- United States

- /

- Retail REITs

- /

- NYSE:ALX

Alexander’s (ALX): Valuation Check After $175 Million Rego Park II Refinancing Extends Debt to 2030

Reviewed by Simply Wall St

Alexander's (ALX) just locked in a fresh $175 million refinancing on its Rego Park II shopping center in Queens, extending the loan out to December 2030 and easing near term refinancing pressure.

See our latest analysis for Alexander's.

That refinancing headline lands against a backdrop where the share price has climbed to $219.31, with an 11.77% year to date share price return and a solid 18.44% one year total shareholder return, suggesting momentum is cautiously rebuilding after recent 90 day weakness.

If this refinancing has you thinking about positioning for the next leg in real estate and income names, it could also be worth scanning pharma stocks with solid dividends for other yield focused opportunities.

Yet with earnings growth under pressure and shares now trading above the average analyst target, investors face a key question: does Alexander's still offer hidden value here, or is the market already pricing in its future growth?

Price-to-Earnings of 30.5x: Is it justified?

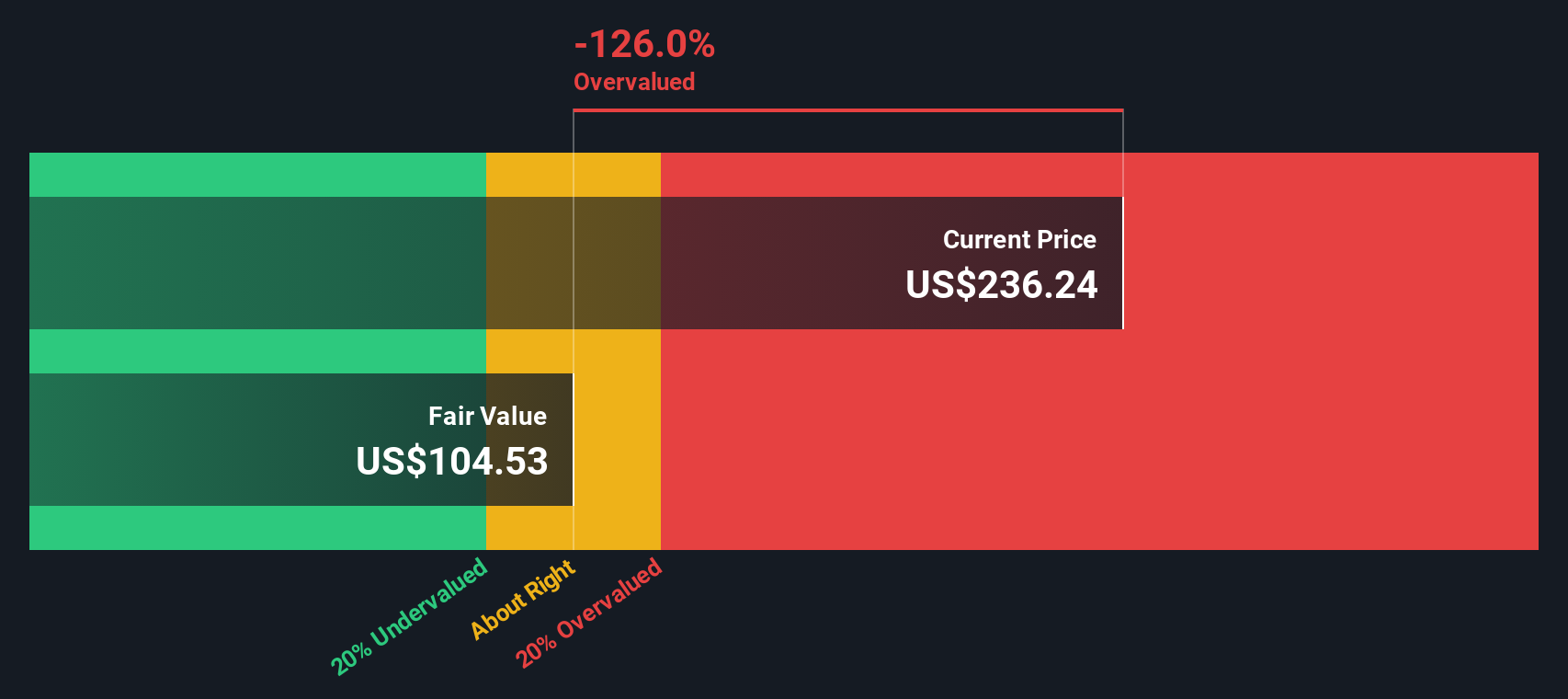

Alexander's last closed at $219.31, and its current price-to-earnings ratio of 30.5x screens as expensive against both peers and its own fundamentals.

The price-to-earnings ratio compares the current share price with the company’s earnings per share. It effectively shows how much investors are paying for each dollar of profit. For a mature, income focused Retail REIT with declining earnings and modest revenue growth, such a rich multiple suggests investors are pricing in more stability and growth than the business has recently delivered.

Compared with the broader US Retail REITs industry average P/E of 27.1x and a peer average of just 19.1x, Alexander's valuation stands at a clear premium. It also sits above the estimated fair P/E ratio of 26.8x. This is a level the market could gravitate toward if sentiment or fundamentals cool from here.

Explore the SWS fair ratio for Alexander's

Result: Price-to-Earnings of 30.5x (OVERVALUED)

However, persistent net income declines and shares trading 18 percent above the consensus target could swiftly unwind sentiment if fundamentals or financing conditions deteriorate.

Find out about the key risks to this Alexander's narrative.

Another View: Our DCF Signals Deeper Downside

While the current price-to-earnings ratio paints Alexander's as expensive, our DCF model goes further and suggests the shares are significantly overvalued versus an estimated fair value of roughly $147. With such a wide gap, could future returns struggle to justify today’s optimism?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Alexander's for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 906 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Alexander's Narrative

If you see things differently or would rather dig into the numbers yourself, you can build a personalized take in just minutes: Do it your way.

A great starting point for your Alexander's research is our analysis highlighting 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

Before you move on, put the Simply Wall Street Screener to work and uncover fresh opportunities that could reshape your portfolio’s returns this year.

- Capture potential mispricings by targeting companies trading below their cash flow value using these 906 undervalued stocks based on cash flows for a sharper margin of safety.

- Capitalize on breakthrough innovation by hunting for future winners among these 26 AI penny stocks before the crowd fully catches on.

- Strengthen your income stream by zeroing in on these 13 dividend stocks with yields > 3% that can complement or even outperform traditional yield plays.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ALX

Alexander's

Alexander’s, Inc. is a real estate investment trust (REIT) engaged in leasing, managing, developing and redeveloping properties.

Average dividend payer with low risk.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion