Advertisement

- United States

- /

- REITS

- /

- NYSE:WPC

How Investors Are Reacting To W. P. Carey (WPC) Raising 2025 Earnings Guidance on Stronger Tenant Outlook

Simply Wall St

Reviewed by Sasha Jovanovic

- In late October 2025, W. P. Carey raised and narrowed its full-year 2025 earnings guidance, now expecting AFFO between US$4.93 and US$4.99 per diluted share, citing higher anticipated investment volume and improved tenant credit outlook.

- This revised guidance signals that better-than-expected tenant credit performance is now expected to substantially reduce potential rent losses for the upcoming year.

- We’ll examine how W. P. Carey’s updated expectations for investment activity and tenant reliability impact its investment narrative and future prospects.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

W. P. Carey Investment Narrative Recap

To be a shareholder in W. P. Carey, you need to believe in the resilience of the net lease model, long-term demand for industrial assets, and the company's ability to manage tenant credit risk. The recent upward revision in 2025 AFFO guidance reduces immediate concerns about rent losses from tenant defaults, positively affecting the company's most important near-term catalyst, stronger rental collections and investment activity. However, this does little to resolve ongoing risks related to reliance on property sales for funding growth.

The recent quarterly dividend increase to US$0.910 per share stands out, reflecting management’s confidence in near-term earnings stability, as reaffirmed by the higher 2025 AFFO outlook. This is encouraging for investors who prioritize reliable income streams, especially as continued investment activity and tenant reliability underpin dividend sustainability.

But even with improving tenant credit quality, investors should not overlook the business's exposure to single-tenant, sub-investment-grade leases and the sudden impact that any unexpected default could have…

Read the full narrative on W. P. Carey (it's free!)

W. P. Carey's outlook anticipates $2.1 billion in revenue and $698.0 million in earnings by 2028. Achieving this would require annual revenue growth of 8.1% and a $362.2 million increase in earnings from the current level of $335.8 million.

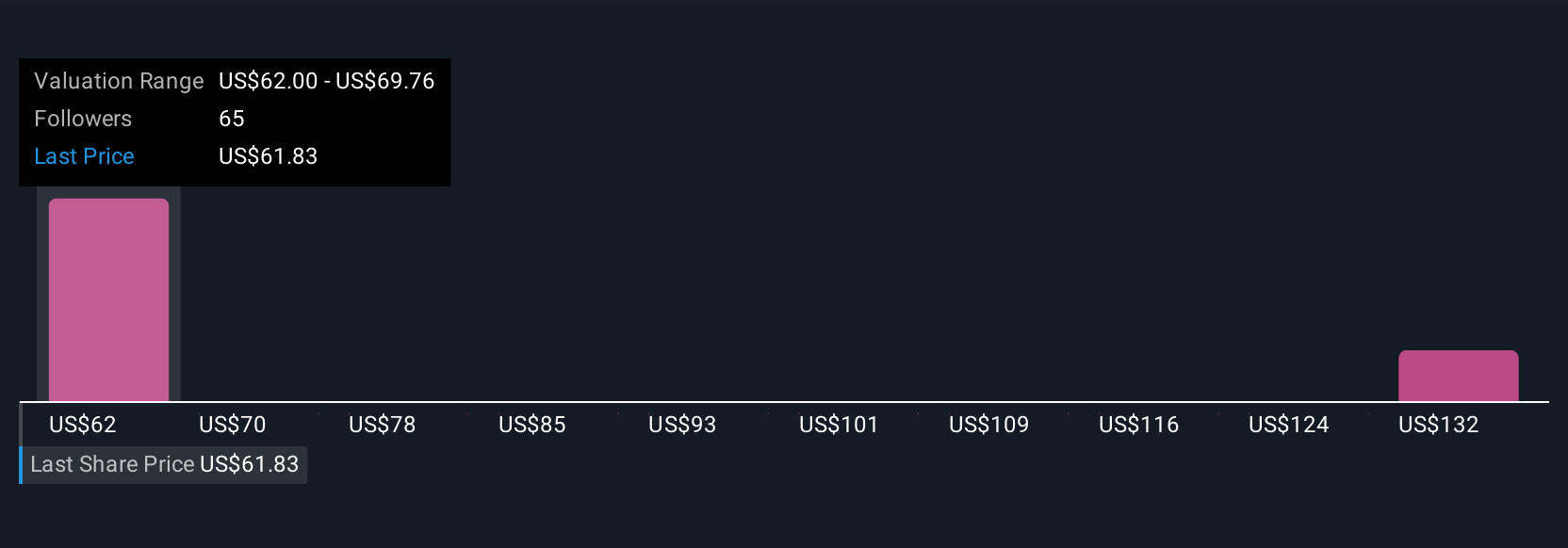

Uncover how W. P. Carey's forecasts yield a $69.18 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community offered fair value estimates for W. P. Carey ranging from US$60.37 to US$158.08 per share. Views differ widely, and while recent guidance points to stronger short-term fundamentals, the potential for tenant defaults remains a central consideration for future income security.

Explore 4 other fair value estimates on W. P. Carey - why the stock might be worth 10% less than the current price!

Build Your Own W. P. Carey Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your W. P. Carey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free W. P. Carey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. P. Carey's overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W. P. Carey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WPC

W. P. Carey

W. P. Carey ranks among the largest net lease REITs with a well-diversified portfolio of high-quality, operationally critical commercial real estate, which includes 1,600 net lease properties covering approximately 178 million square feet and a portfolio of 66 self-storage operating properties as of June 30, 2025.

Average dividend payer with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor