Advertisement

- United States

- /

- Industrial REITs

- /

- NYSE:EGP

How New Credit Terms and Earnings Surpass at EastGroup Properties (EGP) Have Changed Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- EastGroup Properties recently announced it secured a US$250 million unsecured term loan with PNC Bank and partners, alongside an amended US$625 million revolving credit facility that eliminates an upward interest rate adjustment on SOFR loans.

- This financial update comes on the heels of third-quarter 2025 earnings that surpassed analyst expectations, highlighting the company's support from lenders and operational momentum.

- We'll examine how the amended credit facility, which reduces borrowing costs, could impact the investment outlook for EastGroup Properties.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

EastGroup Properties Investment Narrative Recap

To believe in EastGroup Properties as a shareholder, you need conviction in the ongoing demand for modern industrial and logistics space across high-growth Sunbelt markets, supported by e-commerce trends and migration. The recent US$250 million unsecured loan and amended US$625 million credit facility modestly lower borrowing costs, but do not materially change the biggest short-term catalyst, tenant leasing strength, or the primary risk around prolonged uncertainty or decision delays by larger tenants, especially against a backdrop of macroeconomic headwinds.

Among recent announcements, the Q3 2025 earnings report stands out: EastGroup delivered revenue and net income growth, surpassing analyst expectations. This operational outperformance provides a clearer view of how access to improved financing could support new acquisitions or developments if tenant demand remains resilient and leasing timelines shorten as macro challenges abate.

Yet in contrast, investors should be aware that tenant health in key markets like California still presents a risk, especially as...

Read the full narrative on EastGroup Properties (it's free!)

EastGroup Properties' narrative projects $921.3 million revenue and $339.7 million earnings by 2028. This requires 10.8% yearly revenue growth and a $103.2 million earnings increase from $236.5 million today.

Uncover how EastGroup Properties' forecasts yield a $193.84 fair value, a 7% upside to its current price.

Exploring Other Perspectives

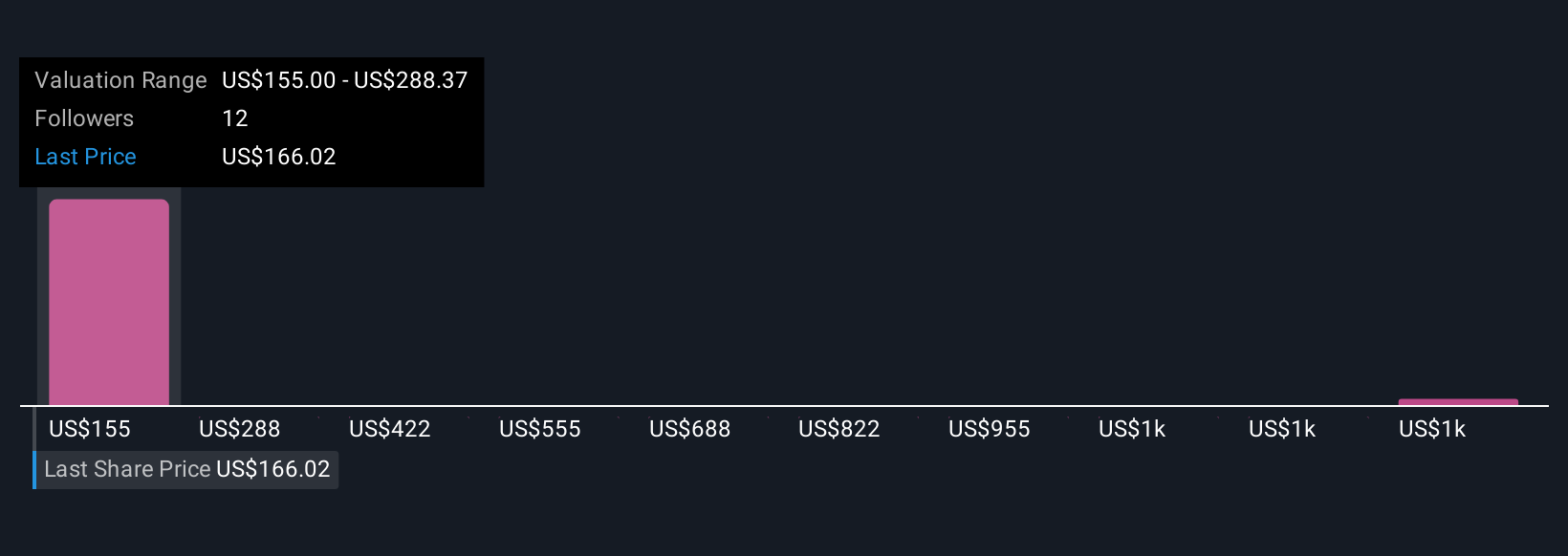

Five fair value estimates from the Simply Wall St Community range from US$155 up to US$1,488, spanning all the way from below to well above analyst and market consensus. Robust population growth and supply constraints are frequently cited as tailwinds, but make sure you review a range of individual perspectives before deciding your view on EastGroup Properties.

Explore 5 other fair value estimates on EastGroup Properties - why the stock might be worth 14% less than the current price!

Build Your Own EastGroup Properties Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your EastGroup Properties research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EastGroup Properties research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EastGroup Properties' overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EastGroup Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EGP

EastGroup Properties

EastGroup Properties, Inc. (NYSE: EGP), a member of the S&P Mid-Cap 400 and Russell 2000 Indexes, is a self-administered equity real estate investment trust focused on the development, acquisition and operation of industrial properties in high-growth markets throughout the United States with an emphasis in the states of Texas, Florida, California, Arizona and North Carolina.

Established dividend payer with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

83 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

919 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative