Advertisement

- United States

- /

- Specialized REITs

- /

- NYSE:FCPT

How Investors May Respond To Four Corners Property Trust (FCPT) Strong Q3 Results and New Capital Initiatives

Simply Wall St

Reviewed by Sasha Jovanovic

- In the past week, Four Corners Property Trust announced robust third quarter 2025 results with US$74.15 million in revenue and US$28.85 million in net income, accompanied by a US$500 million equity distribution agreement and new shelf registration to enhance financial flexibility for expansion and debt repayment.

- The company also acquired US$82 million in net lease properties while maintaining high occupancy, reinforcing its position as a leading owner of restaurant and service retail real estate with a diversified tenant base.

- We’ll explore how these strong operating results and new capital initiatives may impact Four Corners Property Trust’s investment outlook.

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Four Corners Property Trust Investment Narrative Recap

To be a shareholder in Four Corners Property Trust, you need to believe in the ongoing resilience of physical service retail tenants and the company’s disciplined approach to growing and diversifying its property portfolio. The most important catalyst remains FCPT's ability to continue acquiring accretive, e-commerce resistant assets, while the biggest risk is its continued high exposure to casual dining. The recent financial updates and new capital initiatives bolster growth capacity, but do not materially shift either the main short-term driver or risk for the business.

Among the recent announcements, the US$500 million equity distribution agreement stands out as most relevant to the company's capacity for near-term expansion and debt repayment. With new flexibility provided by this agreement alongside a fresh shelf registration, FCPT is positioned to fund property acquisitions and manage its capital structure, supporting its ongoing acquisition strategy and portfolio diversification, both key to the company’s investment thesis and ability to address sector concentration risk.

Yet, despite robust results and new funding sources, investors should be aware that the largest risk remains concentrated exposure to dine-in restaurant tenants, especially if consumer trends shift...

Read the full narrative on Four Corners Property Trust (it's free!)

Four Corners Property Trust is projected to generate $344.5 million in revenue and $144.2 million in earnings by 2028. This outlook assumes a 7.2% annual revenue growth rate and an increase in earnings of approximately $38.4 million from the current $105.8 million.

Uncover how Four Corners Property Trust's forecasts yield a $28.88 fair value, a 20% upside to its current price.

Exploring Other Perspectives

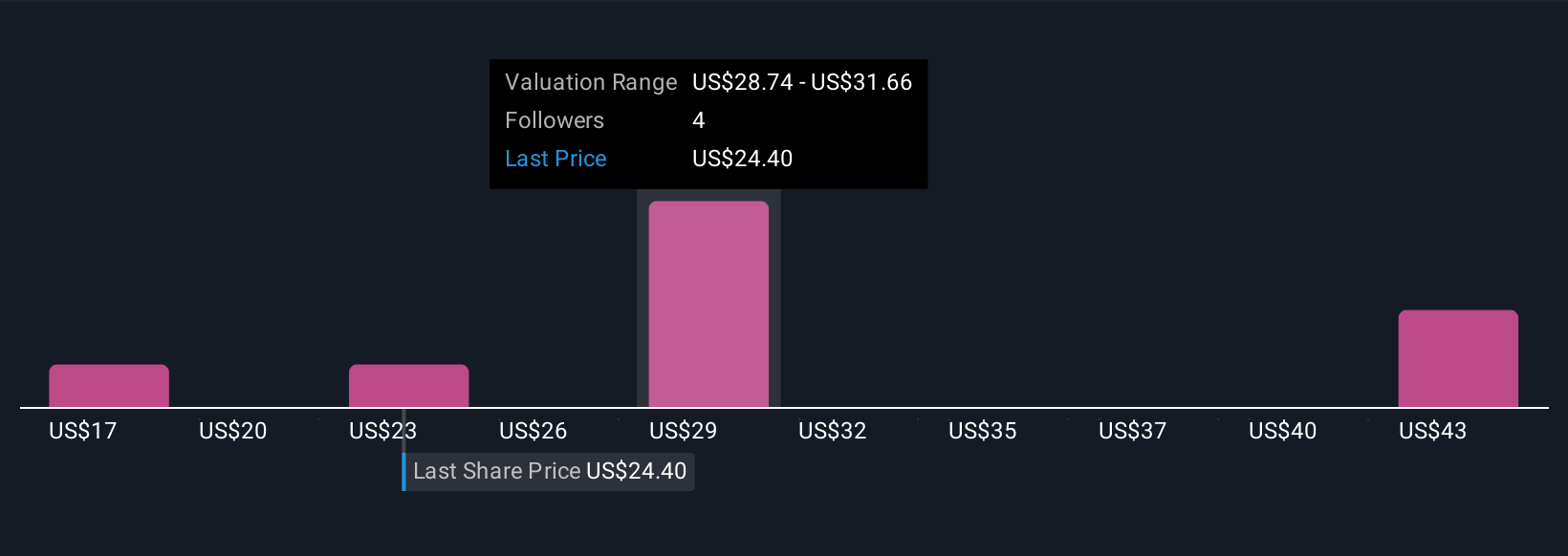

Simply Wall St Community members submitted 4 fair value estimates for FCPT ranging from US$17.09 to US$44.32 per share. While some see substantial upside, others caution that sector concentration and modest rent escalators could shape FCPT's future returns, consider these differing perspectives as you weigh portfolio decisions.

Explore 4 other fair value estimates on Four Corners Property Trust - why the stock might be worth 29% less than the current price!

Build Your Own Four Corners Property Trust Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Four Corners Property Trust research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Four Corners Property Trust research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Four Corners Property Trust's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 38 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FCPT

Four Corners Property Trust

FCPT is a real estate investment trust primarily engaged in the ownership, acquisition and leasing of restaurant and retail properties.

6 star dividend payer with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor