Advertisement

- United States

- /

- Media

- /

- NYSE:NYT

A Look at New York Times (NYT) Valuation Following Recent Share Price Momentum

Simply Wall St

Reviewed by Simply Wall St

Shares of New York Times (NYT) have recently seen some upward movement, capturing attention from investors who are tracking the company’s longer-term performance. Many are weighing current valuations in comparison to recent momentum in the stock.

See our latest analysis for New York Times.

New York Times shares have surged in recent weeks, with a 30-day share price return of over 13% adding to their strong year-to-date momentum. This renewed enthusiasm follows a solid wave of digital subscription growth and steady profitability, and has helped push the company’s 1-year total shareholder return to more than 20%. Momentum appears to be building as investors respond to consistent results and optimism around future growth.

If you’re curious to see what else is drawing investor interest right now, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

But with shares now hovering close to analyst price targets, the key question is whether New York Times remains undervalued, or if the market has already factored in the company’s growth prospects. Is a compelling buying opportunity emerging, or has the market already priced in what comes next?

Most Popular Narrative: 0.8% Undervalued

New York Times closed at $64.50, while the most widely followed analyst narrative places fair value at $65. This positions the company just below consensus estimates and brings attention to the factors influencing this valuation.

Robust growth in digital subscriptions, driven by an expanding portfolio of bundled offerings (news, Cooking, Games, The Athletic) and a focus on direct consumer relationships, positions the company to capture more recurring revenue, strengthen ARPU, and reduce churn. This directly supports long-term revenue and margin expansion. Rising global demand for trusted, high-quality journalism amid increasing misinformation is enabling NYT to increase its international reach and subscription base, paving the way for sustained top-line growth and a larger addressable market.

Want to know which bold projections lie behind this razor-thin margin between price and fair value? The narrative centers on fast-paced digital growth, international expansion, and optimism in recurring revenue. Curious about the math driving this precise valuation? Uncover the full picture behind the headline numbers.

Result: Fair Value of $65 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks such as declining referral traffic from tech platforms and increasing content commoditization could challenge New York Times's long-term subscriber growth and revenue outlook.

Find out about the key risks to this New York Times narrative.

Another View: Multiples Suggest Expensive Territory

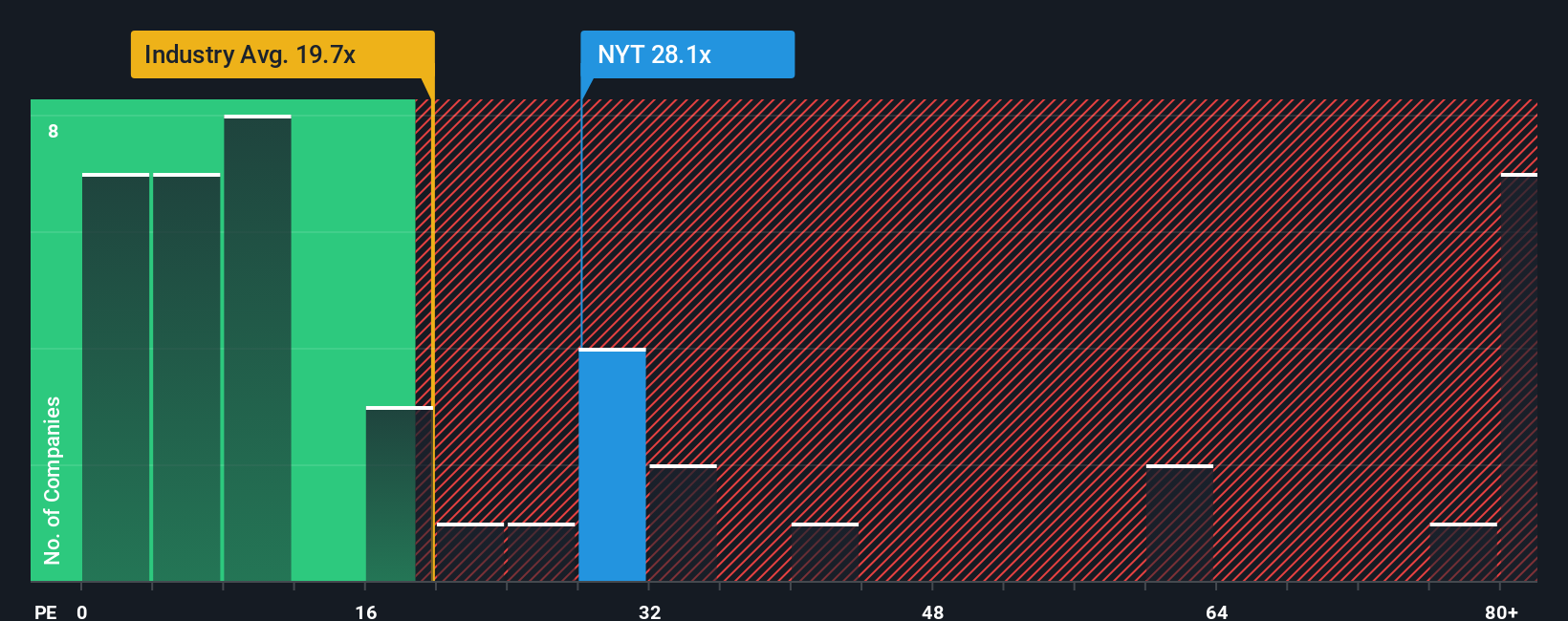

While the consensus narrative points to undervaluation, our comparison using earnings multiples tells a different story. New York Times is trading at a 31x price-to-earnings ratio, which is much higher than both the US Media industry average of 15.4x and its peer average of 17x. Even compared to the fair ratio of 20.2x, NYT appears pricey. This could mean less upside if the market decides to shift toward that lower valuation. Could this premium signal the market’s confidence, or does it hint at potential pullback risk ahead?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own New York Times Narrative

If you think there’s more to the story or want to dig deeper into the data yourself, you can craft your own view in just a few minutes. Do it your way

A great starting point for your New York Times research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don't let opportunity pass by. Reward your curiosity and accelerate your portfolio's growth. These unique stock ideas could be exactly what your strategy needs.

- Unlock the income potential of high-yield portfolios by tapping into these 15 dividend stocks with yields > 3% with generous returns above 3%.

- Ride the innovation wave as artificial intelligence transforms industries by checking out these 25 AI penny stocks at the forefront of this technological shift.

- Capitalize on breakthrough healthcare advancements powered by data and machine learning when you browse these 30 healthcare AI stocks boasting real, future-focused impact.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if New York Times might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NYT

New York Times

The New York Times Company, together with its subsidiaries, creates, collects, and distributes news and information worldwide.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7117.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

108 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative