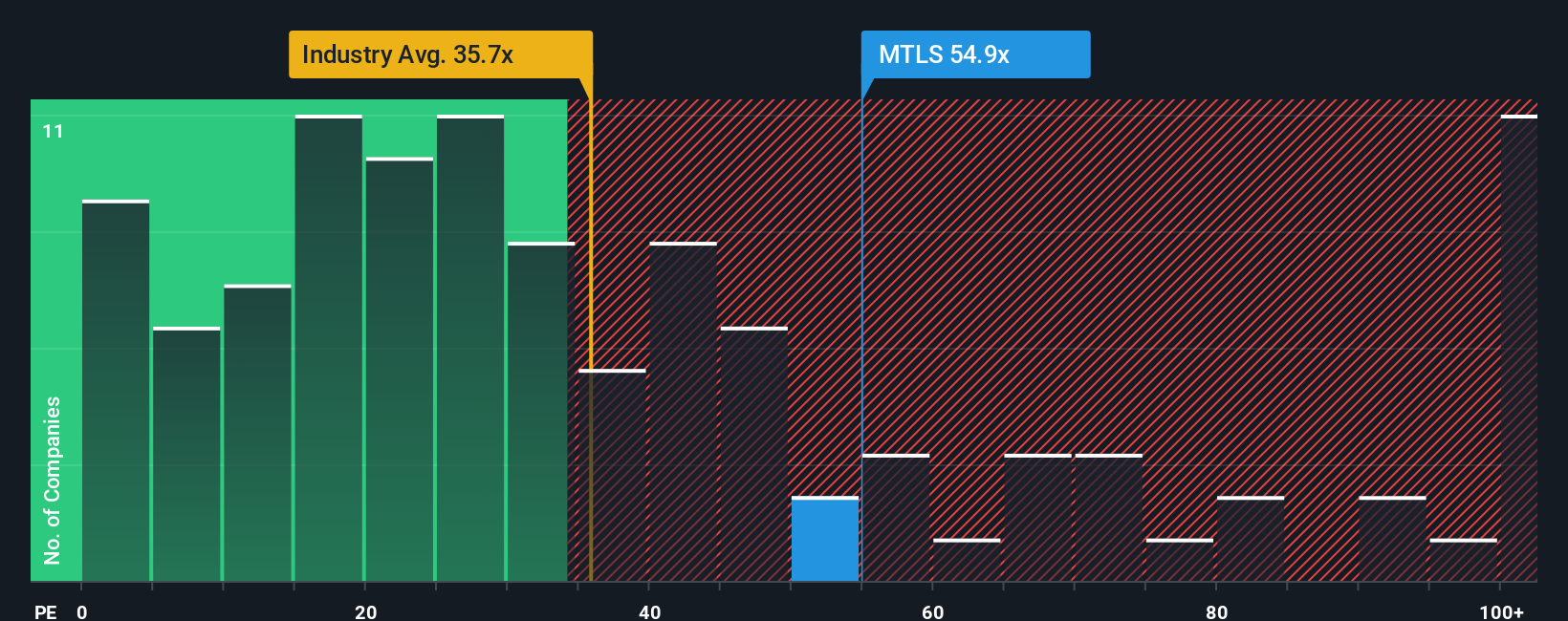

With a price-to-earnings (or "P/E") ratio of 54.9x Materialise NV (NASDAQ:MTLS) may be sending very bearish signals at the moment, given that almost half of all companies in the United States have P/E ratios under 19x and even P/E's lower than 11x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Materialise could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

See our latest analysis for Materialise

Is There Enough Growth For Materialise?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Materialise's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 49% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 61% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 56% each year during the coming three years according to the two analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 11% each year, which is noticeably less attractive.

In light of this, it's understandable that Materialise's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Materialise's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Materialise's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware Materialise is showing 1 warning sign in our investment analysis, you should know about.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:MTLS

Materialise

Provides additive manufacturing and medical software tools, and 3D printing services in the Americas, Europe, Africa, and the Asia-Pacific.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k45.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative