Advertisement

- United States

- /

- Retail Distributors

- /

- NasdaqGM:EDUC

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For Educational Development Corporation's (NASDAQ:EDUC) CEO For Now

Performance at Educational Development Corporation (NASDAQ:EDUC) has been reasonably good and CEO Randall White has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 07 July 2021. However, some shareholders will still be cautious of paying the CEO excessively.

View our latest analysis for Educational Development

Comparing Educational Development Corporation's CEO Compensation With the industry

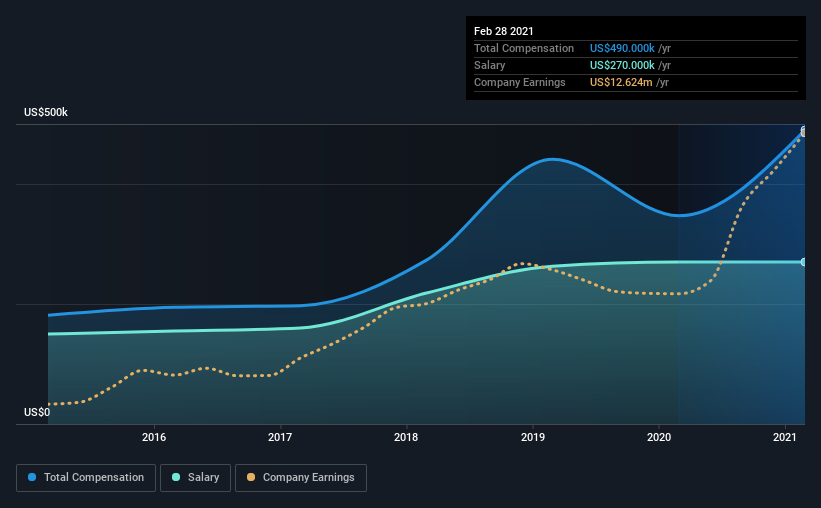

Our data indicates that Educational Development Corporation has a market capitalization of US$104m, and total annual CEO compensation was reported as US$490k for the year to February 2021. We note that's an increase of 41% above last year. In particular, the salary of US$270.0k, makes up a fairly large portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under US$200m, the reported median total CEO compensation was US$28k. Accordingly, our analysis reveals that Educational Development Corporation pays Randall White north of the industry median. Furthermore, Randall White directly owns US$17m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | US$270k | US$270k | 55% |

| Other | US$220k | US$77k | 45% |

| Total Compensation | US$490k | US$347k | 100% |

Talking in terms of the industry, salary represented approximately 52% of total compensation out of all the companies we analyzed, while other remuneration made up 48% of the pie. Our data reveals that Educational Development allocates salary more or less in line with the wider market. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Educational Development Corporation's Growth Numbers

Over the past three years, Educational Development Corporation has seen its earnings per share (EPS) grow by 33% per year. It achieved revenue growth of 81% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Educational Development Corporation Been A Good Investment?

We think that the total shareholder return of 42%, over three years, would leave most Educational Development Corporation shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 3 warning signs for Educational Development that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you’re looking to trade Educational Development, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Educational Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:EDUC

Educational Development

Distributes children's books, educational toys and games, and related products in the United States.

Good value with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor