- United States

- /

- Specialty Stores

- /

- NYSE:GME

Is GameStop’s Recent Slide a Chance or a Warning After Conflicting Valuation Signals?

Reviewed by Bailey Pemberton

How GameStop Has Really Performed for Shareholders

With all the noise around GameStop, it is easy to forget that underneath the memes and message boards sits a real business with a very real share price history. Looking at that record in detail helps separate durable value from short term hype.

Over the last five years, early believers have done very well. GameStop shares are still up more than 350% across that period, even after the dust from the 2021 short squeeze and subsequent volatility has settled.

Zoom in, though, and the picture becomes more complicated. Over the past year the stock has declined around 24%, giving back a chunk of those earlier gains and signaling that the market has tempered expectations about the companys future.

The shorter term moves tell their own story, and they are far from uniformly negative. In the past month the share price has risen roughly 12%, and in just the last week it has added about 6%, suggesting that traders are still quick to re rate the stock when sentiment shifts.

These swings reflect the dual identity GameStop has developed in recent years: part struggling brick and mortar retailer, part speculative trading vehicle. For long term investors, the key question is whether the current price reflects a realistic path for the underlying business rather than the latest surge in enthusiasm.

The market clearly remains divided on that point. Some participants view the recent weakness as an opportunity to buy into a potential turnaround, while others see the volatility as a sign that risk remains elevated and conviction in the business model is low.

To move beyond the headlines and short term price action, we will break down the stock using several valuation lenses, including intrinsic value estimates and relative pricing versus peers. That will also let us come back to GameStops valuation score of 2 out of 6 checks and explore how a more narrative driven view of the company might give an even deeper perspective on what the current share price really implies.

GameStop scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: GameStop Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to todays dollars. For GameStop, the model used here is a 2 stage Free Cash Flow to Equity approach.

GameStop currently generates about $563.2 Million in Free Cash Flow, and the DCF framework assumes this will grow meaningfully over time. Based on analyst input for the early years and extrapolated estimates thereafter, Simply Wall St projects Free Cash Flow rising to about $4.5 Billion by 2035. Each of these future cash flows is discounted back to reflect risk and the time value of money.

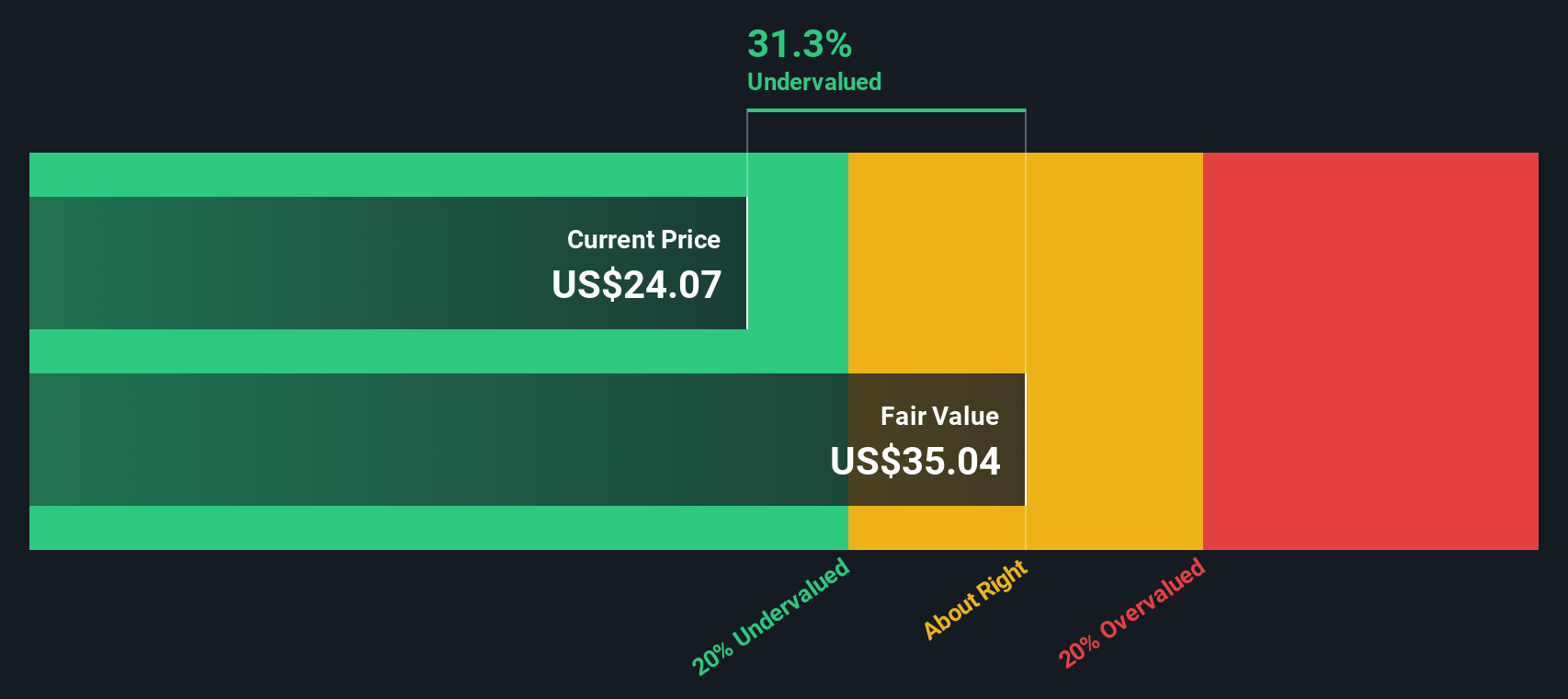

Adding those discounted values together gives an estimated intrinsic value of $101.55 per share. Compared with the current market price, this implies GameStop is trading at a 77.8% discount to its DCF fair value. This suggests the market is pricing in a far weaker future than these cash flow assumptions imply.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests GameStop is undervalued by 77.8%. Track this in your watchlist or portfolio, or discover 914 more undervalued stocks based on cash flows.

Approach 2: GameStop Price vs Earnings

For a business that is generating profits, the price to earnings ratio is a straightforward way to judge how much investors are willing to pay for each dollar of earnings. It ties the share price directly to the bottom line, which makes it a useful cross check against more assumption heavy models such as a DCF.

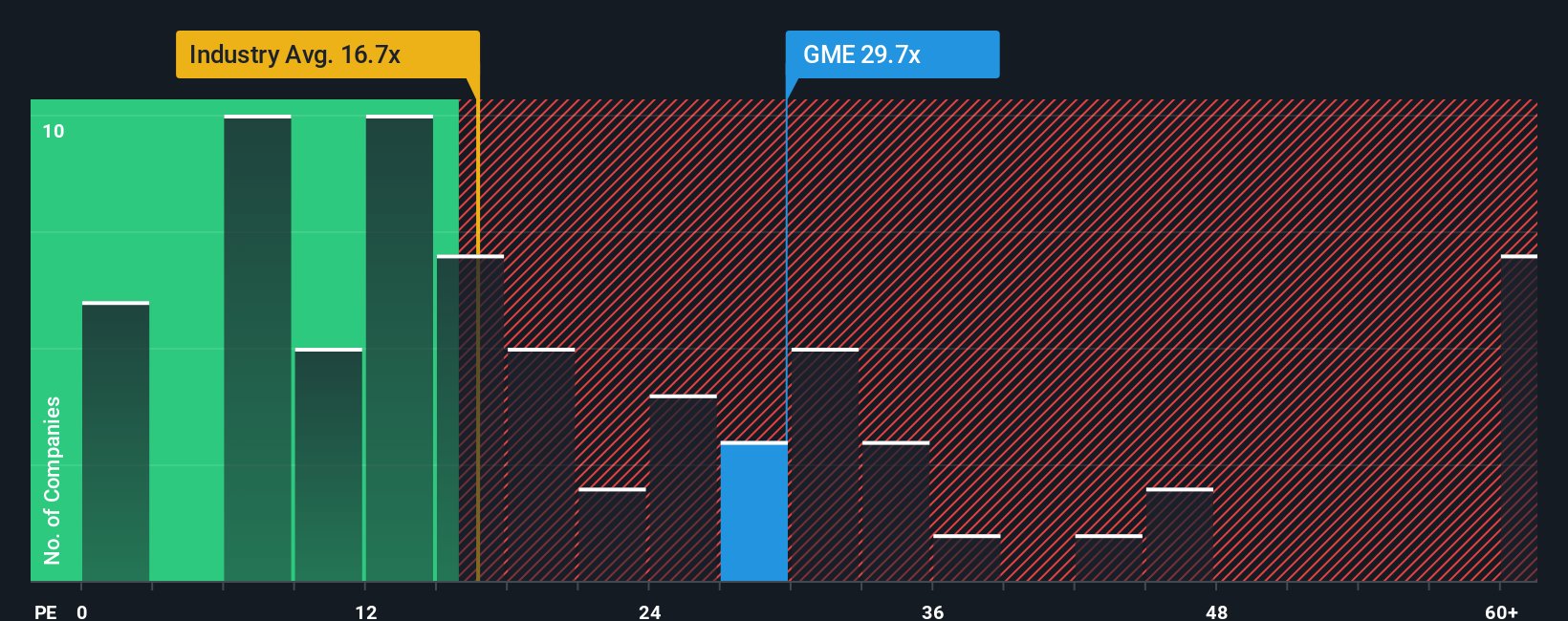

What counts as a normal PE depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth and more resilient profits usually justify a higher multiple. In contrast, slower or more uncertain earnings tend to deserve a discount. GameStop currently trades on a PE of about 23.9x, slightly above the Specialty Retail industry average of around 20.3x and its broader peer group near 20.3x. This signals that the market is already baking in some optimism.

Simply Wall St also calculates a Fair Ratio, a proprietary estimate of what GameStop’s PE should be once you factor in its earnings growth outlook, profit margins, risk profile, industry positioning and market capitalization. This is more tailored than a simple peer comparison because it adjusts for the company’s specific strengths and weaknesses rather than assuming every retailer deserves the same multiple. On that basis, GameStop’s current PE sits meaningfully above its Fair Ratio, indicating the shares are pricing in more good news than the fundamentals alone would suggest.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your GameStop Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you connect your view of a company’s story with a specific financial forecast and Fair Value estimate. A Narrative is your explanation for why the numbers should look a certain way, linking assumptions about future revenue, earnings and margins to a concrete valuation and making it easier to see whether today’s price looks attractive or stretched. Narratives on the platform are easy to explore and compare, and they update dynamically as new information like earnings releases or news arrives, helping you continually reassess when to buy, hold, or sell by comparing each Narrative’s Fair Value to the live share price. For GameStop, one bullish Narrative currently pegs Fair Value around $120 per share while a more cautious one sits closer to $11.91, illustrating how different investors can tell very different but clearly quantified stories about the same stock.

For GameStop, however, we will make it really easy for you with previews of two leading GameStop Narratives:

Fair Value: $120.00

Implied Undervaluation vs Last Close: 81.3%

Revenue Growth Assumption: 0%

- Highlights a sharp swing back to profitability in Q1 2025, with adjusted EPS of $0.17 and a $44.8 million net profit, supported by aggressive cost cutting and store rationalisation.

- Emphasises a fortress balance sheet, with around $6.4 billion in cash, zero long term debt, and a sizeable Bitcoin position that could amplify upside if crypto prices continue to rise.

- Sees GameStop’s loyal retail shareholder base and heavy DRS usage as a structural support for the share price, potentially enabling future short squeezes and underpinning a long term digital transformation story.

Fair Value: $11.91

Implied Overvaluation vs Last Close: 88.9%

Revenue Growth Assumption: 0%

- Argues that while cost cuts and a recent return to profit are positive, GameStop still faces falling revenues, intense digital competition, and an uncertain transition away from its legacy brick and mortar model.

- Views initiatives like BNPL partnerships and potential crypto exposure as interesting but unproven, adding complexity and risk without yet delivering consistent, scalable growth.

- Warns that meme stock dynamics, renewed attention from influential figures, and speculative trading can drive large price swings that are poorly anchored to fundamentals, making the stock risky for long term investors.

Do you think there's more to the story for GameStop? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GME

GameStop

A specialty retailer, provides games and entertainment products through its stores and e-commerce platforms in the United States, Canada, Australia, and Europe.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion