Advertisement

- United States

- /

- Software

- /

- NasdaqCM:CLSK

Is CleanSpark (CLSK) Pricing Reflecting Recent Share Pullback And Bitcoin Sentiment Swings

Reviewed by Bailey Pemberton

- If you are looking at CleanSpark and wondering whether the recent share price makes sense, this article will walk through what that could mean for the stock's current value.

- The share price closed at US$9.85 most recently, with returns of a 2.3% decline over 7 days, a 26.2% decline over 30 days, a 14.7% decline year to date, a 6.2% decline over 1 year and a very large 3 year gain that compares to a 72.9% decline over 5 years.

- Recent coverage around CleanSpark has focused on its position as a listed bitcoin miner and its exposure to changes in cryptocurrency sentiment, which can influence how investors view both risk and opportunity. Headlines often highlight how sensitive miners like CleanSpark can be to bitcoin price moves and regulatory discussions, which helps frame the recent swings in the share price.

- On our valuation checks, CleanSpark currently scores 2 out of 6, which suggests some areas where the stock looks undervalued and others where it does not. Next, we will compare several common valuation approaches for CleanSpark and then finish by looking at a more complete way to think about what the shares are really worth.

CleanSpark scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: CleanSpark Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return, to arrive at an estimate of what the business might be worth per share.

For CleanSpark, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is a loss of about US$1,423.62 million. Analyst input is limited, with a projected Free Cash Flow of US$8 million in 2027, and the remaining yearly figures out to 2035 are extrapolated by Simply Wall St. These ten year projections are all in US$ and mostly sit in the single digit million range, with some years forecast as losses.

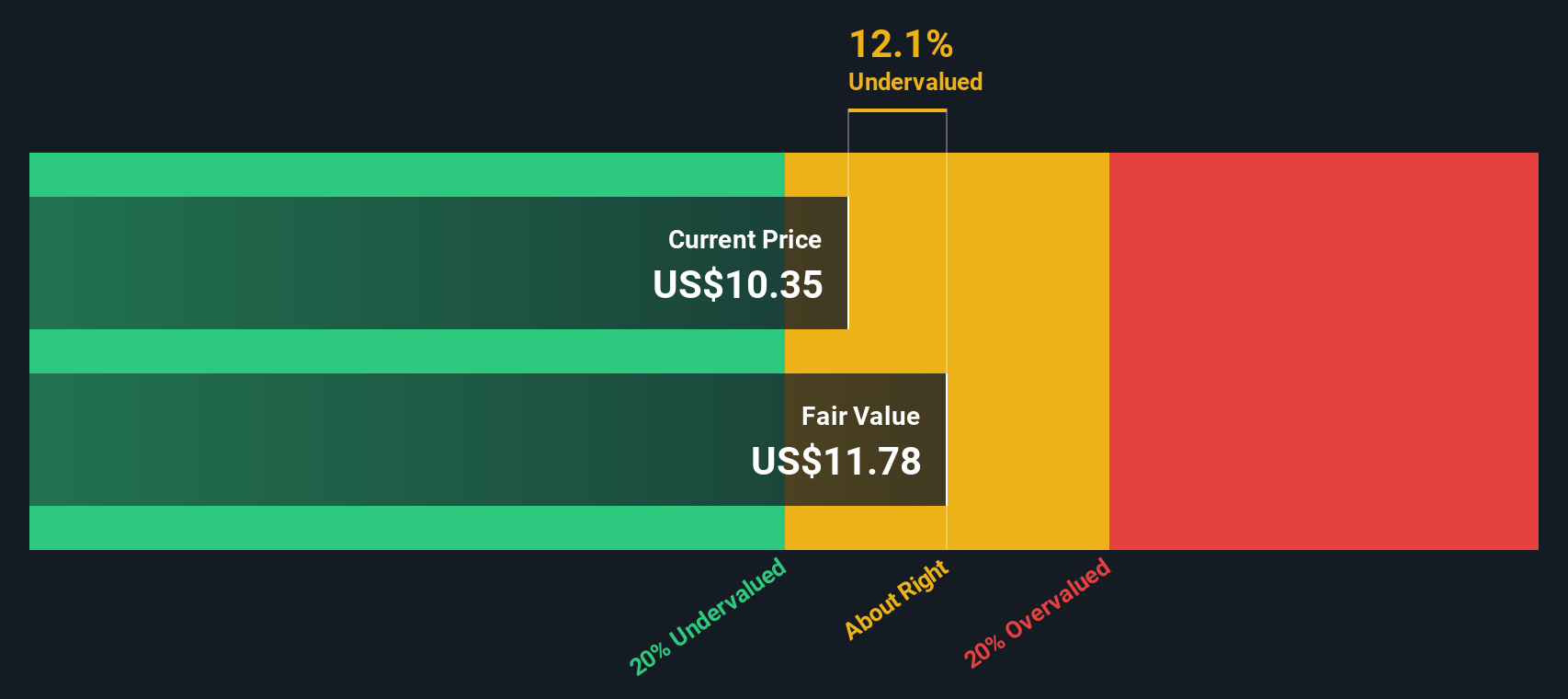

On this basis, the DCF model arrives at an estimated intrinsic value of about US$0.41 per share. Compared with the recent share price of US$9.85, this implies the stock is trading at a significant premium to the DCF estimate. In other words, the current price is far above what this cash flow model suggests.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CleanSpark may be overvalued by 2318.3%. Discover 53 high quality undervalued stocks or create your own screener to find better value opportunities.

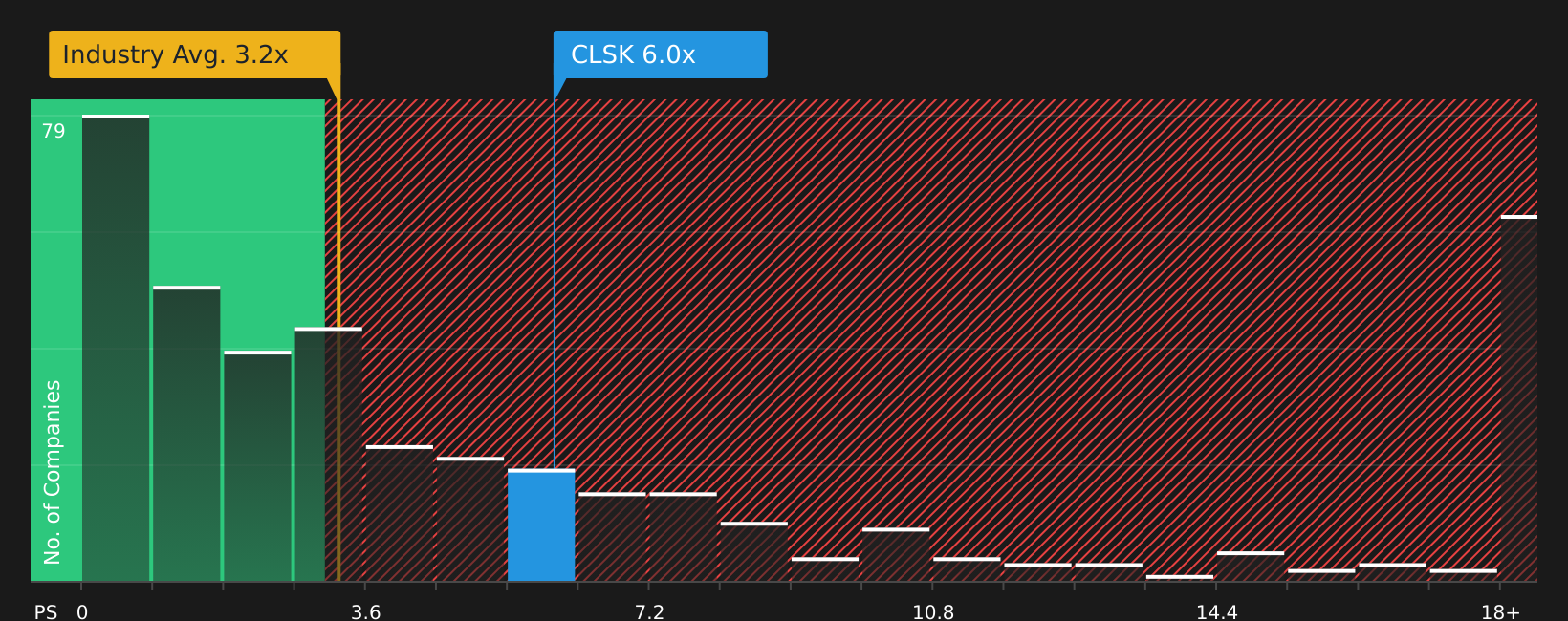

Approach 2: CleanSpark Price vs Sales

For companies where earnings and cash flows can be volatile, the P/S ratio is often a useful way to think about value, because it compares the share price to the revenue the business is generating rather than to profits that may swing around.

In general, investors tend to pay a higher P/S when they expect stronger growth and see lower risk, and a lower P/S when growth expectations are more modest or risks feel higher. So there is no single “right” multiple; it depends on what the market thinks the future could look like.

CleanSpark currently trades on a P/S of 3.21x. That sits a little below the Software industry average of 3.60x, while the broader peer group used here trades on an average of 24.10x, which is far higher. Simply Wall St’s Fair Ratio for CleanSpark is 3.19x, a proprietary estimate of what its P/S might be given factors such as earnings growth, industry, profit margin, market cap and risk profile. This tailored Fair Ratio can be more informative than a simple peer or industry comparison because it adjusts for company specific characteristics.

With the current P/S of 3.21x sitting very close to the Fair Ratio of 3.19x, the shares look priced at about the level this model would suggest.

Result: ABOUT RIGHT

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Upgrade Your Decision Making: Choose your CleanSpark Narrative

Earlier we mentioned that there is an even better way to understand valuation. Narratives on Simply Wall St let you attach a clear story about CleanSpark to the numbers by linking your view of its future revenue, earnings and margins to a financial forecast, a Fair Value estimate, and then a simple comparison with the current share price, all inside an easy tool on the Community page that millions of investors already use.

For CleanSpark, one Narrative might line up with the most optimistic analysts who see a Fair Value of US$30.00 and a higher future P/E of about 13.02x. Another might align with the most cautious view at roughly US$14.69 Fair Value and a future P/E of about 33.56x. Because Narratives update automatically as new news or earnings arrive, you can quickly see whether your Fair Value still justifies buying, holding or selling at today’s market price.

Do you think there's more to the story for CleanSpark? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:CLSK

CleanSpark

Operates as a bitcoin mining company in the Americas.

Low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0774.4% undervalued

218 followersusers have followed this narrative

1 commentusers have commented on this narrative

31 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

55 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0716.3% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3812.7% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on 5E Advanced Materials ·

5E Advanced Materials (FEAM): A Binary Critical Minerals Play with a $6.65 Fair Value Target

Fair Value:US$6.6577.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

53

537578 on Recursion Pharmaceuticals ·

Recursion Pharmaceuticals! WTH is going on?

Fair Value:US$1.9766.5% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Visa ·

Visa and the Case for Patience in Premium Businesses

Fair Value:US$2808.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.1% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

37 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.9% undervalued

1351 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

EL

Element1 on Greatland Resources ·

I can’t believe how inaccurate and out of date this site is—and people rely on it. Greatland owns tw...

0

|0

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0