Advertisement

- United States

- /

- Media

- /

- OTCPK:DMSL.Q

New Forecasts: Here's What Analysts Think The Future Holds For Digital Media Solutions, Inc. (NYSE:DMS)

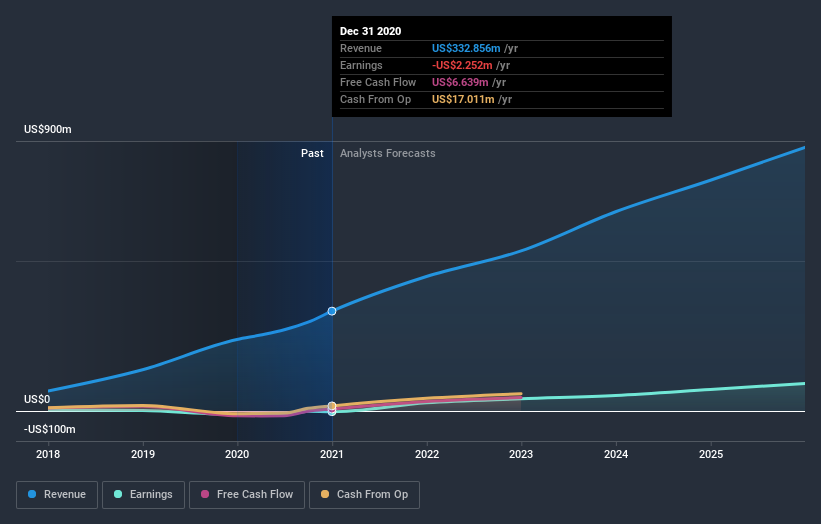

Celebrations may be in order for Digital Media Solutions, Inc. (NYSE:DMS) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline. The stock price has risen 6.7% to US$12.99 over the past week, suggesting investors are becoming more optimistic. Whether the upgrade is enough to drive the stock price higher is yet to be seen, however.

Following the upgrade, the current consensus from Digital Media Solutions' three analysts is for revenues of US$459m in 2021 which - if met - would reflect a huge 38% increase on its sales over the past 12 months. The losses are expected to disappear over the next year or so, with forecasts for a profit of US$0.56 per share this year. Before this latest update, the analysts had been forecasting revenues of US$417m and earnings per share (EPS) of US$0.52 in 2021. Sentiment certainly seems to have improved in recent times, with a decent improvement in revenue and a small lift in earnings per share estimates.

Check out our latest analysis for Digital Media Solutions

Despite these upgrades, the analysts have not made any major changes to their price target of US$15.25, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Digital Media Solutions, with the most bullish analyst valuing it at US$16.00 and the most bearish at US$14.00 per share. This is a very narrow spread of estimates, implying either that Digital Media Solutions is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Digital Media Solutions' past performance and to peers in the same industry. We can infer from the latest estimates that forecasts expect a continuation of Digital Media Solutions'historical trends, as the 38% annualised revenue growth to the end of 2021 is roughly in line with the 38% annual revenue growth over the past three years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 4.6% per year. So although Digital Media Solutions is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Digital Media Solutions.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Digital Media Solutions going out to 2025, and you can see them free on our platform here..

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you decide to trade Digital Media Solutions, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OTCPK:DMSL.Q

Digital Media Solutions

Provides technology enabled digital performance advertising solutions connecting consumers and advertisers in the United States.

Moderate and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor