Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:ROST

How Investors May Respond To Ross Stores (ROST) Surpassing Earnings Expectations for a Second Quarter

Simply Wall St

Reviewed by Sasha Jovanovic

- Ross Stores recently reported earnings that surpassed analyst expectations for the second consecutive quarter, prompting heightened optimism from market watchers.

- Analysts are now increasingly upbeat about the company's future earnings potential, suggesting momentum is building around its ability to consistently deliver positive surprises.

- With analysts turning more positive on future earnings prospects, we'll examine the implications of this trend on Ross Stores' investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Ross Stores Investment Narrative Recap

To feel confident as a Ross Stores shareholder, you’d need to believe the company can continue capturing shoppers seeking value amid ongoing economic uncertainty while balancing margin pressures from tariff and distribution cost headwinds. The recent string of earnings beats fuels optimism around near-term performance, but these positive surprises are not material enough to fully offset the persistent risk of margin compression from higher costs, still the most important issue in the short term.

Among this fall’s key announcements, Ross’s rapid pace of store openings stands out. Launching new locations across multiple states speaks to management’s efforts to expand market share, an important growth catalyst, but also increases exposure to risks tied to rising operating costs and the ever-present question of market saturation.

On the other hand, while most headlines focus on earnings beats, it remains critical for investors to also keep an eye on rising distribution expenses and the risk these pose to...

Read the full narrative on Ross Stores (it's free!)

Ross Stores is projected to reach $25.0 billion in revenue and $2.4 billion in earnings by 2028. This outlook is based on an expected annual revenue growth rate of 5.1% and reflects an increase of $0.3 billion in earnings from the current $2.1 billion level.

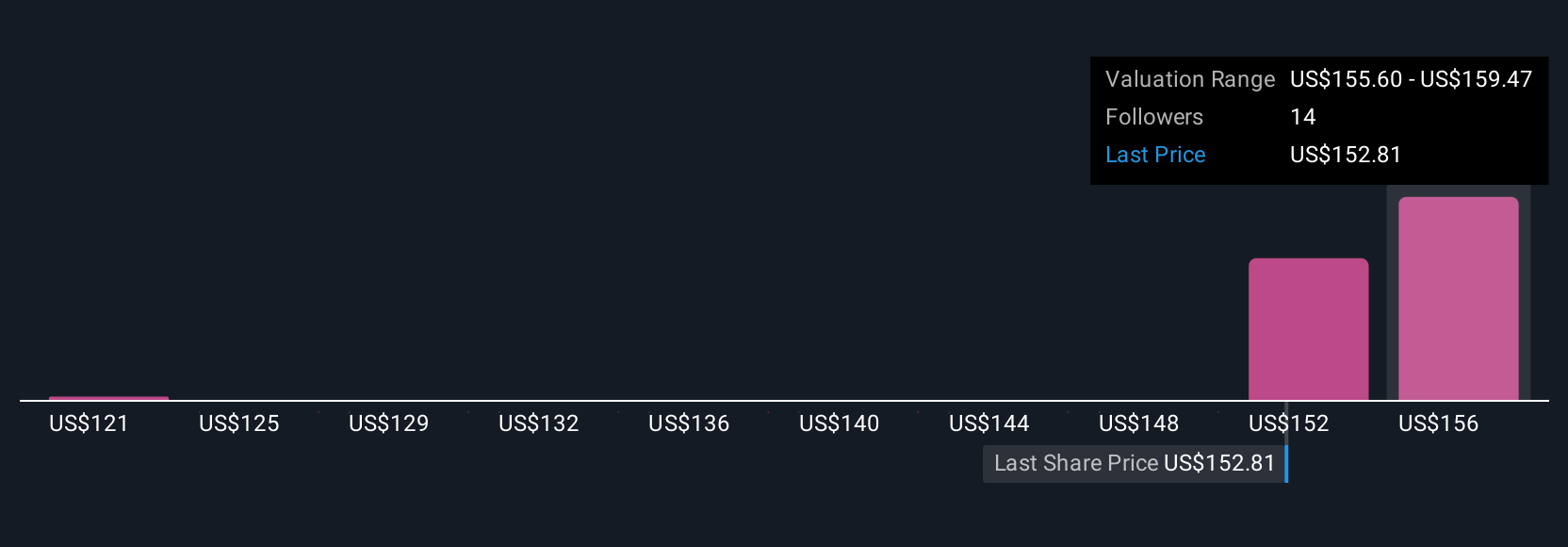

Uncover how Ross Stores' forecasts yield a $164.59 fair value, in line with its current price.

Exploring Other Perspectives

Five private investors from the Simply Wall St Community pegged fair value for Ross Stores between US$10.84 and US$165.42 per share. Their wide-ranging assessments reflect sharply differing expectations, particularly as persistent margin pressure remains a key story shaping the company’s outlook.

Explore 5 other fair value estimates on Ross Stores - why the stock might be worth as much as $165.42!

Build Your Own Ross Stores Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ross Stores research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ross Stores research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ross Stores' overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ROST

Ross Stores

Operates off-price retail apparel and home fashion stores under the Ross Dress for Less and dd’s DISCOUNTS brands in the United States.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor