Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:EXEL

Will Strong Q3 Results and $750M Buyback Shift Exelixis' (EXEL) Outlook?

Simply Wall St

Reviewed by Sasha Jovanovic

- Exelixis reported strong third quarter results, raised its earnings guidance for 2025, and announced a new US$750 million share repurchase program, following a series of operational updates and executive changes that included a new General Counsel appointment this November.

- Investor attention was drawn by the combination of improved financial performance, increased revenue outlook, and substantial capital return commitments.

- We'll examine how the upgraded financial guidance and share buyback program impact Exelixis's investment narrative and outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Exelixis Investment Narrative Recap

Being a shareholder in Exelixis ultimately comes down to believing in the company’s ability to expand beyond its CABOMETYX franchise, while managing the risks of revenue concentration and competitive pressures in oncology. The latest earnings beat and upgraded guidance are positive signals, but they do not materially shift the biggest short-term catalyst, progress in late-stage trials like zanzalintinib in colorectal cancer, nor do they ease the overreliance on CABOMETYX, which remains a central risk.

Of the recent announcements, the US$750 million share repurchase program is especially relevant. This move signals management’s confidence in the company’s longer-term earning power and capital position, which may attract investors seeking capital return. However, the main growth catalyst in the near term continues to hinge on pipeline advancement and new product launches, not buybacks.

By contrast, investors should also be aware that any disruption to CABOMETYX exclusivity or steeper 340B volume growth could quickly...

Read the full narrative on Exelixis (it's free!)

Exelixis' narrative projects $3.1 billion in revenue and $1.1 billion in earnings by 2028. This requires 11.7% yearly revenue growth and a $497.7 million increase in earnings from $602.3 million today.

Uncover how Exelixis' forecasts yield a $44.06 fair value, a 6% upside to its current price.

Exploring Other Perspectives

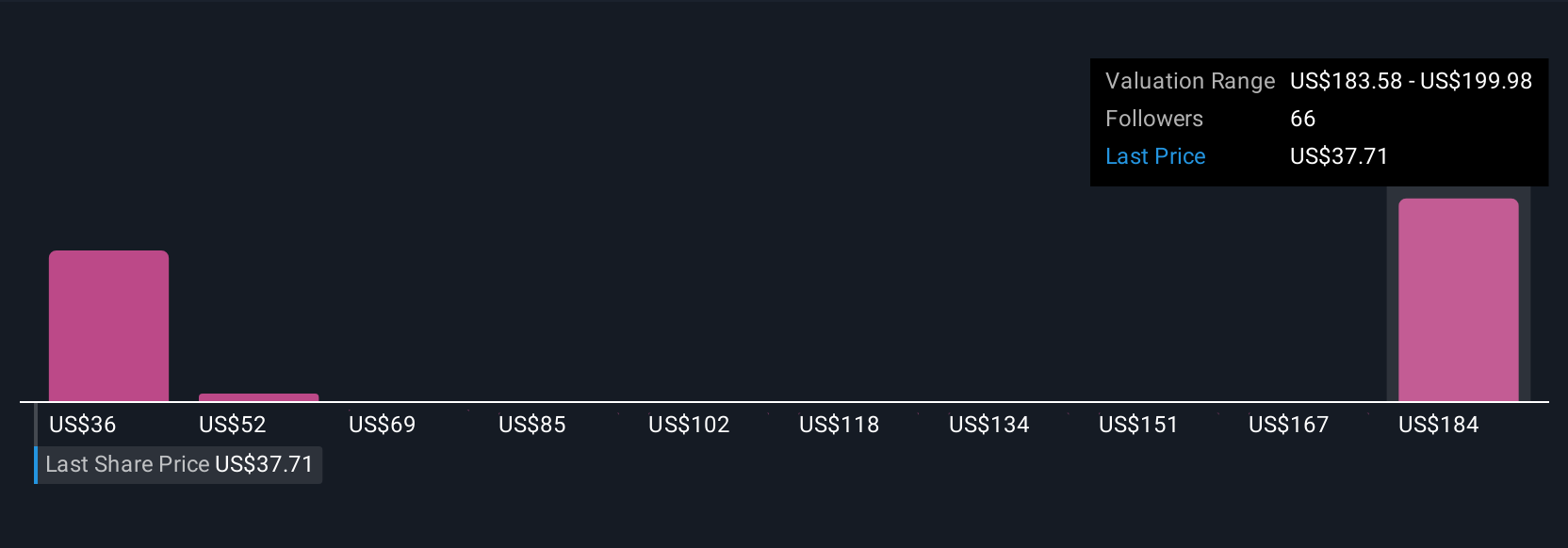

Twelve fair value estimates from the Simply Wall St Community span from US$36 to over US$197 per share, highlighting the wide variance in investor outlooks. While opinions differ, many focus on future pipeline successes as the main factor influencing Exelixis’s performance, making it important to assess several viewpoints.

Explore 12 other fair value estimates on Exelixis - why the stock might be worth 14% less than the current price!

Build Your Own Exelixis Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Exelixis research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Exelixis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Exelixis' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Exelixis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:EXEL

Exelixis

An oncology company, focuses on the discovery, development, and commercialization of new medicines for difficult-to-treat cancers in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor