Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BBWI

Is BBWI’s Downward Guidance a Setback for Its Brand Reinvention and Digital Push?

Simply Wall St

Reviewed by Sasha Jovanovic

- Bath & Body Works recently reported third quarter results, showing quarterly sales of US$1.59 billion and net income of US$77 million, both declining from the same period a year prior, while also revising its full-year 2025 guidance to reflect expected low single-digit declines in both sales and earnings per share.

- This update highlights ongoing pressures from weaker consumer sentiment and elevated tariffs, prompting the company to adjust its outlook despite launching early holiday promotions and appointing new creative leadership.

- We'll examine how this downward earnings revision and updated guidance impact Bath & Body Works' long-term digital and brand transformation narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

Bath & Body Works Investment Narrative Recap

To be a shareholder in Bath & Body Works right now, you need to believe that the company can reignite growth through digital innovation and brand revitalization, even as near-term results remain pressured by weak consumer spending and tariff impacts. The latest downward guidance makes it clear that softer sales and higher costs are the primary short-term catalyst and risk, respectively; this revision does meaningfully increase near-term uncertainty over the earnings recovery narrative.

Among recent announcements, the revised full-year 2025 guidance directly connects to the updated risk profile outlined by management, particularly around global tariffs and persistent headwinds affecting both revenue and profitability. This guidance, which now anticipates low single-digit declines in sales and earnings per share, puts additional focus on how effectively management can manage cost pressures and sustain the momentum of its digital and brand initiatives through challenging conditions.

By contrast, what many investors may be missing is the degree to which margin pressure from tariffs could linger into future quarters, especially if...

Read the full narrative on Bath & Body Works (it's free!)

Bath & Body Works' outlook anticipates $8.1 billion in revenue and $860.7 million in earnings by 2028. This forecast implies a 3.1% annual revenue growth rate and an increase in earnings of about $132.7 million from the current $728.0 million.

Uncover how Bath & Body Works' forecasts yield a $36.96 fair value, a 134% upside to its current price.

Exploring Other Perspectives

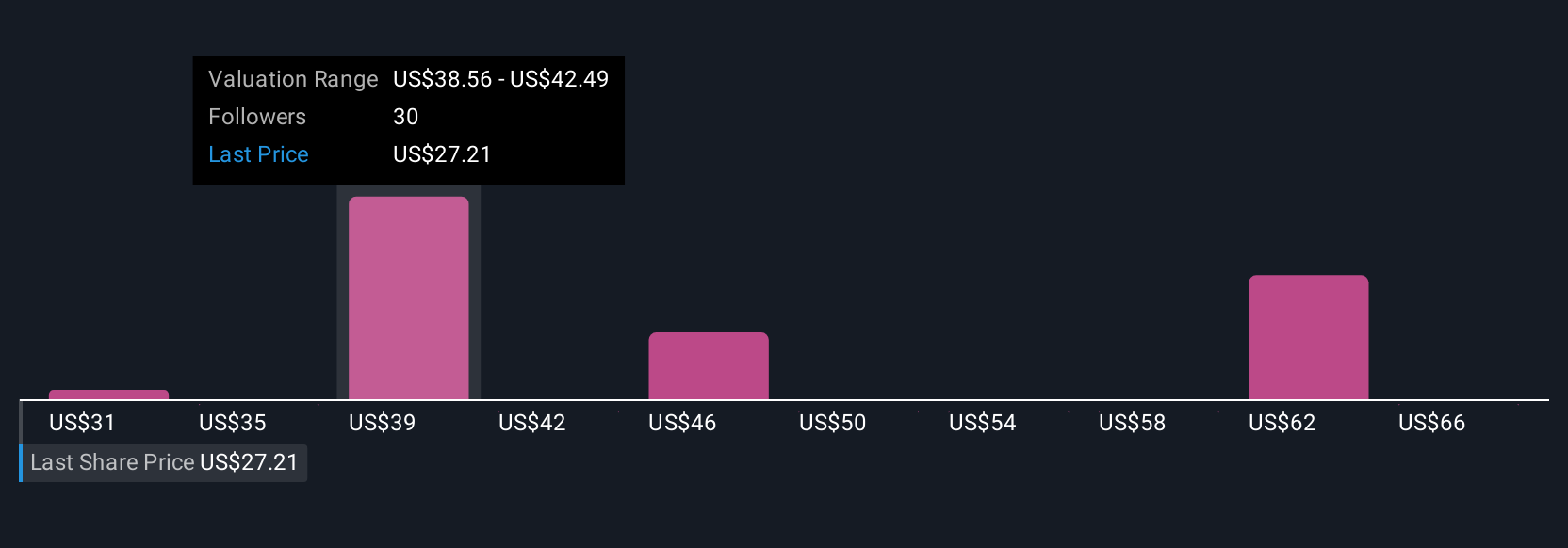

Nine members of the Simply Wall St Community estimate Bath & Body Works’ fair value between US$30.70 and US$64.56, showing wide-ranging outlooks. With revised guidance highlighting ongoing margin risks, consider how your perspective aligns and see what other investors are forecasting.

Explore 9 other fair value estimates on Bath & Body Works - why the stock might be worth over 4x more than the current price!

Build Your Own Bath & Body Works Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bath & Body Works research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Bath & Body Works research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bath & Body Works' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bath & Body Works might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BBWI

Bath & Body Works

Operates as a specialty retailer of home fragrance, personal and body care, soaps, and sanitizer products.

Undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor