Advertisement

- United States

- /

- Software

- /

- NasdaqGS:MSFT

Microsoft Perplexity Deal Puts Azure Multi Model AI Strategy Under Scrutiny

Reviewed by Bailey Pemberton

- Microsoft (NasdaqGS:MSFT) has signed a multi year, US$750 million partnership with AI startup Perplexity.

- Perplexity will use Microsoft Azure's Foundry service to run models from OpenAI, Anthropic, and xAI on Azure infrastructure.

- The agreement highlights Azure's positioning as a multi model AI hosting platform rather than a channel for a single model provider.

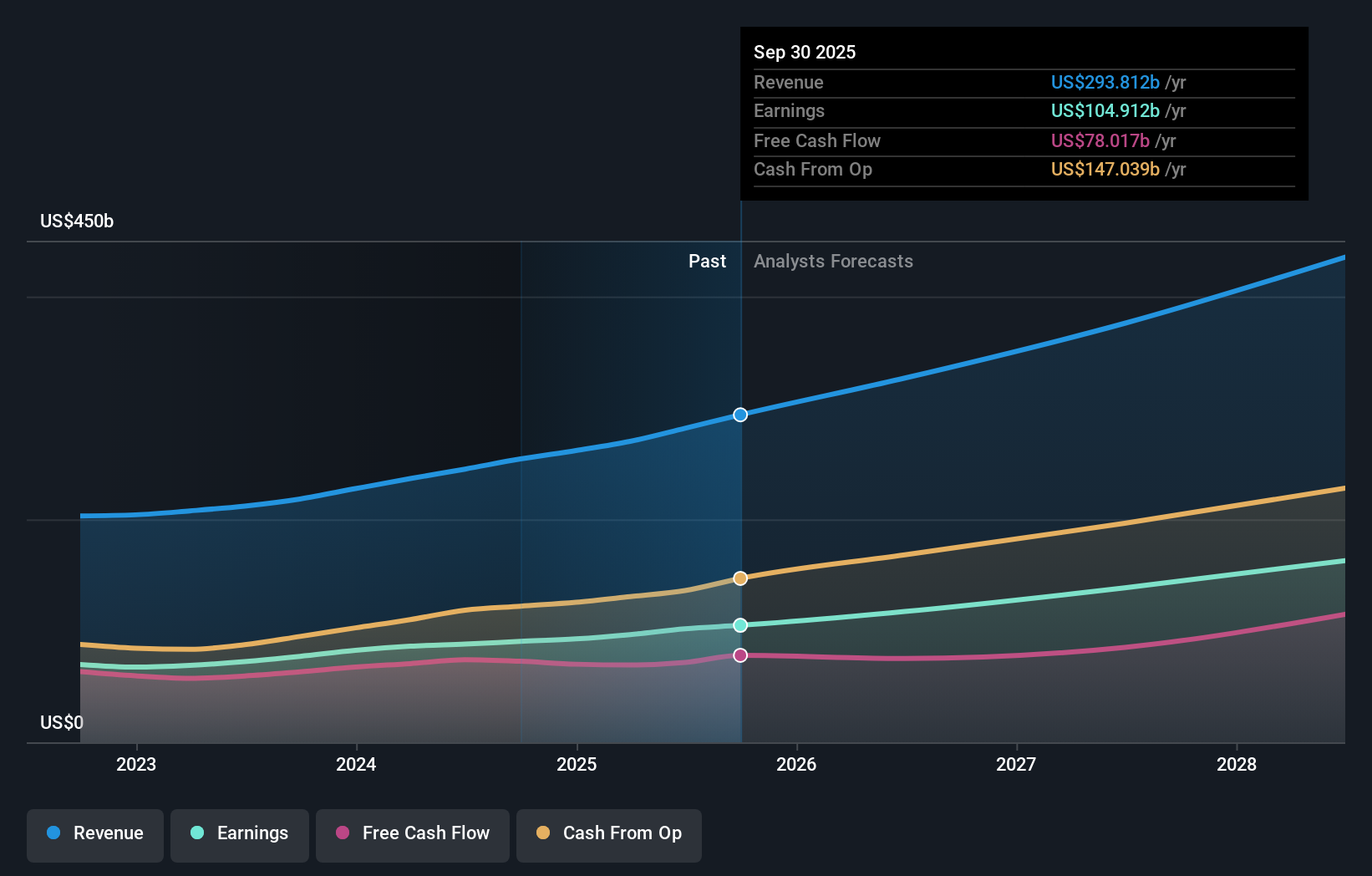

For you as an investor looking at Microsoft (NasdaqGS:MSFT), this deal sits at the intersection of cloud and generative AI, two areas that are central to the company’s long term strategy. Azure is providing computing power and also positioning itself as a neutral venue where different model providers can be accessed in one place. That can matter for customers that want flexibility across OpenAI, Anthropic, xAI and potentially others without committing to a single stack.

The Perplexity agreement also highlights key questions investors are asking about AI spending at Microsoft, including capital intensity, customer concentration and the timing of potential returns. As Azure signs more multi model workloads, the mix of customers and use cases using its AI infrastructure could become an important factor to watch, alongside headline figures on overall cloud demand.

Stay updated on the most important news stories for Microsoft by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Microsoft.

How Microsoft stacks up against its biggest competitors

Perplexity’s three year, US$750 million commitment signals that Microsoft is trying to turn Azure into a neutral, multi model hub where AI customers can mix and match models from OpenAI, Anthropic, xAI and others on one platform. For you, the key point is that this adds another large AI workload to Azure at a time when investors are closely watching how Microsoft converts heavy AI infrastructure spending into contracted usage, especially as rivals like Amazon Web Services and Google Cloud are also courting AI start ups and enterprises.

How this fits into the Microsoft AI narrative

The Perplexity deal lines up with the existing narrative that Microsoft wants Azure to be the default place enterprises build AI powered applications, on top of Copilot, GitHub and sector specific offerings in areas like healthcare and finance. It also slightly broadens the picture beyond OpenAI, which matters given recent concerns that a large share of Microsoft’s commercial backlog is tied to a single AI partner.

Risks and rewards investors should weigh

- Another committed AI customer helps support Azure usage at a time when commercial remaining performance obligations are already very large.

- Multi model access can make Azure more attractive versus Amazon and Google for companies that do not want to be locked into one AI stack.

- The economic value of the US$750 million depends on contract specific terms such as when capacity is available, which models are production ready and which regions can bill per token.

- Multi cloud setups like Perplexity’s use of both AWS and Azure can increase network and data egress costs, so margins on this type of workload are not guaranteed.

What to watch next

From here, it is worth tracking whether Microsoft discloses more large multi model Foundry deals, how quickly contracted commitments like this turn into reported Azure revenue, and whether customer concentration in OpenAI gradually eases. If you want to see how other investors are thinking about these trade offs, you can check community narratives on Microsoft through this dedicated page and compare different long term viewpoints against this new partnership.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MSFT

Microsoft

Develops and supports software, services, devices, and solutions worldwide.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

178 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k9.6% overvalued

24 followersusers have followed this narrative

1 commentusers have commented on this narrative

25 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$50013.5% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8563.4% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

FA

FA_Trader on Guan Huat Seng Holdings Berhad ·

Guan Huat Seng Holdings Berhad’s latest QR shows improving momentum, with stronger revenue, higher profit and first dividend

Fair Value:RM 0.3239.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SO

Souza123 on Inter & Co ·

Inter&Co - 60/30/30 Plan

Fair Value:US$33.374.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.6% undervalued

70 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9827.3% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.9% undervalued

56 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6433.7% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0