Advertisement

- United States

- /

- Real Estate

- /

- NasdaqGS:NMRK

Does Newmark Group’s 39% Rally in 2025 Signal More Room to Run?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if Newmark Group is still a bargain, or if you’ve missed your moment? Let’s break down whether the current price really tells the full story.

- The stock has had quite a year, returning 38.6% year-to-date and rising 5.5% in the past week. It has cooled off a little in the past month.

- Recent headlines around increased commercial real estate activity and high-profile property deals have helped drive investor interest, setting the stage for some of those positive moves. With momentum in the sector building, there’s been extra attention on Newmark’s role in some of the latest transactions and partnerships.

- The company scores a 3 out of 6 on our undervalued checks. However, there’s more to value than just checklists. We’ll start with some classic valuation approaches, but stick around until the end for a perspective that may offer a deeper look at what really drives a fair price.

Approach 1: Newmark Group Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) analysis estimates a company's current value by projecting its future free cash flows and discounting them back to today's dollars. This helps investors determine whether a stock is fairly priced compared to its anticipated cash generation.

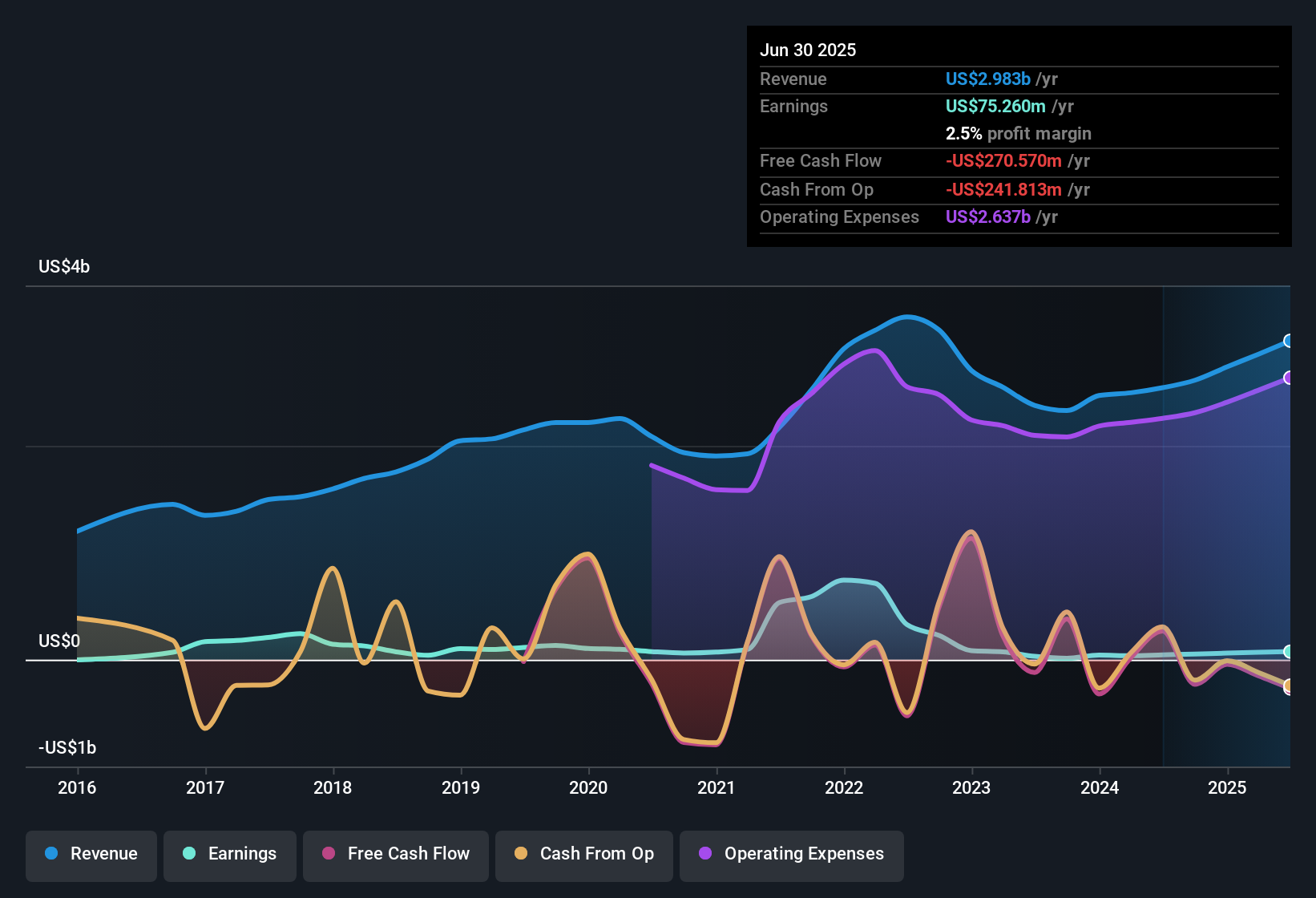

Newmark Group's most recent twelve months of free cash flow were negative, at -$95.16 Million. However, forecasts suggest a turnaround and robust growth. Analyst projections indicate Newmark's free cash flow could reach $444 Million by the end of 2029. After analyst consensus covers the first five years, further annual estimates are extrapolated. These projections show a strong uptrend, with free cash flows rising steadily year after year.

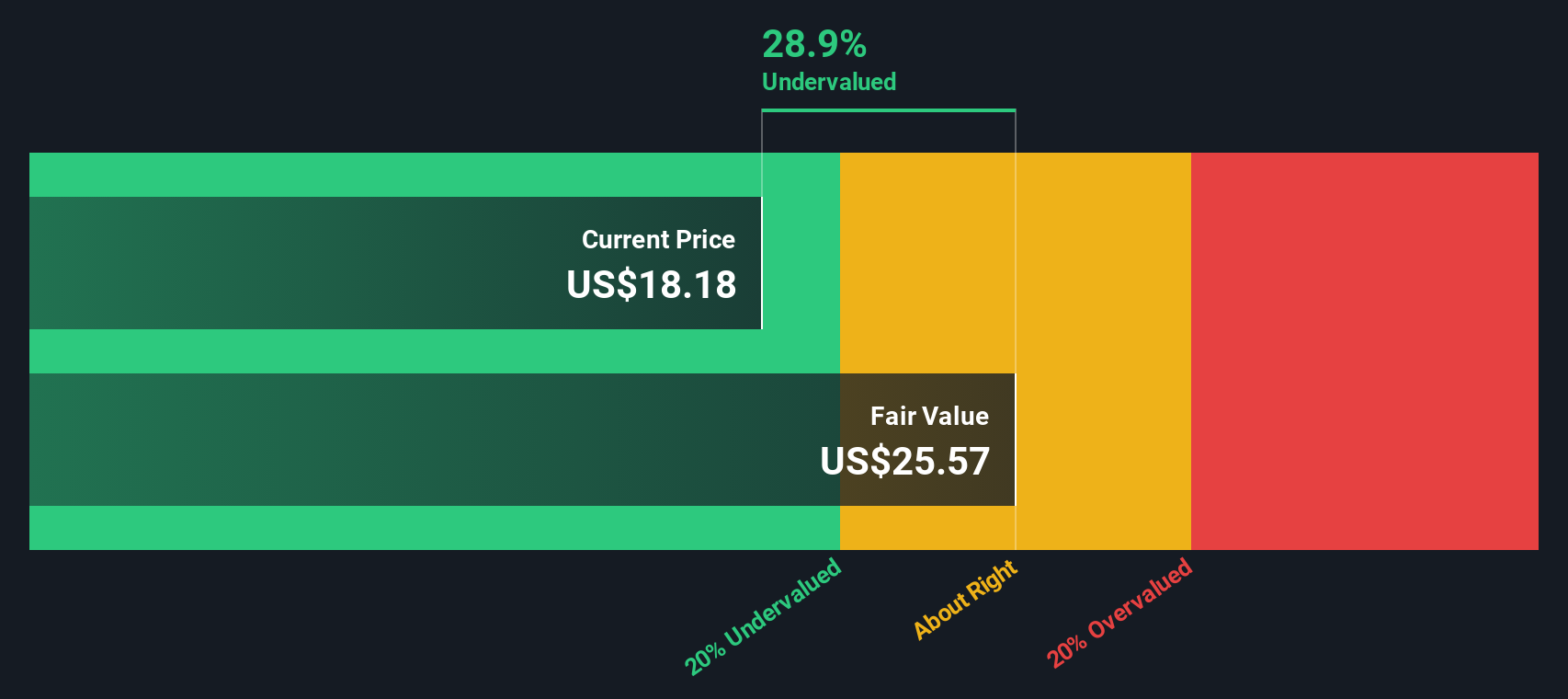

Applying the DCF method to these projections, the estimated intrinsic value per share comes to $23.23. At current prices, this points to a 25.2% discount, suggesting the stock is meaningfully undervalued according to this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Newmark Group is undervalued by 25.2%. Track this in your watchlist or portfolio, or discover 917 more undervalued stocks based on cash flows.

Approach 2: Newmark Group Price vs Earnings

The Price-to-Earnings (PE) ratio is often considered the go-to valuation metric for profitable companies because it ties the company’s market price directly to its bottom-line earnings. Investors frequently rely on the PE ratio to determine how much they are paying for each dollar of a company’s earnings, offering a quick lens for comparing value across similar businesses.

What is considered a “normal” or “fair” PE ratio can shift quite a bit depending on a company’s expected growth and risk profile. Firms with more robust growth outlooks or lower risk typically command higher PE multiples, while those facing uncertainty or slower expansion usually trade at more modest multiples.

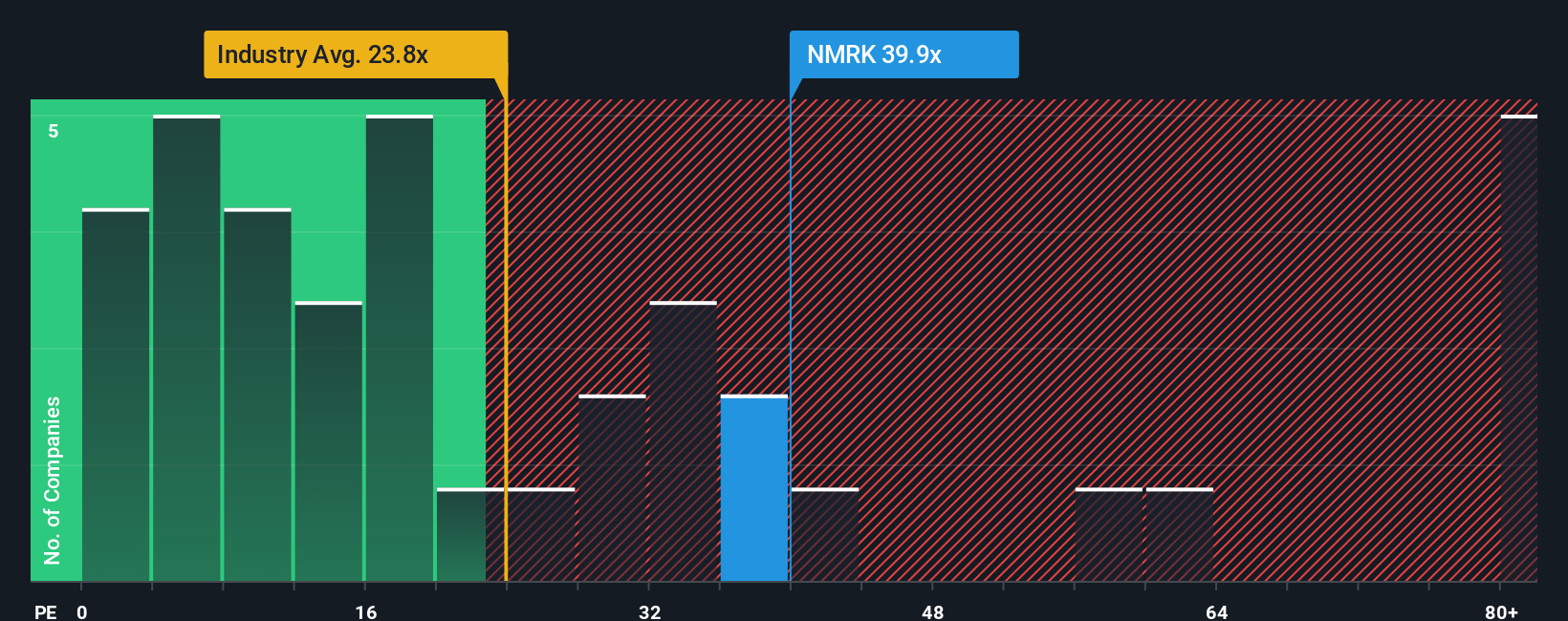

For Newmark Group, the stock’s current PE ratio is 30.3x, which is virtually in line with the average among its industry peers at 30.3x and just above the broader real estate industry average of 29.9x. On the surface, this suggests Newmark is valued comparably to its closest competitors.

However, looking at Simply Wall St’s proprietary “Fair Ratio” metric provides a more nuanced perspective. The Fair Ratio, calculated as 22.5x, incorporates a range of relevant factors including Newmark’s earnings growth, profit margins, market cap, sector risks, and overall industry context. Unlike simple comparisons to peer or industry averages, the Fair Ratio aims to tailor a benchmark that actually fits Newmark’s unique profile.

Comparing the numbers, Newmark’s actual PE of 30.3x is notably above its Fair Ratio of 22.5x. This points to the market assigning a premium to the stock relative to what the underlying fundamentals and risk profile would typically justify.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Newmark Group Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your story for a company: it’s a way to connect what you believe about a business’s future with your own estimates for its revenue, earnings, margins, and ultimately, fair value. In just a few steps, Narratives let you bring the numbers to life by linking your company outlook to a real financial forecast. Then, they show how your assumptions stack up against the current price. Narratives are available to every investor in the Community page on Simply Wall St, used by millions. They are designed to update automatically as new information is released, so your view stays accurate and up to date.

This makes Narratives a powerful, accessible tool to help you decide when to take action by comparing your fair value to the latest market price. For example, with Newmark Group, some investors see bold growth driven by global expansion and increasing demand for digital infrastructure, resulting in a fair value of $22.25. Others are more cautious about margin risk and global uncertainties, seeing a fair value as low as $14.00. Which story fits your view?

Do you think there's more to the story for Newmark Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Newmark Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NMRK

Newmark Group

Provides commercial real estate services in the United States, the United Kingdom, and internationally.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

933 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative