Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:ASYS

Amtech Systems, Inc. Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Predictions

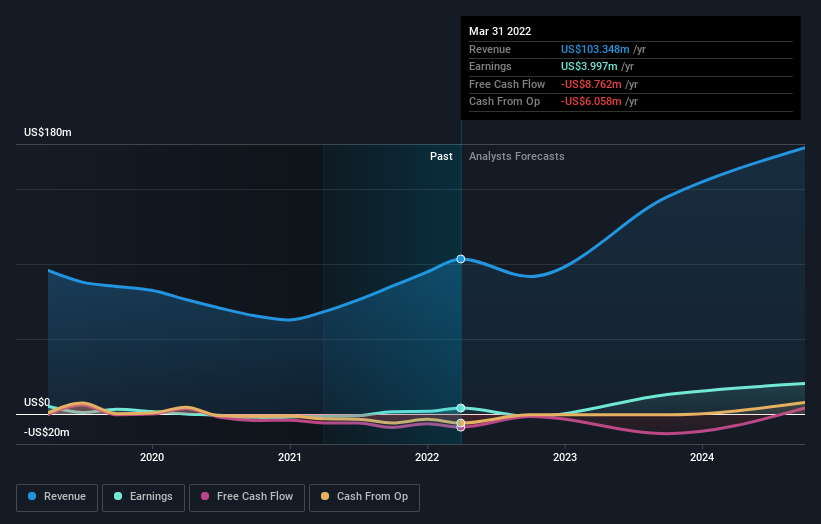

Amtech Systems, Inc. (NASDAQ:ASYS) defied analyst predictions to release its second-quarter results, which were ahead of market expectations. It was overall a positive result, with revenues beating expectations by 4.1% to hit US$29m. Amtech Systems also reported a statutory profit of US$0.14, which was an impressive 91% above what the analysts had forecast. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for Amtech Systems

After the latest results, the consensus from Amtech Systems' three analysts is for revenues of US$91.6m in 2022, which would reflect an uncomfortable 11% decline in sales compared to the last year of performance. Earnings are expected to tip over into lossmaking territory, with the analysts forecasting statutory losses of -US$0.10 per share in 2022. Before this earnings report, the analysts had been forecasting revenues of US$112.5m and earnings per share (EPS) of US$0.35 in 2022. So we can see that the consensus has become notably more bearish on Amtech Systems' outlook following these results, with a real cut to next year's revenue estimates. Furthermore, they expect the business to be loss-making next year, compared to their previous calls for a profit.

The average price target was broadly unchanged at US$16.33, perhaps implicitly signalling that the weaker earnings outlook is not expected to have a long-term impact on the valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Amtech Systems at US$18.00 per share, while the most bearish prices it at US$15.00. Still, with such a tight range of estimates, it suggeststhe analysts have a pretty good idea of what they think the company is worth.

Of course, another way to look at these forecasts is to place them into context against the industry itself. Over the past five years, revenues have declined around 13% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 21% decline in revenue until the end of 2022. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 9.5% per year. So it's pretty clear that, while it does have declining revenues, the analysts also expect Amtech Systems to suffer worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts are expecting Amtech Systems to become unprofitable next year. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target held steady at US$16.33, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Amtech Systems going out to 2024, and you can see them free on our platform here..

Even so, be aware that Amtech Systems is showing 2 warning signs in our investment analysis , and 1 of those shouldn't be ignored...

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ASYS

Amtech Systems

Manufactures and sells capital equipment and related consumables for use in fabricating and packaging semiconductor devices in the United States, Canada, Mexico, China, Malaysia, Taiwan, Singapore, the Czech Republic, Austria, Hungary, the United Kingdom, Germany, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7060.2% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.226.4% undervalued

35 followersusers have followed this narrative

7 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0542.8% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.9% undervalued

86 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Guanajuato Silver ·

Guanajuanto Silver, Hidden Gem of 1.8M Oz Producer + 75,000m Drilling = Huge Upside

Fair Value:CA$9.8495.2% undervalued

13 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.1621.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WI

Wizkhalifa on PSP Energy Berhad ·

PSP Energy Breaks Key Downtrend, Momentum Building for Further Upside

Fair Value:RM 0.09257.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9724.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1935.7% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0