- United States

- /

- Software

- /

- NasdaqGS:MSFT

Microsoft (MSFT) Partners With Cerence For AI Integration In Vehicle Work Solutions

Microsoft (MSFT) recently collaborated with Cerence Inc. to launch a mobile work AI agent, enhancing vehicle integration with Microsoft 365 Copilot. This event coincided with the company's diverse strategic partnerships and product launches, such as Microsoft Azure OpenAI initiatives that further solidified its position in tech innovation. Over the last quarter, Microsoft's stock gained 5.11%, a move that aligns with broader market trends like optimism for interest rate cuts and tech sector resilience. Periodic corporate actions, like the announced quarterly dividend and share buybacks, added weight to these movements, reflecting overall investor confidence in Microsoft's growth trajectory.

We've discovered 1 weakness for Microsoft that you should be aware of before investing here.

The recent collaboration between Microsoft and Cerence Inc. aims to enhance vehicle integration with Microsoft 365 Copilot, potentially reinforcing Microsoft's key growth drivers in AI and cloud services. This alignment could bolster revenue streams as these technologies become increasingly embedded across Microsoft's offerings, such as Azure AI and Microsoft 365. As demand for integrated solutions rises, this collaboration might spur further top-line growth and could be a significant factor in meeting revenue and earnings forecasts. The focus on AI and subscription models supports expectations for sustained high-margin growth despite the high investment costs associated with expanding AI infrastructure.

Over the past five years, Microsoft's total shareholder returns, incorporating share price appreciation and dividends, reached 151.33%. This substantial growth reflects the company's successful capital allocation strategies and investor confidence. However, in the last year, Microsoft's stock performance lagged behind the broader US Software industry, which saw a higher return.

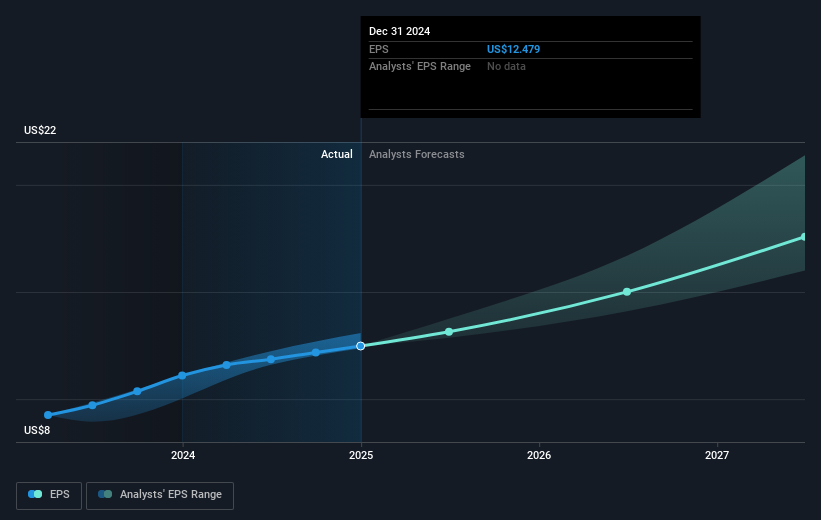

Currently, Microsoft's shares are trading at US$495.00, offering a noticeable discount of approximately 24% to the consensus analyst price target of US$613.89. This gap suggests potential room for appreciation if Microsoft's revenue and earnings growth align with projections. The analysts' consensus implies sustained belief in Microsoft's ability to manage high growth areas such as AI and cloud, which are pivotal to its future revenue streams. Investors should consider these factors when evaluating the potential upside against the current price level.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MSFT

Microsoft

Develops and supports software, services, devices, and solutions worldwide.

Very undervalued with outstanding track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

When GPS fails: this small cap is fixing a $54B drone problem

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Recently Updated Narratives

Building a 75/15/10 Income Machine with Schwab's Dividend ETF

Microsoft's Capex Bill Comes Due Before the AI Revenue Does

Future Growth Awaits NGXGROUP with New High-Profile Listings

Popular Narratives

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

A wonderful business at reasonable price.

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Trending Discussion

⏫42X THE AVERAGE DAILY TRADING VOLUME TODAY, JULY 28 🐂🐂🐂 FORTY-TWO!