- United States

- /

- Media

- /

- NYSE:DV

DoubleVerify Holdings (DV) Stock Declines 7% Over Last Month

Reviewed by Simply Wall St

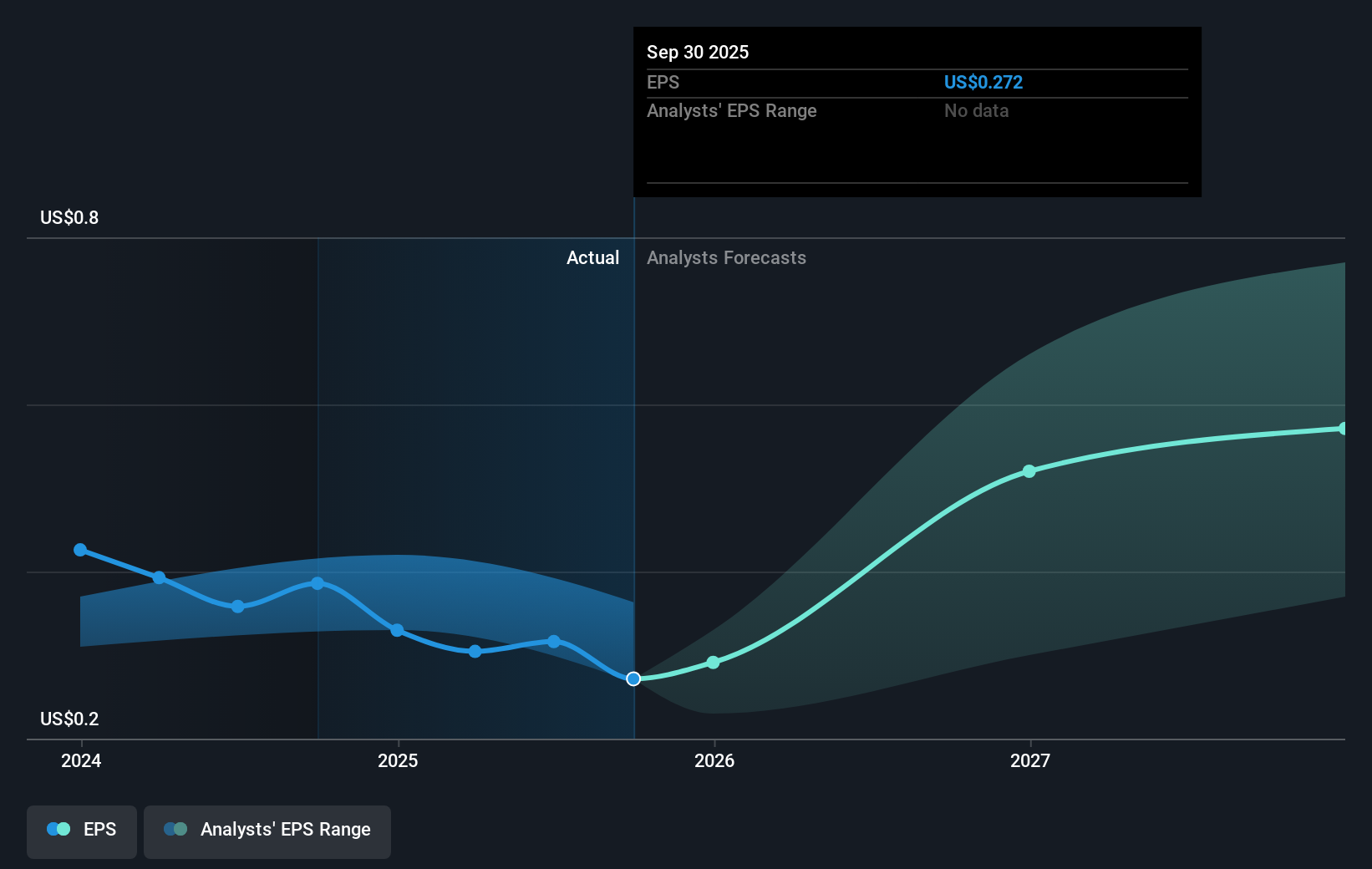

DoubleVerify Holdings (DV) experienced a price movement of 6.88% during the last month, amidst an environment where the major U.S. stock indexes, like the S&P 500 and Nasdaq, reached record highs following favorable consumer inflation data, which bolstered hopes for a Federal Reserve rate cut. While the market rise of 1.4% within the last week contributed to a generally positive sentiment, DV's decline over the past month stands in contrast. During this period, specific company-related events may not have significantly impacted DV, and its share performance largely counteracted broader market trends.

The recent market dynamics, highlighted by the significant price movement of DoubleVerify Holdings (DV), contrast with broader market trends, creating a complex backdrop for its narrative. Although DV saw a decline over the past month, its share price performance comes after a year-long total return of 23.08% decline, underperforming the US Market, which returned 20% over the same period. This underperformance may reflect market skepticism regarding DV's ability to capitalize on its strategic initiatives in the expanding Connected TV and social media markets. Nevertheless, the company's comprehensive approach to innovation in digital ad verification and platform integrations continues to support its revenue diversification and long-term growth potential.

The recent market sentiment, fueled by potential federal monetary policy changes, creates an opportunity for DV to potentially benefit from a favorable economic outlook. However, this has not yet translated into significant share price recovery. As DV trades considerably below analysts' consensus price target of US$19.39, there remains a gap between current perceptions and expected enterprise valuation, which may hinge on achieving projected revenue growth and profit margins. Current earnings projections of US$114 million in 2028 underscore the need for robust, consistent performance to justify such targets. Ultimately, while short-term movements may fluctuate, investors will likely keep a close eye on DV's execution of its growth strategy in an increasingly competitive digital advertising landscape.

Take a closer look at DoubleVerify Holdings' potential here in our financial health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DV

DoubleVerify Holdings

Provides media effectiveness platforms in the United States and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion