Advertisement

- United States

- /

- IT

- /

- NasdaqGM:CMRC

Why Commerce.com (CMRC) Is Up 9.8% After BigCommerce Partnership Unlocks Embedded Payments Potential

- On September 16, 2025, Fortis announced a partnership with BigCommerce, powered by Commerce.com, to bring embedded payments technology and real-time transaction capabilities to a broad range of ecommerce merchants and developers.

- This collaboration aims to streamline payment processes, improve operational efficiency, and offer global payment support, significantly enhancing the Commerce.com platform’s value for growing businesses.

- We'll explore how integrating advanced payments with BigCommerce could reshape Commerce.com's investment prospects and growth drivers.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Commerce.com Investment Narrative Recap

To own Commerce.com stock, you need to believe the company can accelerate its modest revenue growth and overcome ongoing profitability challenges, despite a low valuation. The Fortis partnership introduces embedded payments and real-time transaction capabilities, supporting efficiency but its immediate impact on revenue growth, the key catalyst, remains to be seen; the main risk continues to be achieving substantial top-line expansion in a competitive sector.

Among recent announcements, the August 26 rollout of a headless ecommerce experience for Metrolinx stands out, highlighting Commerce.com’s ongoing integration of advanced payments and scalable solutions, key factors tied to growth catalysts such as product innovation and operational improvements.

On the other hand, investors should be mindful that despite exciting partnerships, Commerce.com's revenue trajectory...

Read the full narrative on Commerce.com (it's free!)

Commerce.com's narrative projects $383.7 million revenue and $24.4 million earnings by 2028. This requires 4.6% yearly revenue growth and a $45.4 million increase in earnings from -$21.0 million today.

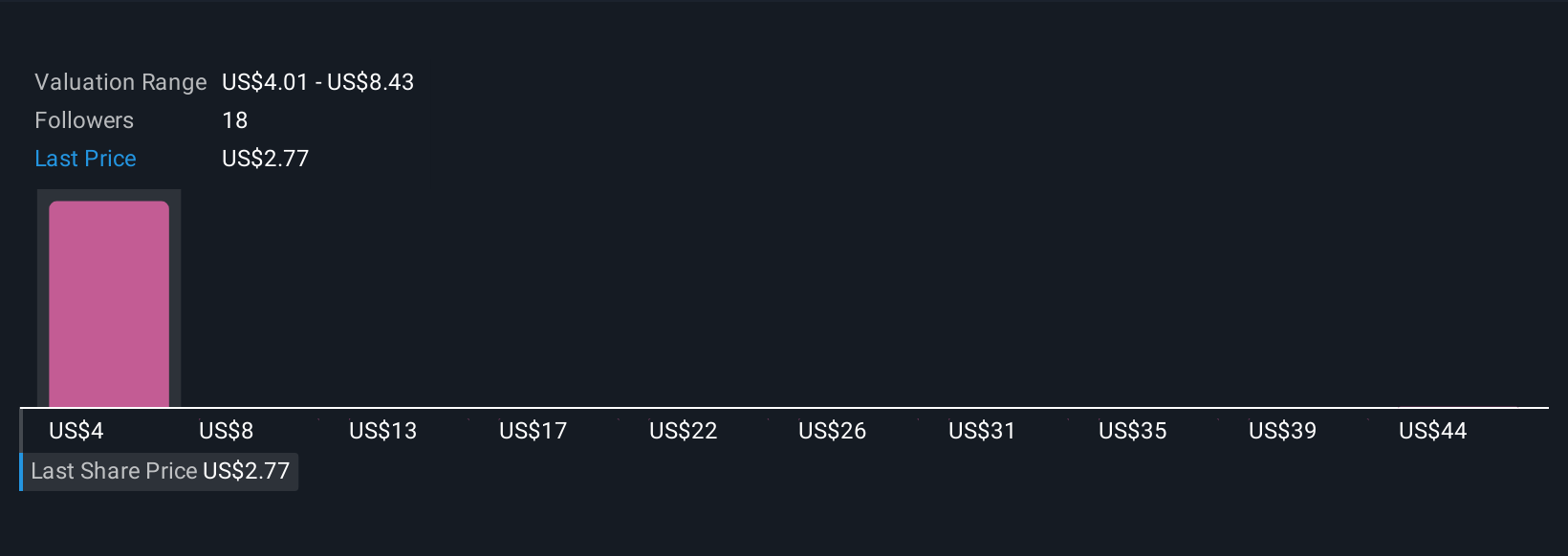

Uncover how Commerce.com's forecasts yield a $7.56 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided five unique fair value estimates for Commerce.com between US$4.01 and US$13.78 per share before the latest news. As many focus on the slow revenue growth, now is a good time to compare diverse opinions and see how new catalysts might shift your own outlook.

Explore 5 other fair value estimates on Commerce.com - why the stock might be worth over 2x more than the current price!

Build Your Own Commerce.com Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Commerce.com research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Commerce.com research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Commerce.com's overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Find companies with promising cash flow potential yet trading below their fair value.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:CMRC

Commerce.com

Provides artificial intelligence-driven commerce ecosystem in the United States, Europe, the Middle East, Africa, the Asia Pacific, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2537.9% undervalued

146 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0327.9% undervalued

32 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.521.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.726.3% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Oriental Kopi Holdings Berhad ·

Oriental Kopi's Indonesia JV Strengthens Regional Growth Narrative

Fair Value:RM 1.533.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on UCB ·

FV 206,24 but with a 310-154 range...to discuss

Fair Value:€206.249.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Figma ·

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value:US$22.367.2% overvalued

62 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28021.9% undervalued

260 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.0% overvalued

128 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6276.6% overvalued

139 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0