Advertisement

- United States

- /

- Biotech

- /

- NasdaqGM:IRON

Disc Medicine (IRON): Examining Valuation Following Equity Raise and FDA Pipeline Milestone

Simply Wall St

Reviewed by Simply Wall St

Disc Medicine (IRON) completed a $250 million follow-on equity offering and also highlighted major progress in its pipeline, including a key FDA voucher for bitopertin in erythropoietic protoporphyria. This dual update draws investor attention to the company’s near-term momentum.

See our latest analysis for Disc Medicine.

Disc Medicine’s 1-year total shareholder return of nearly 91% stands out, with momentum accelerating further thanks to the recent 40% year-to-date share price return. Its follow-on offering and FDA voucher news have clearly fueled optimism around growth prospects and strategic progress. This indicates investors see tangible catalysts ahead.

If you’re watching how biotech breakthroughs can spark substantial gains, you might want to explore the healthcare sector and discover See the full list for free.

Given Disc Medicine’s standout returns and ongoing progress, the central question for investors now is whether the stock remains undervalued or if the recent run-up already reflects all anticipated growth. This could mean there is little room for further upside.

Price-to-Book of 5x: Is it justified?

Disc Medicine’s current price-to-book ratio sits at 5x, meaning the shares are valued at five times the company’s book value. This is significantly lower than the peer average of 20.7x, suggesting that the market is not pricing the stock as aggressively as similar companies in the sector.

The price-to-book ratio reflects what investors are willing to pay for each dollar of net assets. For a biotech at Disc Medicine’s stage, with rapid pipeline development and ongoing unprofitability, this multiple gives a snapshot of market confidence in its asset base and future growth potential.

Compared to its peers, Disc Medicine appears attractively valued on this basis. While some caution is warranted given industry risks, the lower-than-average ratio suggests the market could be underestimating upcoming milestones and commercial prospects.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 5x (UNDERVALUED)

However, Disc Medicine remains unprofitable. Delays in clinical milestones or regulatory setbacks could quickly undermine current investor optimism and valuations.

Find out about the key risks to this Disc Medicine narrative.

Another View: Discounted Cash Flow Perspective

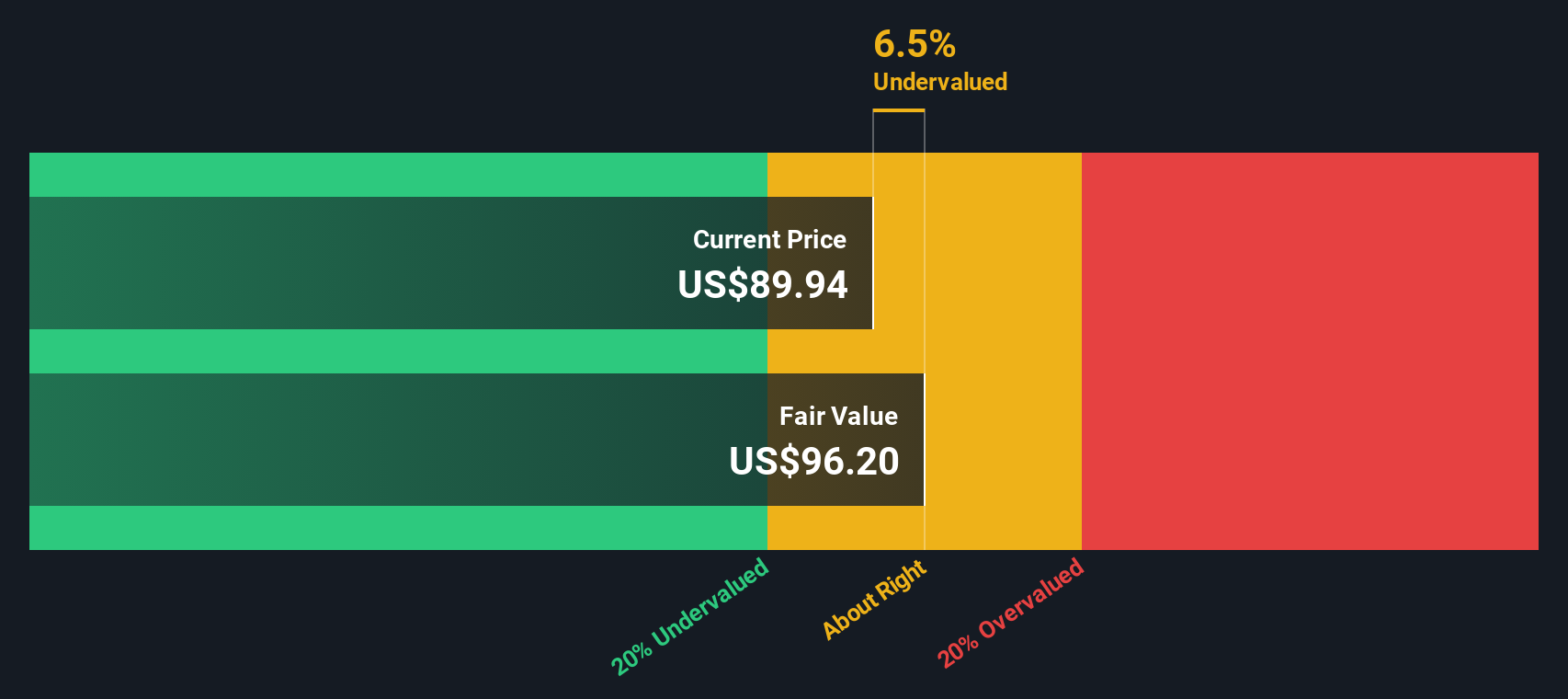

Looking beyond book value, our DCF model suggests Disc Medicine shares trade 27% below what we estimate to be fair value, at $87.61 compared to a DCF value of $120.35. This supports an undervalued argument, but as with all models, much depends on how the future unfolds. Are these forecasts too optimistic, or is there even more upside?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Disc Medicine for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Disc Medicine Narrative

If you want to dig deeper or challenge the outlook here, you can review the underlying figures and craft your own perspective in just a few minutes. Do it your way.

A great starting point for your Disc Medicine research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t limit yourself to just one growth story. Smart investors constantly expand their watchlist. Let me point you toward strategies that could help you spot your next opportunity on Simply Wall Street.

- Target fresh value by unlocking opportunities with these 864 undervalued stocks based on cash flows which highlights stocks currently trading below intrinsic worth.

- Tap into unstoppable income streams by reviewing these 21 dividend stocks with yields > 3% that features yields over 3% from established, dependable companies.

- Ride the next tech wave by searching these 26 AI penny stocks with promising names reshaping industries through artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:IRON

Disc Medicine

A clinical-stage biopharmaceutical company, engages in the discovery, development, and commercialization of novel treatments for patients suffering from serious hematologic diseases in the United States.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor