Advertisement

- United States

- /

- Software

- /

- NasdaqGS:AGYS

Does Agilysys Justify Its Premium Valuation After a 218% Five Year Surge?

Reviewed by Bailey Pemberton

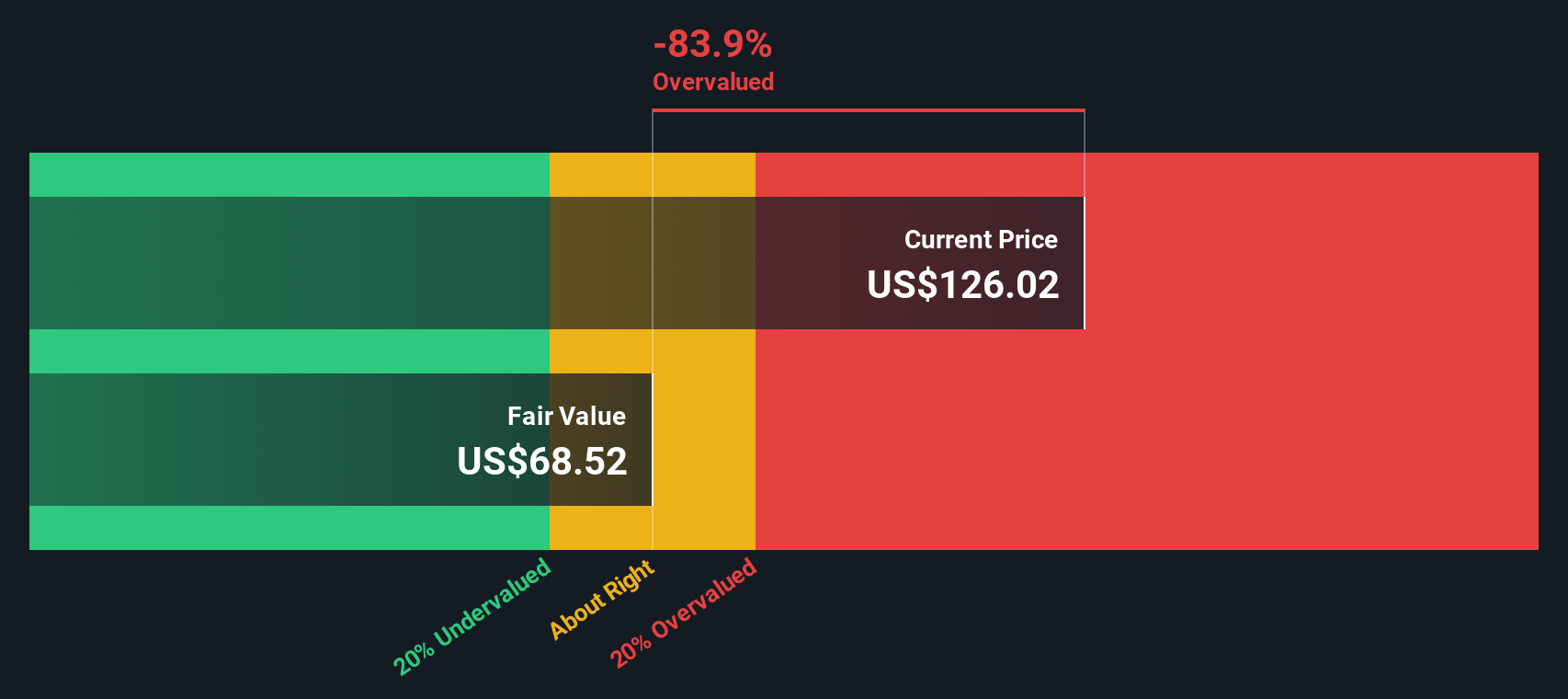

- Wondering if Agilysys at around $126 a share is a hidden opportunity or just fully priced in already? You are not alone, as this stock has been quietly attracting valuation minded investors.

- Over the very short term it has been a bit choppy, up 2.5% in the last week but roughly flat over 30 days, while still sitting on a 106.9% gain over 3 years and 217.7% over 5 years, even though it is down 2.8% year to date and 5.7% over the last year.

- Recent attention has centered on Agilysys as a niche software provider in hospitality and gaming technology, as investors debate how durable its growth runway is. Coverage has highlighted expanding demand for cloud based property management and point of sale platforms across hotels, casinos and resorts, reinforcing the idea that this is a quality growth story rather than a short term trading play.

- Despite that backdrop, our current valuation framework gives Agilysys a value score of 0/6, meaning it does not screen as undervalued on any of our six checks. Next we will unpack what each valuation lens is telling us and, at the end of the article, explore a more holistic way to judge whether the stock deserves its current price tag.

Agilysys scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Agilysys Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting the cash it could generate in the future and then discounting those cash flows back to the present. For Agilysys, this means looking at how much cash the company can return to shareholders over time in $.

Agilysys currently generates around $51.2 million in free cash flow, and analyst forecasts, combined with Simply Wall St extrapolations, suggest this could rise to about $142.7 million in 10 years. Those projections step up through the late 2020s, with forecast free cash flow of roughly $75.8 million by FY 2027 as the business scales.

When all those future cash flows are discounted using a 2 Stage Free Cash Flow to Equity model, the resulting intrinsic value is about $68.55 per share. Against a market price near $126, the model implies Agilysys is roughly 83.8% overvalued on a pure cash flow basis, suggesting expectations baked into the stock are very demanding.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Agilysys may be overvalued by 83.8%. Discover 906 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Agilysys Price vs Earnings

For profitable software businesses like Agilysys, the price to earnings, or PE, ratio is a useful shorthand for how much investors are willing to pay for each dollar of current earnings. Higher growth and lower perceived risk usually justify a higher PE, while slower or more uncertain growth should command a lower multiple.

Agilysys currently trades on a PE of about 144.3x, which is far richer than both the broader Software industry average of roughly 31.5x and the 38.4x average of its peers. To go a step further than these blunt comparisons, Simply Wall St uses a proprietary “Fair Ratio” framework that estimates what PE a company should trade on after accounting for factors like expected earnings growth, profitability, industry, market cap and specific risks.

For Agilysys, this Fair Ratio comes out at around 37.7x, suggesting that even after allowing for its attractive growth profile, the current 144.3x looks stretched. On this lens, the shares appear priced for very strong execution with little margin for error.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Agilysys Narrative

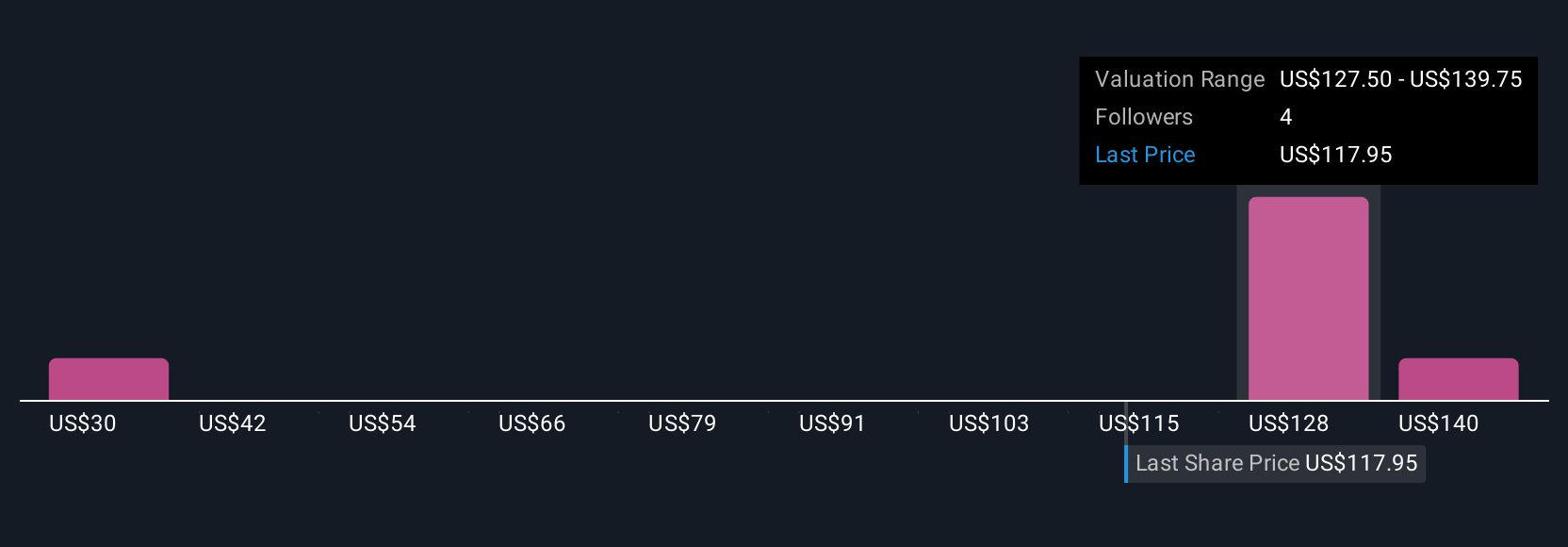

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you spell out your story for a company, link that story to a concrete forecast for revenue, earnings and margins, and then translate it into a fair value you can compare to today’s share price to help inform a decision to buy, hold or sell. The Narrative automatically updates as new news or earnings arrive. For Agilysys, one investor might believe its SaaS transition and AI features will drive strong global growth and assign a fair value near $152. A more cautious investor, worried about competition and margin pressure, might see fair value closer to $120. This shows how different but clearly defined perspectives can coexist and be weighed against the actual market price.

Do you think there's more to the story for Agilysys? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AGYS

Agilysys

Operates as a developer and marketer of software-enabled solutions and services to the hospitality industry in North America, Europe, the Asia-Pacific, and India.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

FU

FundamentalFlow on Vertiv Holdings Co ·

The Short and Long Term Compounder of Liquid Cooling industry.

Fair Value:US$45040.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2034.6% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on GQG Partners ·

The Cheap Genius Problem

Fair Value:AU$2.4541.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

Recently Updated Narratives

KL

Klim on PetroTal ·

PetroTal: Betting On a Production Recovery

Fair Value:CA$0.8542.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_1211213 on Robo.ai ·

Robo.ai (AIIO): A Long-Term Bullish Technical Setup

Fair Value:US$5.6443.6% undervalued

1 followerusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on Lagenda Properties Berhad ·

Lagenda Properties 录得创纪录销售额与收入,推动盈利能见度提升

Fair Value:RM 2.543.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

293 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

156 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

176 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

GE

george_b177x on Bloom Energy ·

Brilliant analysis. Great company with proven product and service!

0

|0