Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:EXEL

Board Member’s $1.2 Million Share Buy Might Change the Case for Investing in Exelixis (EXEL)

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Exelixis board member David Johnson purchased 27,500 shares for approximately US$1.2 million, reinforcing interest in the company’s future direction.

- This substantial insider investment stands out as a meaningful show of confidence by a key leader, particularly given Exelixis’s focus on advancing cancer therapies.

- With this significant board member share purchase as a backdrop, we’ll look at how insider confidence shapes Exelixis’s broader investment narrative.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Exelixis Investment Narrative Recap

To be a shareholder of Exelixis, you need to share the belief that its leadership in cancer therapies and innovative pipeline can offset risks tied to its reliance on CABOMETYX, its main revenue contributor. While David Johnson’s recent US$1.2 million insider share purchase indicates board-level confidence, it does not materially impact the near-term catalyst of pipeline progress, nor does it shift the most significant risk: future revenue vulnerability once CABOMETYX faces generic competition.

Among recent announcements, the promising results from the STELLAR-303 trial, where zanzalintinib showed a 20% reduction in risk of death for colorectal cancer, resonates strongly. This development is closely linked to the company's main catalyst, as further clinical trial wins and new drug approvals could diversify Exelixis’s revenue base and mitigate risks from heavy reliance on a single product.

By contrast, investors should be mindful that rising 340B sales mean a higher share of Exelixis’s business is exposed to price …

Read the full narrative on Exelixis (it's free!)

Exelixis' outlook anticipates $3.1 billion in revenue and $1.1 billion in earnings by 2028. This projection relies on an annual revenue growth rate of 11.7% and an earnings increase of $497.7 million from the current $602.3 million.

Uncover how Exelixis' forecasts yield a $44.61 fair value, in line with its current price.

Exploring Other Perspectives

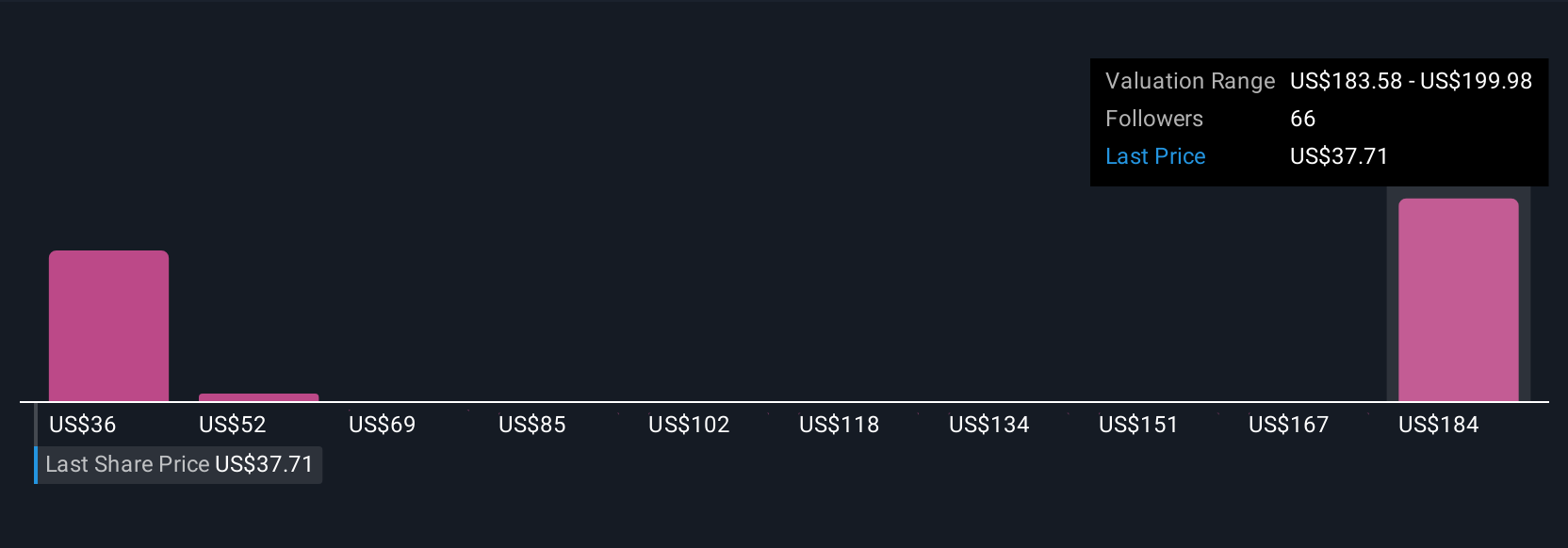

Twelve individual perspectives from the Simply Wall St Community put Exelixis’s estimated fair value as low as US$36 and as high as US$185,847 a share. With Exelixis’s dependence on CABOMETYX so pronounced, you may want to explore how shifts in pricing or patent exclusivity could shape future outcomes.

Explore 12 other fair value estimates on Exelixis - why the stock might be worth over 4x more than the current price!

Build Your Own Exelixis Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Exelixis research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Exelixis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Exelixis' overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Exelixis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:EXEL

Exelixis

An oncology company, focuses on the discovery, development, and commercialization of new medicines for difficult-to-treat cancers in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative