Advertisement

- United States

- /

- Software

- /

- NasdaqCM:BTDR

Evaluating Bitdeer Technologies Group (NasdaqCM:BTDR) Valuation Following Debt Repayment and Power Plant Acquisition

Reviewed by Simply Wall St

If you are holding or eyeing shares of Bitdeer Technologies Group (NasdaqCM:BTDR), this week’s string of announcements probably has you weighing your next move. The company is cleaning up its balance sheet by redeeming all outstanding 8.50% convertible senior notes, and it is actively preparing to boost its war chest through a newly filed shelf registration. At the same time, Bitdeer’s acquisition of a 101-megawatt gas-fired power plant in Alberta marks a tangible step toward vertical integration in crypto mining. The combination of debt reduction, access to new growth capital, and power infrastructure expansion is clearly intended to signal stronger financial footing and more control over costs in an unpredictable industry.

All these moves come after a year that has been anything but boring for the stock. Despite recent volatility, Bitdeer has actually delivered impressive annual returns, jumping 122% over the past year. That rally stands in sharp contrast to a much steeper decline year to date, as short-term momentum has cooled, even as management posts steep annual gains in both revenue and net income. The market’s shifting perception seems to reflect both excitement about long-term potential and concerns about near-term risks such as dilution and industry volatility.

So after this rollercoaster year and the company’s latest financial maneuvers, is Bitdeer a bargain that the market is overlooking, or is future growth already priced in?

Most Popular Narrative: 41.9% Undervalued

The prevailing narrative sees Bitdeer Technologies Group as significantly undervalued, with a calculated fair value far above the current share price. Proponents of this perspective point to the company's ambitious growth plans and improving operating metrics as key catalysts for a potential re-rating.

"Bitdeer's development of proprietary ASIC technology is expected to create cost advantages and open opportunities in selling machines to penetrate the $4 billion to $5 billion annual ASIC market, which could drive significant revenue and margin improvements."

Curious how Bitdeer's bold strategic moves add up to such a high target? The most-followed valuation narrative hinges on aggressive financial projections that few other companies in the space dare to target. Want to know which radical earnings and margin goals are built into this outlook? Just how high do those ambitions run for the years ahead? The answers may challenge your expectations.

Result: Fair Value of $21.87 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, slower revenue growth and persistently high R&D costs could quickly challenge forecasts and unsettle even the strongest bull case for Bitdeer.

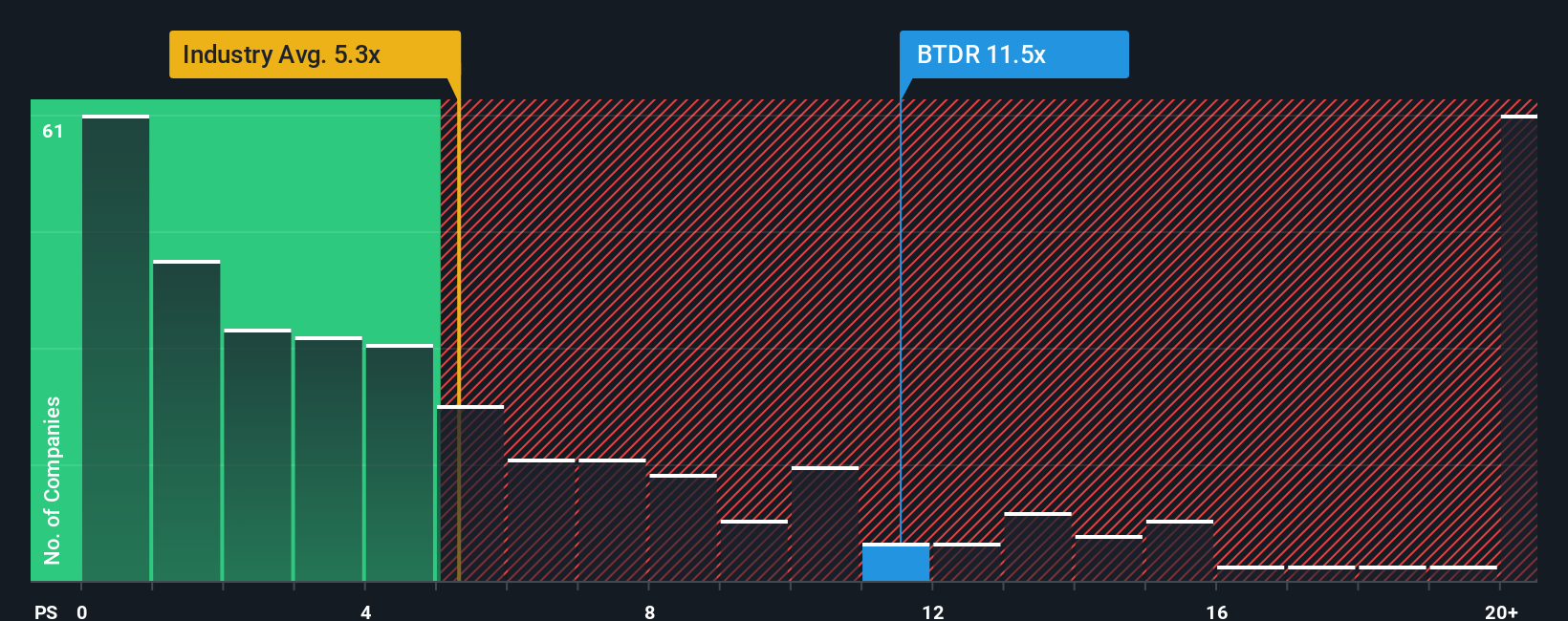

Find out about the key risks to this Bitdeer Technologies Group narrative.Another View: Multiples Paint a Different Picture

While fair value models suggest Bitdeer is seriously undervalued, a look at its revenue ratio compared to the broader software industry tells a more cautious story. Can multiple-based valuations reveal something the bulls are missing?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bitdeer Technologies Group Narrative

If you think there’s another angle or want to dig deeper into the numbers yourself, it’s quick and easy to shape your own view in just a few minutes. Do it your way.

A great starting point for your Bitdeer Technologies Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Level up your portfolio by checking out some high-potential stock opportunities you may not have considered. Don’t let these standout sectors and emerging trends pass you by. See what else could be driving the next wave of returns.

- Boost your income with reliable picks offering robust yields by searching among hand-picked dividend stocks with yields > 3%.

- Take advantage of undervalued gems that may be flying under the radar using our exclusive shortlist for undervalued stocks based on cash flows.

- Ride the AI momentum by targeting companies at the forefront of artificial intelligence breakthroughs via our expert-curated collection of AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bitdeer Technologies Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqCM:BTDR

Bitdeer Technologies Group

Operates as a technology company for blockchain and high-performance computing (HPC) in Singapore, the United States, Bhutan, Norway, Finland, Ethiopia, Canada, and internationally.

Slight risk with limited growth.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

47 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

WI

WisetoWealth on PayPal Holdings ·

The Underrated Transformation of a Digital Payments Giant

Fair Value:US$90.3137.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

Blagget on Terra Balcanica Resources ·

The C$4M Explorer Positioned to Become Europe's First Antimony Mine

Fair Value:CA$0.487.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_6nroa on Charter Communications ·

Charter is undervalued - Here's why.

Fair Value:US$87.0741.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

81 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

185 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

DE

derek_3wsdg on Teladoc Health ·

You’ve overlooked the activist investor factor. Travis Cocke’s Voss has announced 5% ownership through a 13G filing. They’ve added to that 5% since, and in doing so, have created a structural trap door for 27.42 Million Shares actively sold short. Chuck will announce lots of positives on July 29 but it’s what Voss announces shortly after that will rock the overextended Teledoc shorts. The Walmart partnership is the tip of the iceberg. The market is missing the sheer regulatory and enterprise friction of modern corporate healthcare. Teladoc isn't a "consumer app"; it is the primary digital infrastructure integrated directly into the legacy backends of Tier-1 insurance companies and fortune 500 employers, covering 105 million+ lives. Teladoc is acting as the digital top-of-funnel engine for the world's largest retailer. If Voss pushes the narrative that Teladoc is effectively the outsourced digital brain of Walmart's entire healthcare footprint, the fair value shifts from a basic health multiple to an enterprise distribution premium. Additionally , we are in a structural gold rush for high-quality, legally compliant, longitudinal medical data to train vertical healthcare AI models. Large technology hyperscalers and pharmaceutical giants cannot simply scrape the internet for this; they need structured clinical inputs. Teladoc sits on one of the largest de-identified virtual medical datasets on earth. From the activist playbook , we’ll see Voss demand the immediate creation of a Data & Diagnostics Licensing Division, transforming a legacy liability into an incredibly high-margin, pure-software data asset that requires zero human clinician hours to scale. Chuck is doing great work and deserves credi5 for the Teledoc turnaround but it will be Travis Cocke who will be responsible for a share price way beyond your $15 valuation.

1

|0