Advertisement

- United States

- /

- Real Estate

- /

- NasdaqGS:NMRK

Will Newmark Group's (NMRK) European Hires Redefine Its Global Capital Markets Ambitions?

Simply Wall St

Reviewed by Sasha Jovanovic

- Newmark Group recently appointed Andrew Wheldon and Matthew Bailey, two highly experienced finance professionals, to its European Finance team to strengthen its capital markets advisory capabilities across multiple asset classes in Europe.

- This move not only enhances Newmark’s regional expertise but also reflects the company’s push to scale its global Debt, Equity and Structured Finance business amid continued investment in international capital markets growth.

- We’ll explore how the addition of veteran European finance specialists may further support Newmark’s expansion strategy and evolving investment outlook.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Newmark Group Investment Narrative Recap

Shareholders in Newmark Group, Inc. typically believe in the company's ability to scale globally, particularly in capital markets and alternative asset classes, through continued investment in talent and expansion across Europe and Asia. The recent hiring of Andrew Wheldon and Matthew Bailey aligns with management’s growth strategy, but this development is not likely to materially change the most immediate catalyst: sustained growth in capital markets revenue, nor does it mitigate the biggest risk, higher operational and integration costs from rapid international buildout.

Among recent announcements, Newmark’s raised earnings guidance stands out, estimating 2025 revenues between US$3.18 billion and US$3.33 billion. This ties directly to new hires like Wheldon and Bailey, as their track record in European structured finance supports efforts to capitalize on market share opportunities, though integration of these hires remains crucial to capturing the benefits implied in the guidance.

However, despite the global ambitions, investors need to be aware that rapid expansion outside the US brings increased execution and integration risk, especially if...

Read the full narrative on Newmark Group (it's free!)

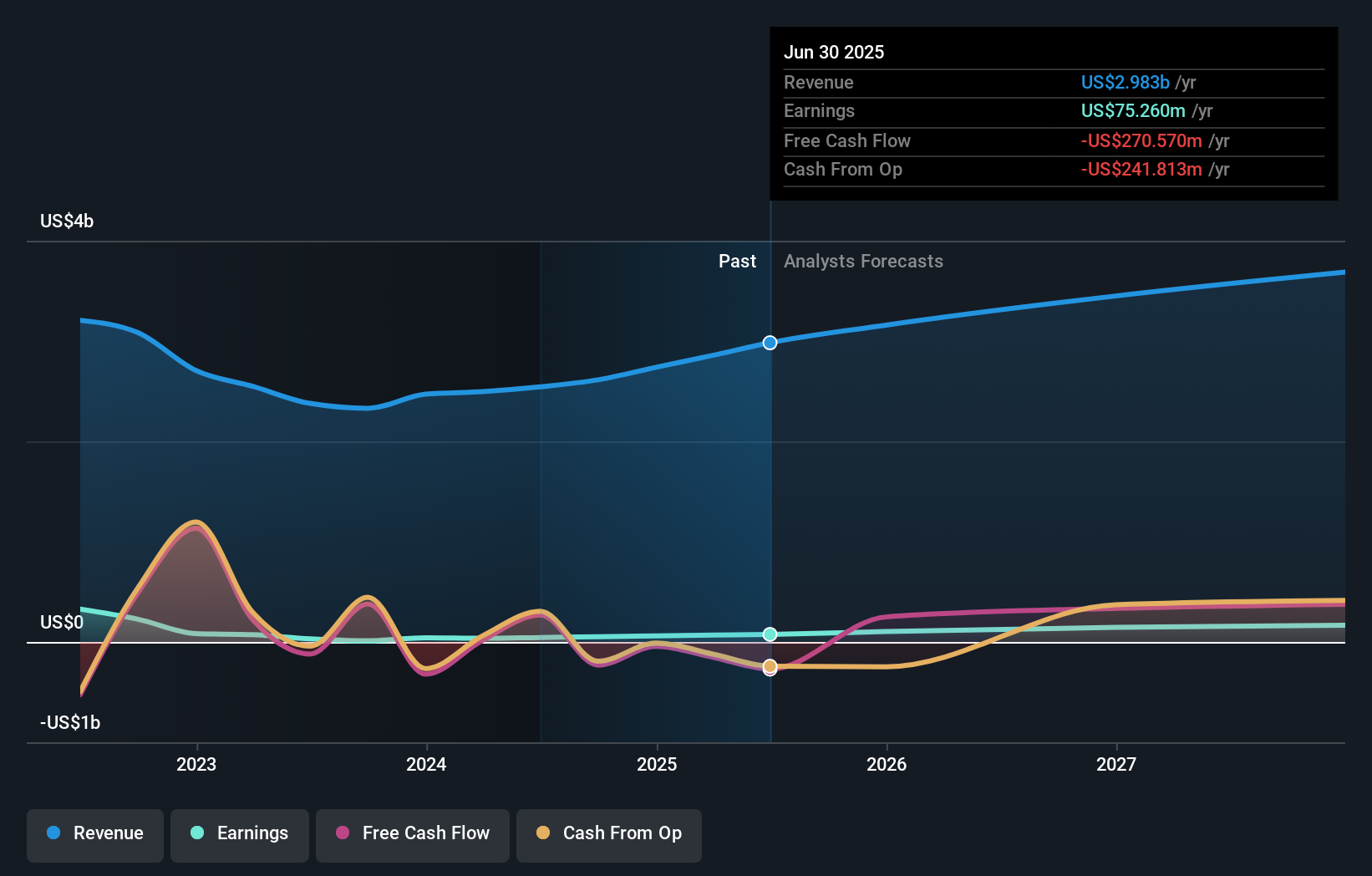

Newmark Group's forecast sees revenues reaching $3.8 billion and earnings at $201.7 million by 2028. This outlook assumes an annual revenue growth rate of 8.2% and an earnings increase of about $126 million from the current level of $75.3 million.

Uncover how Newmark Group's forecasts yield a $19.80 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Fair value opinions from the Simply Wall St Community range from US$11.81 to US$23.26, based on three separate analyses. With elevated integration risk tied to new international leadership, it’s clear that many views on Newmark’s performance potential remain sharply divided, explore several points of view before making any decisions.

Explore 3 other fair value estimates on Newmark Group - why the stock might be worth as much as 42% more than the current price!

Build Your Own Newmark Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Newmark Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Newmark Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Newmark Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Newmark Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NMRK

Newmark Group

Provides commercial real estate services in the United States, the United Kingdom, and internationally.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor