Stock Analysis

- United States

- /

- Biotech

- /

- OTCPK:DMTK.Q

We're Not Very Worried About DermTech's (NASDAQ:DMTK) Cash Burn Rate

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, DermTech (NASDAQ:DMTK) shareholders have done very well over the last year, with the share price soaring by 180%. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

In light of its strong share price run, we think now is a good time to investigate how risky DermTech's cash burn is. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). Let's start with an examination of the business' cash, relative to its cash burn.

Check out our latest analysis for DermTech

How Long Is DermTech's Cash Runway?

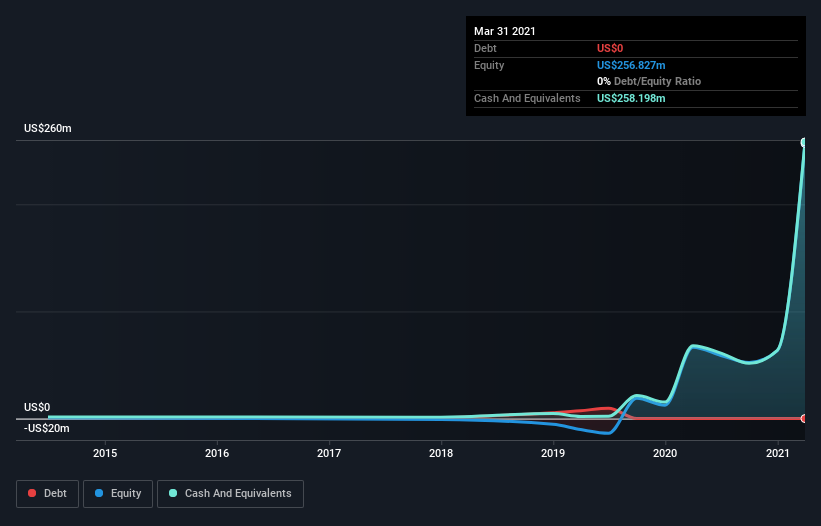

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In March 2021, DermTech had US$258m in cash, and was debt-free. Looking at the last year, the company burnt through US$34m. That means it had a cash runway of about 7.7 years as of March 2021. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. The image below shows how its cash balance has been changing over the last few years.

How Well Is DermTech Growing?

At first glance it's a bit worrying to see that DermTech actually boosted its cash burn by 47%, year on year. Having said that, it's revenue is up a very solid 58% in the last year, so there's plenty of reason to believe in the growth story. The company needs to keep up that growth, if it is to really please shareholders. On balance, we'd say the company is improving over time. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

Can DermTech Raise More Cash Easily?

There's no doubt DermTech seems to be in a fairly good position, when it comes to managing its cash burn, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$1.1b, DermTech's US$34m in cash burn equates to about 3.0% of its market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

How Risky Is DermTech's Cash Burn Situation?

As you can probably tell by now, we're not too worried about DermTech's cash burn. In particular, we think its revenue growth stands out as evidence that the company is well on top of its spending. Although its increasing cash burn does give us reason for pause, the other metrics we discussed in this article form a positive picture overall. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. On another note, DermTech has 4 warning signs (and 1 which is concerning) we think you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

If you decide to trade DermTech, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether DermTech is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OTCPK:DMTK.Q

DermTech

A molecular diagnostic company, engages in the development and marketing of novel non-invasive genomics tests to aid in the diagnosis and management of melanoma in the United States.

Fair value with mediocre balance sheet.