Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGM:ACMR

ACM Research (ACMR): Revisiting Valuation Following Q3 Growth and Updated 2025 Revenue Guidance

Simply Wall St

Reviewed by Simply Wall St

ACM Research (ACMR) drew investor focus after releasing third quarter earnings that showed year-over-year growth in both sales and net income. The company also provided updated revenue guidance for fiscal year 2025.

See our latest analysis for ACM Research.

ACM Research’s updated guidance and robust Q3 results sparked added attention, though investor expectations appeared overheated in recent weeks. Despite a steep pullback with a 25% share price decline over the past month, the stock still boasts a 99.7% year-to-date share price gain and a remarkable 61.8% one-year total shareholder return. This momentum underscores both its growth potential and underlying volatility.

If strong performance streaks and quick shifts catch your attention, this is the perfect moment to broaden your investing perspective and discover fast growing stocks with high insider ownership

The question now is whether ACM Research’s impressive growth and guidance revisions have left room for further upside, or if the market has already factored in all the company’s future gains. This could leave little opportunity for new buyers.

Most Popular Narrative: 23.8% Undervalued

ACM Research is trading at $31.10, yet the most widely followed narrative suggests fair value is much higher. This striking valuation gap is anchored by bullish long-term growth assumptions and evolving margins.

Advanced digitalization and AI adoption are driving a surge in demand for next-generation semiconductor manufacturing. ACM's differentiated cleaning and plating solutions (such as its proprietary N2 bubbling and SPM tools) are positioned to capture increased orders as foundries invest in more complex 3D NAND, DRAM, and logic nodes, supporting long-term revenue growth.

Want to know which major drivers power this bullish price target? The narrative leans heavily on ambitious sales growth assumptions and expectations for sustained profit margins. Guess which core financial forecast is causing all the hype? Click to see how these projections build the foundation for the bold valuation.

Result: Fair Value of $40.81 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, overreliance on China's semiconductor market and uncertainty around U.S.-China export controls could quickly challenge these bullish outlooks.

Find out about the key risks to this ACM Research narrative.

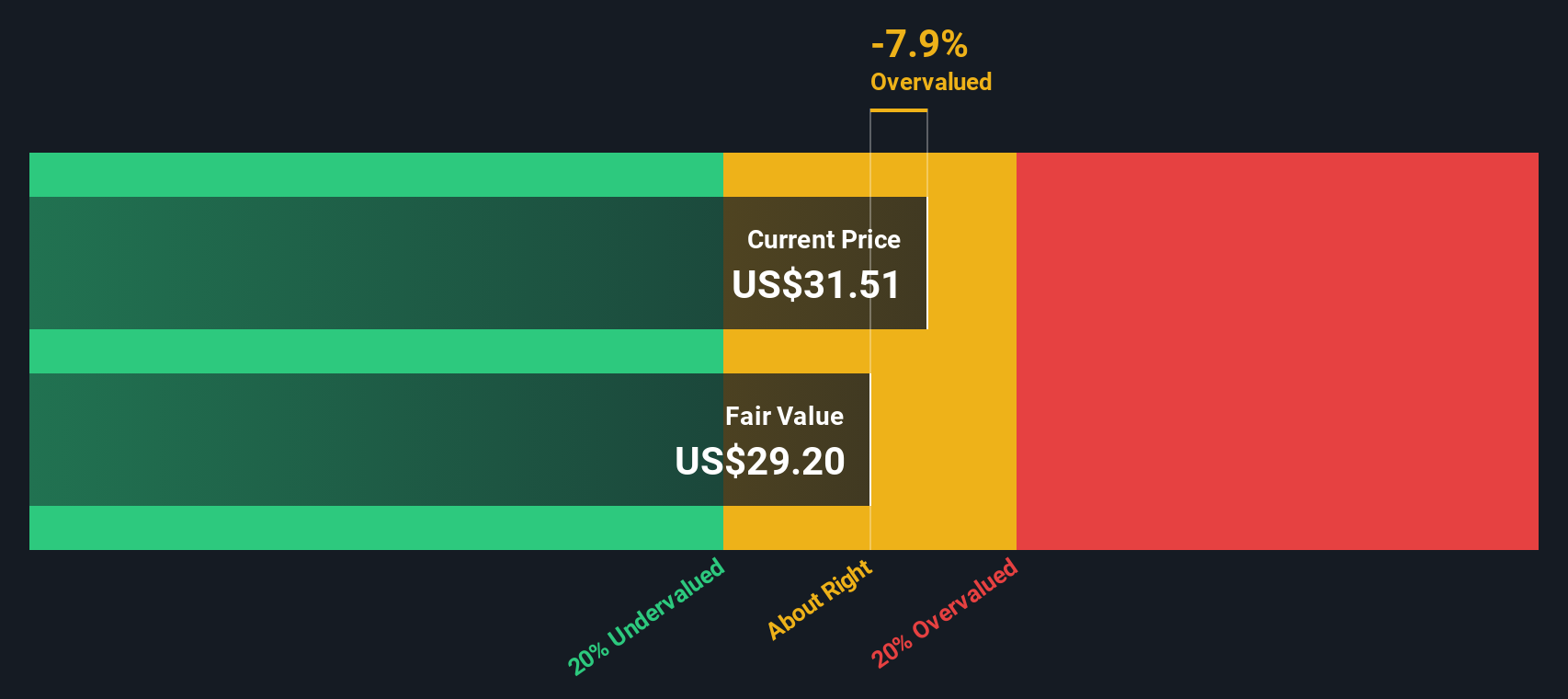

Another View: Discounted Cash Flow Perspective

Looking from another angle, our SWS DCF model suggests ACM Research is trading slightly above its own fair value estimate of $29.43. While the earlier narrative points to a sizable undervaluation, the DCF approach signals the stock may actually be a touch overvalued at current levels. Could this be a sign the market is factoring in too much future optimism?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ACM Research for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ACM Research Narrative

If you have a different perspective or want to form your own view based on the numbers, you can do so yourself in just a few minutes. Do it your way

A great starting point for your ACM Research research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Why limit your strategy? Access a wealth of fresh opportunities by using the Simply Wall Street Screener to spot companies set for major growth and powerful returns.

- Seize the momentum with these 870 undervalued stocks based on cash flows, offering compelling valuations based on real cash flow potential before the crowd catches on.

- Tap into technological advancements and stay ahead of market shifts via these 24 AI penny stocks, featuring companies pioneering AI-driven solutions across industries.

- Maximize your income stream by targeting these 16 dividend stocks with yields > 3%, with reliably high yields to strengthen your portfolio’s long-term stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:ACMR

ACM Research

Develops, manufactures, and sells capital equipment worldwide.

Good value with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor