Advertisement

- United States

- /

- Pharma

- /

- NYSE:PRGO

Could Perrigo’s (PRGO) Infant Formula Review Reveal a Shift in Its Capital Allocation Priorities?

Simply Wall St

Reviewed by Sasha Jovanovic

- Perrigo Company plc recently announced it is conducting a strategic review of its infant formula business, exploring a full range of alternatives as part of its Three-S plan to optimize capital allocation and portfolio impact.

- This move comes as Perrigo reassesses a US$240 million investment and considers the shifting strategic fit of infant formula within its broader consumer health focus, highlighting its intent to focus on sustainable growth, cash flow generation, and operational discipline.

- We'll examine how Perrigo's review of its infant formula business could reshape the company's investment narrative and portfolio priorities.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Perrigo Investment Narrative Recap

To be a Perrigo shareholder right now, you have to believe in the company’s ability to reposition itself through sharper portfolio focus, cost discipline, and winning in private-label consumer health, despite soft category consumption and margin pressures. The strategic review of its infant formula business is the headline news, but it is unlikely to materially shift the most important short-term catalyst: private label OTC share gains. That said, execution risk on portfolio changes remains the biggest challenge in the near term.

The recent update to Perrigo’s earnings guidance, signaling lower anticipated 2025 net sales growth, directly ties into ongoing pressures in both the infant formula segment and the broader OTC market, context that frames the importance of this review. It highlights how sensitive Perrigo remains to volatility in these core categories, especially as it works to stabilize and streamline operations.

Yet, despite these efforts, investors should be especially aware that risks from ongoing industry headwinds and operational changes could...

Read the full narrative on Perrigo (it's free!)

Perrigo's outlook projects $4.6 billion in revenue and $183.6 million in earnings by 2028. This assumes a 1.7% annual revenue growth rate and an earnings increase of $243.1 million from the current earnings of -$59.5 million.

Uncover how Perrigo's forecasts yield a $32.50 fair value, a 125% upside to its current price.

Exploring Other Perspectives

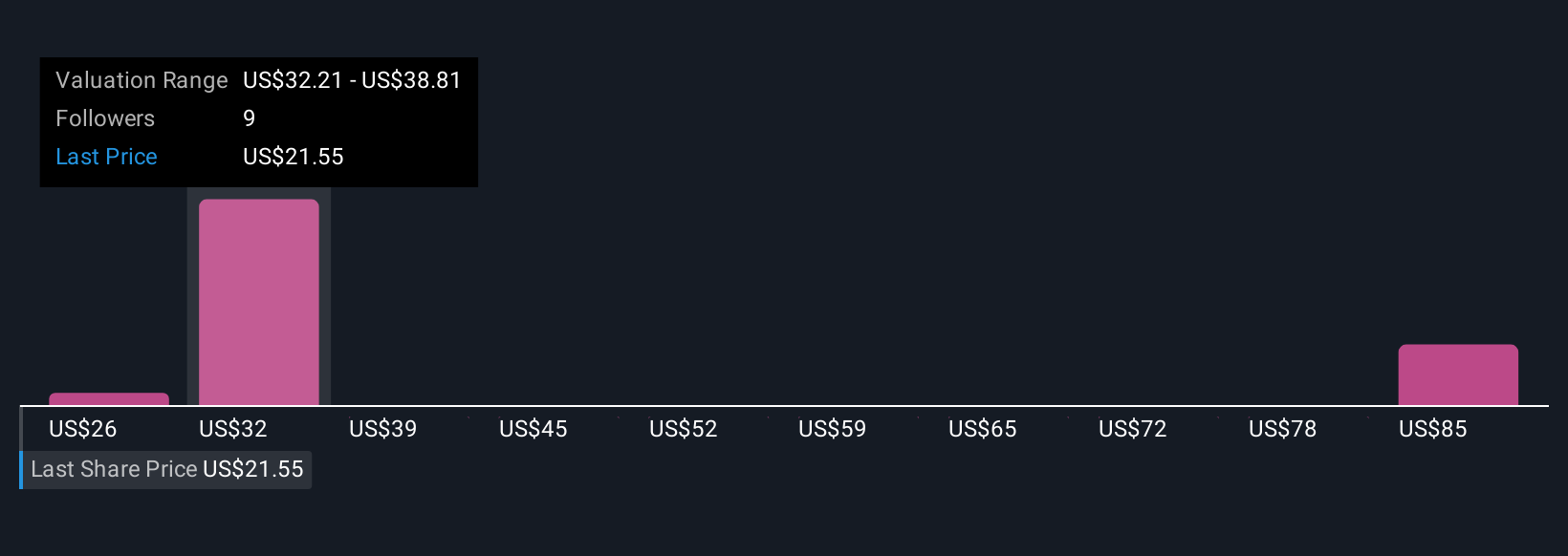

Simply Wall St Community members have set fair value estimates for Perrigo between US$25.60 and US$66.38 across 4 opinions. While many see value given its low price-to-sales ratio, the company's exposure to shifting demand for OTC and nutrition products calls for careful consideration of where performance might trend next.

Explore 4 other fair value estimates on Perrigo - why the stock might be worth just $25.60!

Build Your Own Perrigo Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Perrigo research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Perrigo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Perrigo's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PRGO

Perrigo

Provides over-the-counter health and wellness solutions in the United States, Europe, and internationally.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor