- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:TBLA

Taboola (TBLA): Weighing Insider Selling and Technical Signals Against a 10% Undervaluation Case

Reviewed by Simply Wall St

Taboola.com (TBLA) just slipped about 3% after a technical sell signal flashed and recent insider share sales grabbed traders attention, even as the company follows up stronger than expected quarterly results with upbeat guidance.

See our latest analysis for Taboola.com.

Zooming out, Taboola.com’s $4.03 share price sits on top of a solid 90 day share price return of about 15%, even though the 1 year total shareholder return is more modest. This suggests momentum is building but still tentative as investors weigh growth against insider selling and technical noise.

If this kind of mixed momentum has you rethinking your watchlist, it could be a good time to explore high growth tech and AI stocks for more tech names with different risk reward profiles.

With shares still trading below analyst targets and a hefty modeled discount to intrinsic value, is Taboola quietly offering growth at a reasonable price, or is the market already factoring in the next phase of its AI driven expansion?

Most Popular Narrative: 10.4% Undervalued

With Taboola.com’s fair value pinned at 4.50 dollars and the stock last closing at 4.03 dollars, the narrative leans toward upside potential built on improving fundamentals.

The analysts have a consensus price target of $4.167 for Taboola.com based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.2 billion, earnings will come to $37.6 million, and it would be trading on a PE ratio of 33.7x, assuming you use a discount rate of 8.5%.

Curious how modest revenue growth, a lean but improving margin profile, and a future premium multiple all connect to that upside case? The full narrative unpacks the exact growth path, the earnings ramp, and the valuation bridge that must hold for this target to make sense.

Result: Fair Value of $4.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside still hinges on Realize gaining real traction, and on open web traffic holding up as AI powered search and walled gardens reshape discovery.

Find out about the key risks to this Taboola.com narrative.

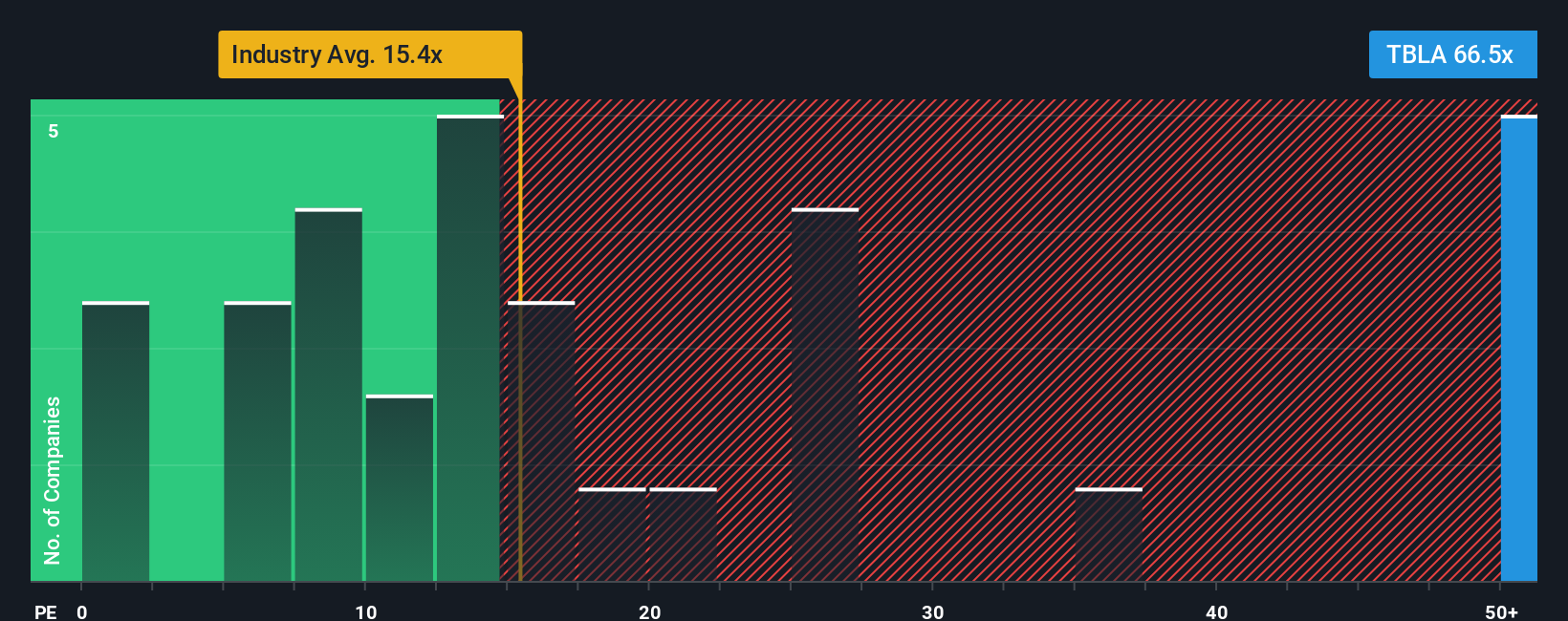

Another View: Rich on Earnings

There is a catch. On an earnings basis Taboola.com trades at about 45.9 times profits, compared with roughly 16 times for both the wider US interactive media space and its peer group, and a fair ratio of 16 times. That rich gap could unwind if growth disappoints, or it could widen if sentiment turns.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Taboola.com Narrative

If you see the story differently or would rather dig into the numbers yourself, you can shape a fresh view in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Taboola.com.

Looking for more investment ideas?

Do not stop at one opportunity; use the Simply Wall Street Screener to uncover more focused ideas that match your strategy and keep you ahead of the crowd.

- Capitalize on early stage potential by reviewing these 3614 penny stocks with strong financials that already exhibit strong fundamentals instead of just speculative hype.

- Position yourself for potential productivity gains by targeting these 25 AI penny stocks that use artificial intelligence to reshape industries and margins.

- Explore risk and reward setups through these 914 undervalued stocks based on cash flows that appear attractively priced relative to their projected cash flows and business quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Taboola.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TBLA

Taboola.com

Operates an artificial intelligence-based algorithmic engine platform in Israel, the United States, the United Kingdom, Germany, and internationally.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion