Advertisement

- United States

- /

- Retail Distributors

- /

- NasdaqGS:POOL

Is This the Right Time to Revisit Pool After a 4.4% Weekly Rally?

Simply Wall St

Reviewed by Bailey Pemberton

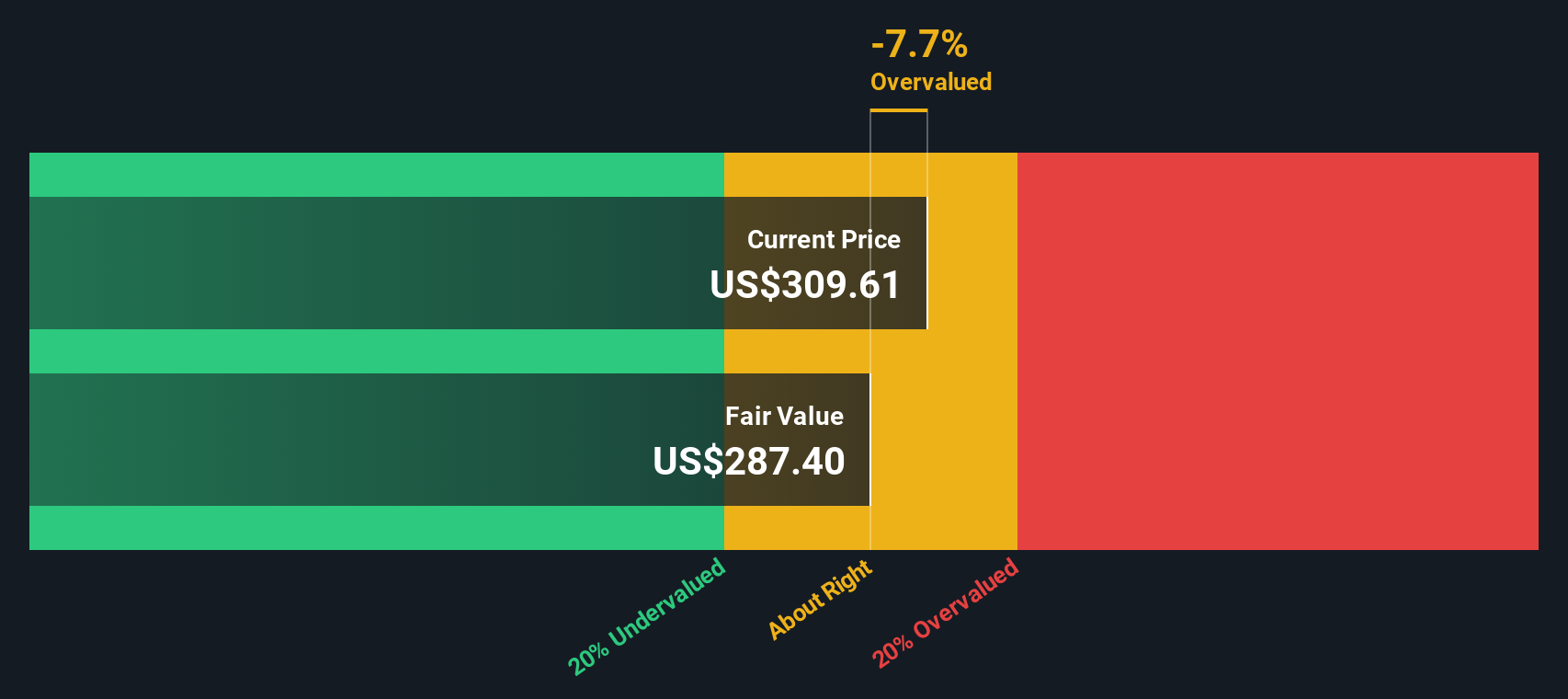

- Ever wondered if Pool stock is a hidden deal or overpriced in today’s market? You’re not alone. Many investors are questioning whether now is the right time to make a move.

- Pool’s share price has recently bounced 4.4% in the past week, but that rally comes after a tougher stretch. Over the past month the stock fell 16.8%, and it is now down 26.6% year-to-date.

- Some of this volatility comes as the industry is abuzz over increased residential construction and shifting consumer demand in the leisure and home improvement sectors. This has shined a new spotlight on Pool. Investors are paying close attention as the company navigates fluctuating supply costs and ongoing changes in home project trends.

- With a current valuation score of 3 out of 6, Pool’s price has some investors feeling cautious, while others see opportunity. We’ll break down the usual valuation checks next, but stick around because we’ll close with a perspective many investors overlook when evaluating companies like Pool.

Find out why Pool's -34.1% return over the last year is lagging behind its peers.

Approach 1: Pool Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) approach estimates a company's intrinsic value by projecting its expected future cash flows and discounting them back to their value today. This method helps investors gauge whether a stock’s current price reflects its actual earning power over time.

For Pool, analysts estimate current Free Cash Flow at $396.6 million. Over the next five years, future cash flows are projected to rise steadily, with the forecast for 2028 reaching $482 million. Projections beyond these years, based on a blend of analyst consensus and long-term trend assumptions, show Free Cash Flow reaching approximately $626.6 million by 2035. All of these figures are in US dollars.

When all projected cash flows are discounted to their present value, the result is an estimated intrinsic value per share of $303.38. Compared to Pool’s current trading price, the DCF analysis indicates the stock is 19.5% undervalued. In other words, the market may not be fully recognizing the company’s ability to grow and generate cash in the years ahead.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pool is undervalued by 19.5%. Track this in your watchlist or portfolio, or discover 928 more undervalued stocks based on cash flows.

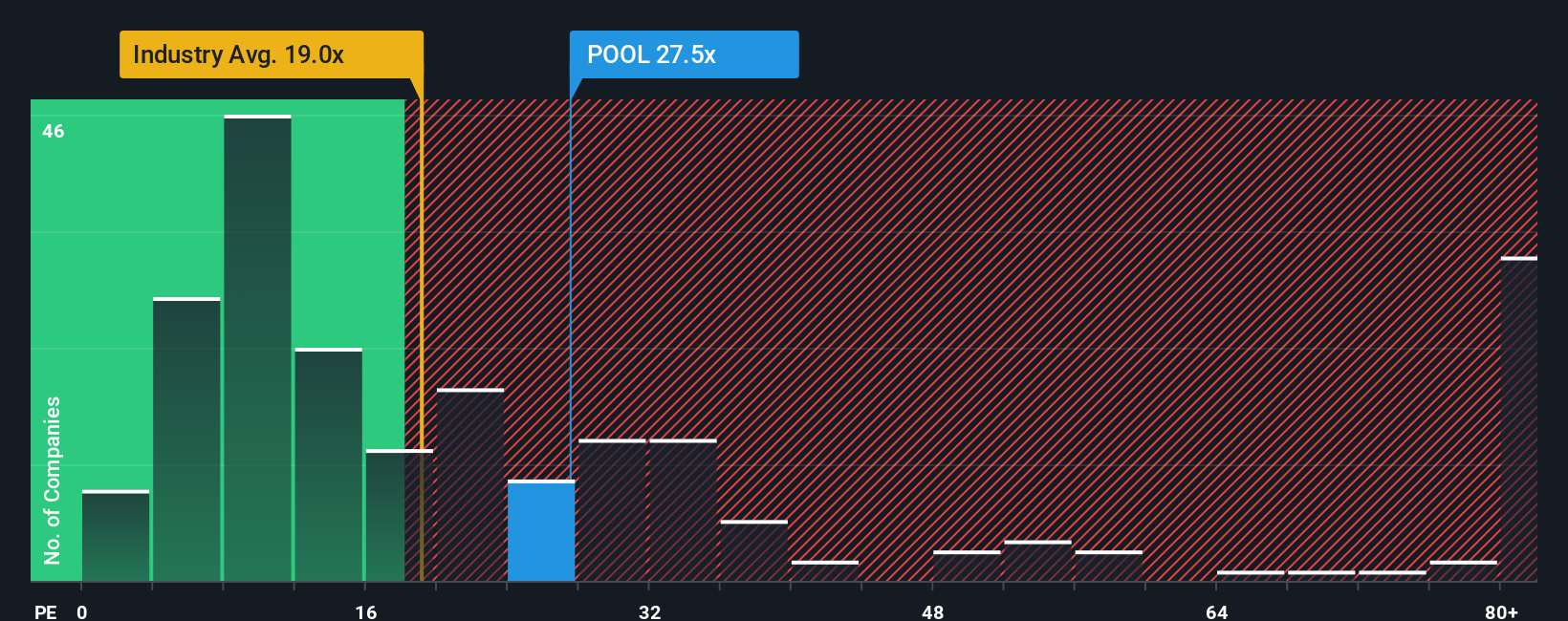

Approach 2: Pool Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used metric for valuing profitable companies like Pool. It measures how much investors are willing to pay today for a dollar of the company’s earnings, making it a straightforward tool for comparing valuations across different businesses.

Generally, higher growth expectations and lower perceived risks justify a higher PE ratio, while companies with slower growth or higher uncertainty typically trade at lower multiples. Comparing Pool’s current PE ratio of 22.2x to the retail distributors industry average of 18.0x and the peer group average of 33.7x, Pool’s valuation stands in the middle. This suggests the market is pricing in moderate growth prospects and some stability versus its peers.

To provide added context, Simply Wall St’s proprietary "Fair Ratio" assesses what an appropriate PE multiple should be for Pool based on its earnings growth, industry positioning, risk profile, profit margins, and market cap. This tailored approach offers a more precise benchmark than just comparing Company A with peers or broad industry figures because it specifically considers Pool’s unique circumstances and forward outlook.

Pool’s Fair Ratio comes in at 15.5x, notably lower than its current PE of 22.2x. This indicates that the stock is trading above what would be considered fair value for the characteristics it currently presents.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pool Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are a simple and powerful method for investors to go beyond the numbers by telling the story they believe about a company, including their reasons and assumptions about future revenue, profit margins, and fair value. They connect your view of Pool—whether it will succeed or face challenges—to a financial forecast and, ultimately, a fair value estimate. This helps you see if today’s price aligns with your expectations for tomorrow.

Accessible and straightforward, Narratives are available directly in Simply Wall St's Community page, used by millions of investors to share and stress-test their perspectives. This tool empowers you to make more informed decisions by directly comparing each Narrative’s calculated Fair Value with the current market price. Whenever new news or earnings data emerges, Narratives automatically update, ensuring your view always reflects the latest information. For example, some investors believe Pool’s recurring maintenance revenues and Sun Belt expansion justify a price as high as $375.0, while others, more cautious about housing headwinds, set their fair value closer to $285.0. This highlights how Narratives allow you to personalize your investment approach.

Do you think there's more to the story for Pool? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:POOL

Pool

Distributes swimming pool supplies, equipment, related leisure, irrigation, and landscape maintenance products in the United States and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

80 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative