Advertisement

- United States

- /

- Life Sciences

- /

- NasdaqCM:BLFS

BioLife Solutions (BLFS) Refocuses on Cell Processing After Evo Sale—Is Its Core Platform Ready to Scale?

Reviewed by Sasha Jovanovic

- BioLife Solutions, Inc. recently reported third-quarter 2025 results, posting US$28.07 million in revenue and earnings of US$0.01 per share, both of which surpassed analyst expectations following the sale of its evo cold chain logistics segment.

- This shift enables BioLife Solutions to focus on accelerating growth in its core cell processing platform, which has seen strong recurring demand and expanded market share.

- We will examine how the updated 2025 revenue guidance, raised after the business divestiture, may shape BioLife’s investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

BioLife Solutions Investment Narrative Recap

To own shares of BioLife Solutions, you need to believe in the expanding adoption of advanced cell and gene therapies, with BioLife’s core cell processing platform benefiting from continued momentum and integration into clinical workflows. The company’s third-quarter results, which beat revenue and earnings expectations, support enthusiasm around recurring demand, but also shine a light on key risks such as heavy reliance on a concentrated customer base, which could drive earnings volatility if large clients reduce orders. The recent news significantly reinforces the short-term catalyst of recurring revenue growth, while the customer concentration risk remains an important consideration for shareholders.

BioLife’s updated 2025 revenue guidance, projecting 27% to 29% year-over-year growth after the divestiture of evo cold chain logistics, stands out in the context of this earnings beat. With cell processing platform revenue targets raised to US$93.0 million to US$94.0 million, the company appears to be capitalizing on higher recurring demand within its core business segment, a factor closely watched by investors looking for clear growth levers and operational focus.

However, while the growth outlook excites, investors should also be alert to the less visible risk if one of BioLife’s largest customers decides to...

Read the full narrative on BioLife Solutions (it's free!)

BioLife Solutions' narrative projects $161.3 million revenue and $33.2 million earnings by 2028. This requires 19.9% yearly revenue growth and a $52.1 million increase in earnings from -$18.9 million today.

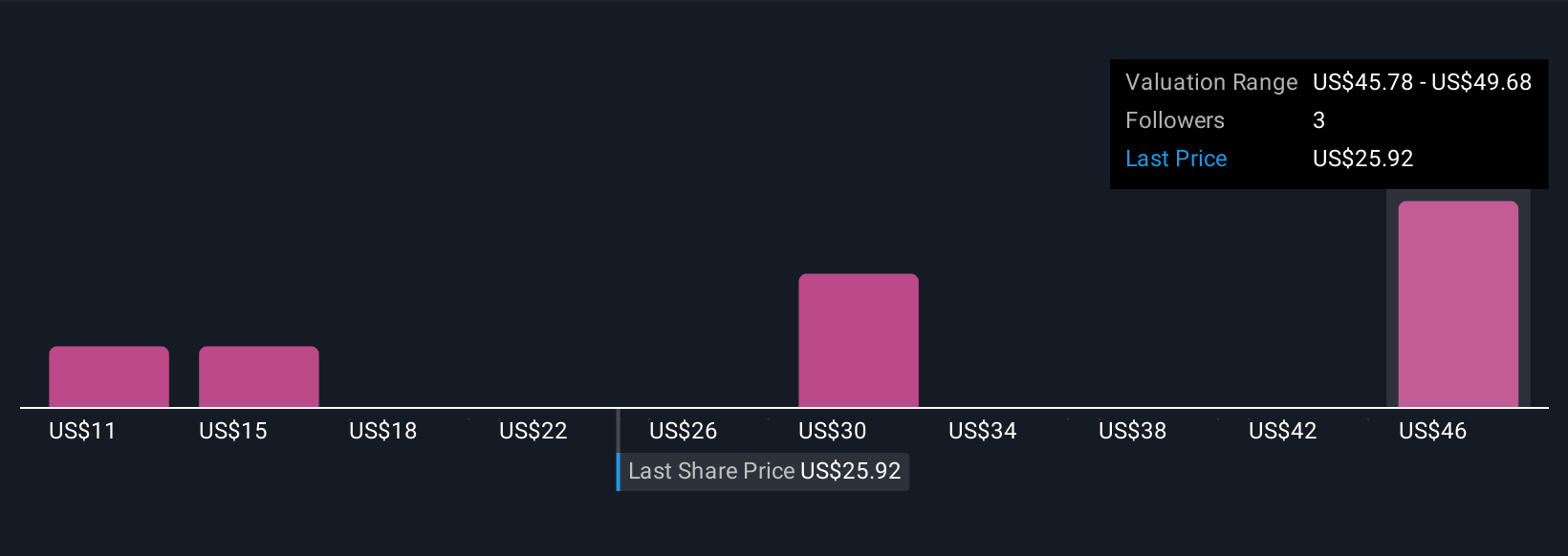

Uncover how BioLife Solutions' forecasts yield a $31.30 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community valued BioLife Solutions between US$10.69 and US$38.66 per share ahead of this news. In contrast, recurring revenue growth and customer concentration could have outsized effects on future performance, highlighting why it pays to consider multiple perspectives.

Explore 4 other fair value estimates on BioLife Solutions - why the stock might be worth less than half the current price!

Build Your Own BioLife Solutions Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your BioLife Solutions research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free BioLife Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BioLife Solutions' overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BioLife Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:BLFS

BioLife Solutions

Develops, manufactures, and markets bioproduction products and services for the cell and gene therapy (CGT) industry in the United States, Europe, the Middle East, Africa, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7058.5% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17045.8% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38029.2% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

RE

REElax on Volta Metals ·

Springer REE deposit valuation

Fair Value:CA$3.595.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Atlas Salt ·

Once In A Life Time Deeply Discounted Recession Proof Utility

Fair Value:CA$2.9656.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PittTheYounger on SSAB ·

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value:SEK 79.1721.8% overvalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7449.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.3% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.9% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

KA

Karndog on Berkshire Hathaway ·

Abel is also an Energy expert. He's already on the AI train even without "buying tech".

0

|0

SI

Simply Wall St User on Automatic Data Processing ·

This stock with dividend Aristocrat status and real annual increases may require more time to ascert...

0

|0

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

0

|0